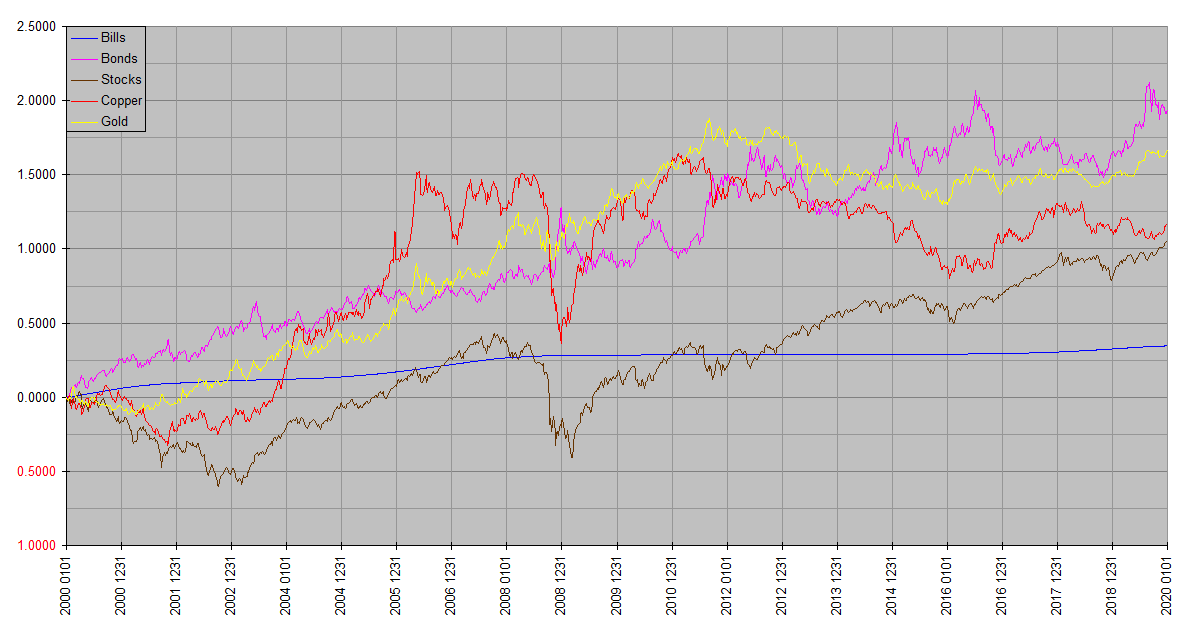

Let’s open with a big picture review of the first twenty years of this century. For the following major asset classes, from WTBFOTS 2000 0101 to 2020 0101 (when the ball fell on Times Square), the total returns in US dollars were as follows:

As a multiple:

US TBills: 1.4138

US TBonds: 6.9686

Stocks: 2.8713

Copper: 3.1777

Gold: 5.3200

In percentage terms:

US TBills: 41%

US TBonds: 597%

Stocks: 187%

Copper: 218%

Gold: 432%

Annualized:

US TBills: 1.75%

US TBonds: 10.19%

Stocks: 5.42%

Copper: 5.95%

Gold: 8.72%

Plotted semilog:

To those who get their financial news from mass market media, it may come as a surprise that copper, gold and long term US Treasuries handily outperformed stocks over two decades. It should come as no surprise that outlets aligned with Wall Street prefer to tout Wall Street investments. But here at Financology we have no such outside masters. The actual historical record speaks for itself.

Imagine that … mere chunks of inert metal outreturned stocks over twenty years … the asset class we’re taught to count on for “the long run”. Why? Simple … stocks started out overvalued. This also informs our outlook for the next ten.

In our last installment, Major Trend Review, we briefly discussed our outlook for the next decade. Reversing the order of the past decade, nonUS stocks will power ahead over US stocks. Stylistically, “value” will outperform “growth”. Physical commodities such as copper and gold will outperform US stocks. Why? Valuation. By a variety of measures – price to revenue, price to dividends, price to book, market cap to economic output, investors’ stock allocations – US stocks are historically overvalued. US Treasuries, while more attractive than most other sovereign bonds, are likewise richly priced and unlikely to repeat their outperformance of the past two decades.

