According to a recent article by Daniel Amerman, Economists Can’t Account For 98% Of Rising Inflation (hat tip to Chris Coles for calling this to our attention). Referring to a Wall Street Journal article, Amerman says

”According to the article and the prominent economists interviewed, the leading inflation prediction methodology used by economists completely failed, leaving the Federal Reserve, White House & European Central Bank stunned and blindsided by the highest rates of inflation in 40 years.”

Could it be that conventional economics is 98% garbage? You bet. It’s so rent with false assumptions and invalid premises it’s hard to know where to start. But one standout with regard to inflation is that it – inexplicably – pretends that it affects only consumer prices. Asset prices can soar into outer space and it’s as if inflation had nothing to do with it.

We took a deeper dive into this problem in The Big Takeaway. Economists, either through gross negligence or willful self-delusion, have been wandering about their own field wearing self-donned blinders. They arbitrarily exclude asset prices from their reckoning of inflation. Maybe it’s because inflation is fun while it’s contained to asset prices, and they allow value judgment to cloud their vision. Inflation is a Bad Thing and therefore it cannot be inflation while it feels Good. Throwing objectivity out the window like this wouldn’t be acceptable in any other field aspiring to the status of science, but for some reason it’s become routine in economics.

So stock prices quintuple over the course of a decade. It’s just prosperity. Never mind that when the owners of stocks go to cash in their gains and buy stuff with them, that the amount of stuff out there hasn’t quintupled. The actual “prosperity” didn’t happen. All that happened was the nominal price of claims on stuff rose unsupported … how could this not be inflation?

If we can’t help ourselves and simply must allow value judgments to compromise our capacity to think clearly, maybe we should at least consider the possibility it was a Bad Thing all along. The illusion of wealth where it isn’t justified – confusing the expansion of claims on wealth with the real thing – should be taken as a sign that something is amiss. That maybe policy isn’t as appropriate as we thought. Must economics be forever condemned to acknowledge reality only after it has been painfully thrust in its face? As I’ve pointed out repeatedly, it’s simply not possible for asset prices to rise indefinitely without consumer prices eventually following suit.

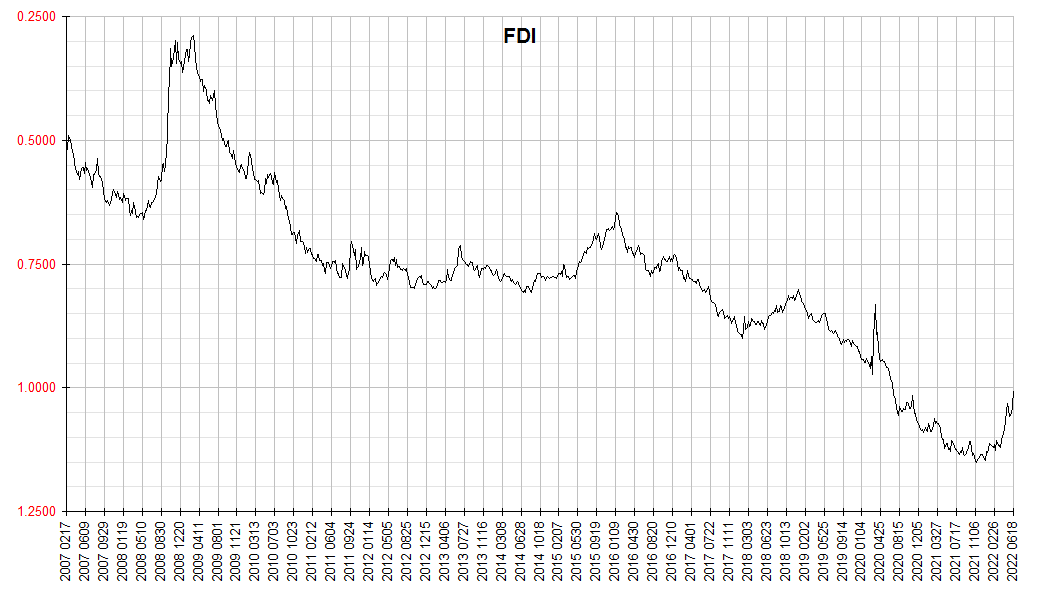

This is no mere Monday morning quarterbacking. We’ve been 2% economists from the start … long before consumer price inflation was making headlines we tipped the that commodity prices were due to soar this decade. We didn’t call it “inflation” simply because it’s our position that It’s Been Inflation All Along. The only thing that’s changed is that it’s finally spilled over into commodity and consumer prices in a big way. Our home grown index of inflation, the FDI, draws on all classes of prices, and has since inception over fifteen years ago.