These are high confidence long term calls. (Insert graphic of pounding the table). The recently updated Synthetic Systems charts (posted under Market Analysis) are shorter term in nature, and inherently more speculative. I think of the long term outlook as an aid in deciding how much of each asset class to own; Synthetic Systems helps with when to make the adjustments.

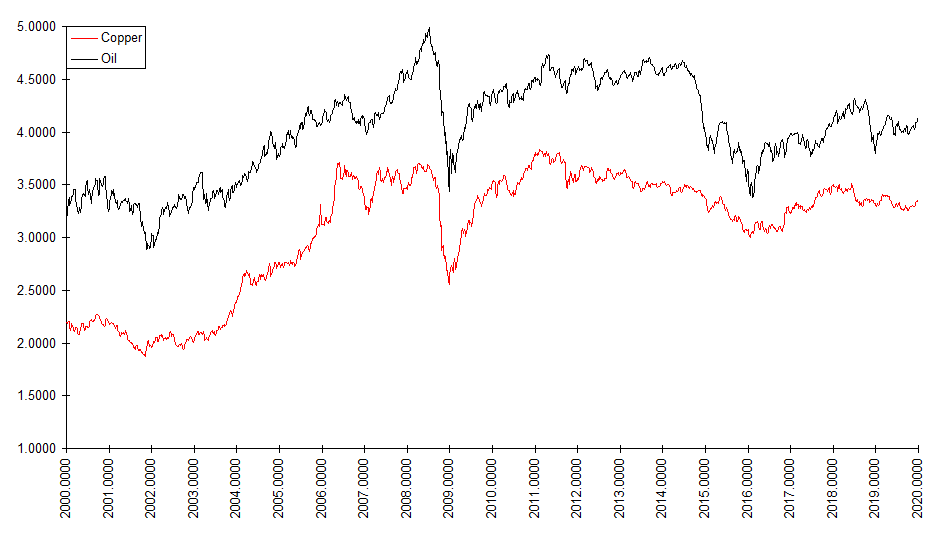

the biggest component, by far, of commodity indices is energy. but of course oil doesn’t have a Ph.D. like Dr. copper. any thoughts on how well your copper projections track with energy prices?

Sure, JK. We can put numbers on it. The raw correlation coefficient of weekly copper and oil (WTIC) prices over the past twenty years – since the beginning of 2000 – is 0.8675 … on a logarithmic basis (more meaningful since it registers halvings or doublings the same) it’s 0.9051. Correlations are a bit tricky though, since they depend on how frequently you sample the data. The correlation rises as you use longer intervals … for example if you use quarterly data the correlation exceeds 0.99. This stands to reason, since as you extend the time frame, commodity price fluctuations are increasingly dominated by changes not in the individual commodities, but in their common denominator – the value of the currency unit you’re pricing them in.

So as the dollar loses value to inflation, dollar denominated physical commodity prices will rise in kind merely by virtue of remaining the same in real terms. BTW my comments aren’t with respect to any particular commodity price index … although some, such as the GSCI, are overwhelmingly energy weighted, others are not. One source, however, that supports the commodities outperformance thesis, Jeff Gundlach at DoubleLine, IIRC cites the energy-heavy GSCI.

In the spirit of a picture is worth a thousand words…

Copper & Oil, log scaled

thanks. your comments are always appreciated.

>US TBonds: 597%

How is the return on bonds calculated to get such a high return? Outside of coupons, what else did the investor do to get such a high return? I seem to recall bond yields never being higher than 7% in any year from 2000 to 2020 so I’m guessing that there is a capital gain component to the return. What tenure of bond did the investor buy and when did he make his trades, if any?

Great question, Milton. This is one of the most commonly misunderstood aspects of bonds. The financial media are to blame, because invariably they will report stock market action in terms of price change (“the Dow was up 247 points today”), but report bond action in terms of yield (“ten year Treasury yields fell 17 basis points”). The cynical among us might suspect a media bias in favor of Wall Street’s most profitable products…

In fact you can report stock action in terms of yield too. And bond action in terms of price. They’re intimately related by hard math. If a security with a $2 annual payout costs $100, the yield is 2%. If the same security happens to trade hands at $50, the yield is 4%.

It doesn’t matter whether it’s a stock or bond. The main differences are that the payout of a stock changes too, so the yield computation is more complex, and that the change in the price/yield relationship of a bond also has time to maturity in the math. The longer the maturity, the bigger the price change that corresponds to a given change in yield.

So your intuition that a big part of that return is due to capital gains is correct. For a long term Treasury bond, the price change nears inverse proportion to yield. Back in 2000, long term Treasuries yielded about 6%. Now they yield about 1%. So there you go … in addition to the yield, you have potential price appreciation approaching six fold.

For a real-world example of long term Treasury returns, pull up a chart of VGLT or TLT. These are funds that hold TBonds from 10-30 years and 20-30 years maturity, respectively. The funds buy and sell the bonds internally as needed to maintain their target maturity ranges. An owner of these funds would only need have bought and held the fund for the duration, or bought a thirty year bond in 2000 and maybe traded it for a new thirty year bond each five-ten years.

I’m still scratching my head over how the 597% return on bonds is calculated over 20 years. I get the funny feeling it’s done by looking up what a bond with a, say, 6.5% coupon and 30 years remaining in 2000 would cost and then looking up what the price of a hypothetical bond with the same 6.5% coupon and 30 years remaining would be priced at in 2020, a year where actual rates are about 1%?

This is kind of a strange comparison to the other assets because a bond, in a sense, fundamentally changes over time because its tenure declines. At maturation, the bond vanishes and the investor gets his principal back.

I must be missing something because if I were able to go back in time and buy a 30-year UST in 2000, collect the coupons for 10 years, sell the bond (now with 20 years left) in 2010, buy a new 30-year bond, collect another 10 years of coupons, and then sell the bond in 2020, I would not have made 597% of profit.

My calculations are for continuous compounding of total return based on the accumulated interest and change in price, modeling a perpetual bond with the yield of the longest outstanding Treasury. https://financology.net/market-forecasts/ The raw yield series can be found at https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield. So I don’t know why one would look “up what a bond with a, say, 6.5% coupon and 30 years remaining in 2000 would cost and then looking up what the price of a hypothetical bond with the same 6.5% coupon and 30 years remaining would be priced at in 2020”, and certainly did not follow that method myself. Nor did I specifically cite 30 year bonds in my post. (On the other hand, a 30 year bond bought in 2000 will still have the same yield on the original price 20 years later, and an additional return due to price appreciation as the yield fell over the duration.)

Returns on 30 year bonds replaced at multiyear intervals would be somewhat less than on continuously compounded perpetual bonds (although returns on zeros could be higher). But we have real world long UST bond index funds that show returns also exceeding real world stock index funds. TLT, for example, would do, but TLT did not exist until July 22, 2002. Even so, the annualized return on TLT since inception as of yesterday given by Morningstar is 7.51%, and this excludes the period from 2000 0101 until 2002 0722, in which starting yields fell from 6.61% to 5.40% (and in which stocks were in a bear market). Given that TLT has a stated expense ratio of 0.15% and includes maturities as low as 20 years, the return on the underlying bonds was 7.66%, and the longest of those bonds higher still. Even without including the higher returns of the first two and a half years, the return for 30 year bonds was still well in excess of the returns on stocks.

It’s true that as fixed income, fixed maturity securities, bonds are different than stocks, but even the S&P 500 does not contain the same stocks in 2020 as in 2000. So they are similar in that to construct an index of returns, one cannot simply start with a set of securities and assume they’re held over a long period of time. In both cases, the securities originally “bought” have to be “sold” and replaced with others. With Treasuries, you could buy one and replace it anywhere from every second to every decade or more. With stocks, you have similar considerations. So there are always some assumptions involved in specifying returns on things described broadly as “stocks” or “bonds”.