Amerman himself, alas, remains firmly ensconced in the 98%. He fingers fiscal policy as the cause of this inflation. No doubt it’s been a catalyst in greasing the skids for the spillover from asset prices into consumer prices, but that’s all. It was inevitable. He still shows no sign of understanding the fundamental nature of inflation as depreciation of currency, instead putting the focus on supply and demand for stuff. That understanding appears yet confined to the 2%.

To truly understand inflation is to understand two central points:

1) Inflation is currency depreciation. It is not things “going up”. It simply takes more of the shrunken currency units to buy the same stuff.

2) Inflation does not affect all prices uniformly and simultaneously. It first affects the prices of things used to store value (assets) and only later spills over into other prices (goods and services) for which that stored value is spent.

FDI 2022 0618

Thanks for the timely reminder Bill.

I’m keen to hear your views on the driver(s) for Fed’s mandate of maintaining inflation at 2%. Is it rooted in managing currency depreciation or in maintaining price stability.

We’re left to speculate because the Fed doesn’t talk about currency depreciation. It’s likely the ultimate driver though.

The official explanation is that 2% is sort of a buffer to avoid deflation. A slippery slope theory of deflation … if you get too close to 0% you might slip and slide down into a spiral…

Bollocks. No theoretical mechanism has ever been offered. Even worse, the empirical data indicate just the opposite. The most intense deflationary episode of modern times was borne amid accelerating inflation. Remember oil hit $147 a barrel in the middle of 2008 … CPI had shot over 5%. This was mere weeks before Fannie Mae and Freddie Mac had to be taken into Treasury conservatorship and only shortly thereafter Lehman Bros infamously imploded. CPI went negative shortly after that.

If anything a rational economist would have to conclude that the cause of deflation is inflation.

Yet beginning with Ben Bernanke, the Fed insists otherwise. There is only one logical conclusion: the Fed is not being run by rational economists.

Less logical yet plausible is that it provides the Fed with a justification for holding rates lower than it would otherwise … possibly because it’s beholden to Wall Street, or to subsidize deficit spending … the only thing we know for sure is that it doesn’t serve the interests of the general American public.

Corporate managements benefit from currency depreciation because it forces savers out of currency and into stocks. This results in a captive investor base unable to challenge the self serving stock option and buyback schemes that make corporate insiders rich. Politicians benefit because they don’t have to fully fund programs with taxes. With much of the cost funded by the hidden inflation tax, programs appear to have a much more favorable cost benefit profile than is actually the case.

Finally, there is a perfectly solid theoretical mechanism explaining how inflation causes deflation, once inflation is understood as currency depreciation. If the currency can be counted on to depreciate, one can easily profit by going short. That is, by taking on debt. But once the trade becomes too popular, it can no longer work. Not everyone can short something and profit. If it were possible, everyone could just quit working and live off currency depreciation. Farmers wouldn’t need to plow their fields, truckers wouldn’t need to haul goods to market, teachers needn’t teach, doctors needn’t heal … in short, everyone would have plenty of money but nothing to buy with it. Rich but starving. If this sounds vaguely reminiscent of the current state of the economy, perhaps it’s no accident…

But any attempt to halt the process short of hyperinflationary apocalypse triggers a short squeeze. Debt is no longer profitable, but becomes costly, and people rush to cover. The currency appreciates in value, which – if inflation is depreciation – is deflation.

The cause of deflation is inflation.

I listened to a podcast last week with Judy Shelton where she shared that the 2% number originated decades ago when Greenspan was chair and Yellen was a governor heavily influenced by her husband who is a labor economist. So the 2% came from Janet Yellen. The rationale is that it is difficult to cut wages, so better to avoid periods where inflation could come in negative and employers lay off people rather than cut wages and 2% provides somewhat of a buffer. Apparently, Greenspan was anxious about the minutes of the meeting where this was discussed, fearing that the Fed might be perceived as not following the law that mandates that the Federal Reserve should control inflation and maintain the value of the currency.

Thanks, kbird … I hadn’t heard that before. Just that Bernanke’s two predecessors – Volcker and Greenspan – both opposed it. I’d also read that historically the 2% figure originated in New Zealand.

Here are a couple links for further reading:

https://mises.org/power-market/origins-2-percent-inflation-target

https://www.stlouisfed.org/open-vault/2019/january/fed-inflation-target-2-percent

Thanks for the detailed response and additional links Bill.

The first link does refer to Yellen’s support for inflation targeting, corroborating Judy Shelton’s account, thank you Kbird for sharing this.

Thank you, Sunpearl. It’s a pretty good account of all of it … from NZ to Yellen to the rest of the Fed … to its faulty rationale. It also highlights Yellen’s major contribution to today’s economic environment.