For the past couple of years or so, Financology has been circling one core economic and financial theme. We’ve looked at it repeatedly from multiple angles, but not really connected them to highlight their common core. Here we’re going to review it again, to tie them together into a single 360° view, and because it is so, so critical for understanding the economic environment we’re in and how to invest successfully through it.

One such angle is the idea that investment assets do not exist outside the world of inflation and that rising asset prices are every bit as much a symptom of inflation as rising consumer prices. Quiescent consumer prices do not excuse easy money policy. We recently fleshed out this theme in It’s Been Inflation All Along.

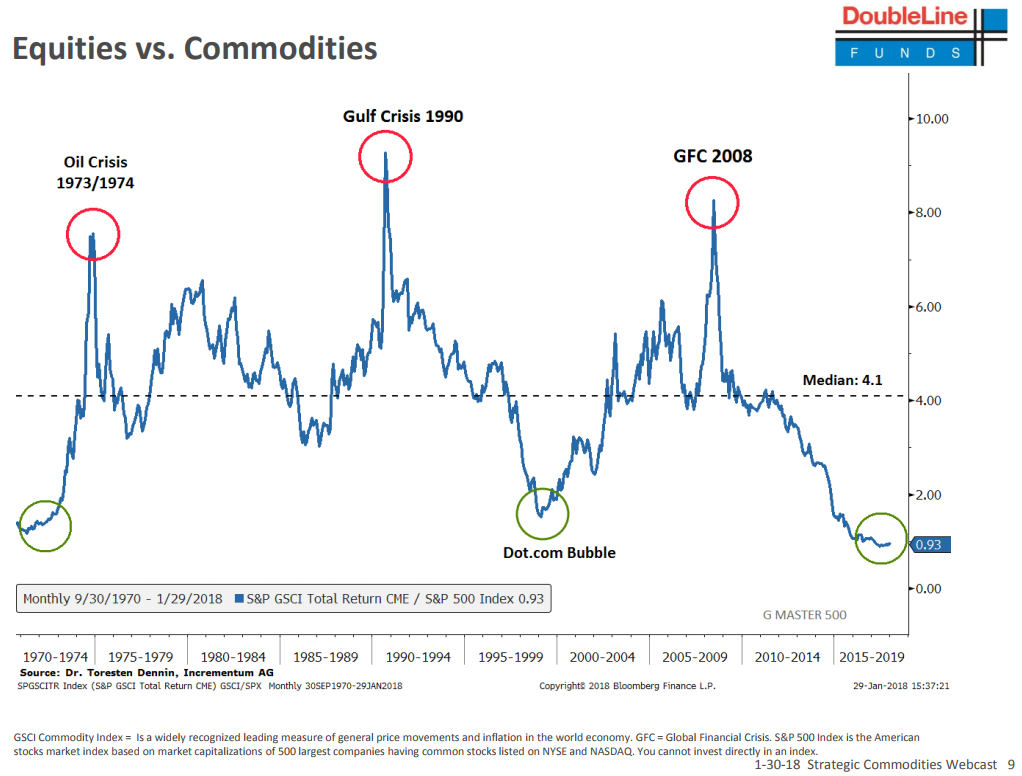

Another angle is the relative valuations of financial and real assets. Or more precisely, things which are used as investment assets and which derive their value from future cash flows versus those with current utility value, like physical commodities. On the basis of relative valuations of stocks versus commodities, we were able to observe at the beginning of this decade that the relationship had gone far out of whack and predict they would revert in the 2020s. See our analysis in Outlook for the 2020s and Commodities & NonUS Stocks, where we cited the following chart.

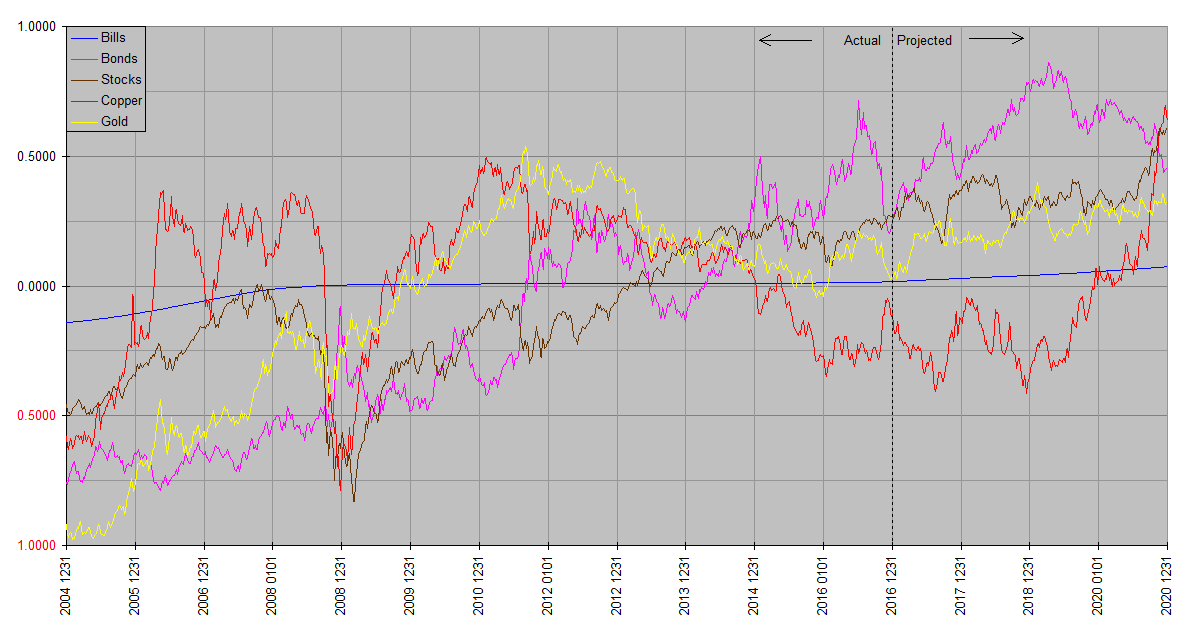

We complemented this valuation analysis with a more technical view via our Synthetic Systems computer model. At the beginning of 2017 this model first predicted the 2020 appearance of rapidly rising commodity prices and consumer price inflation, via the rising Copper plot:

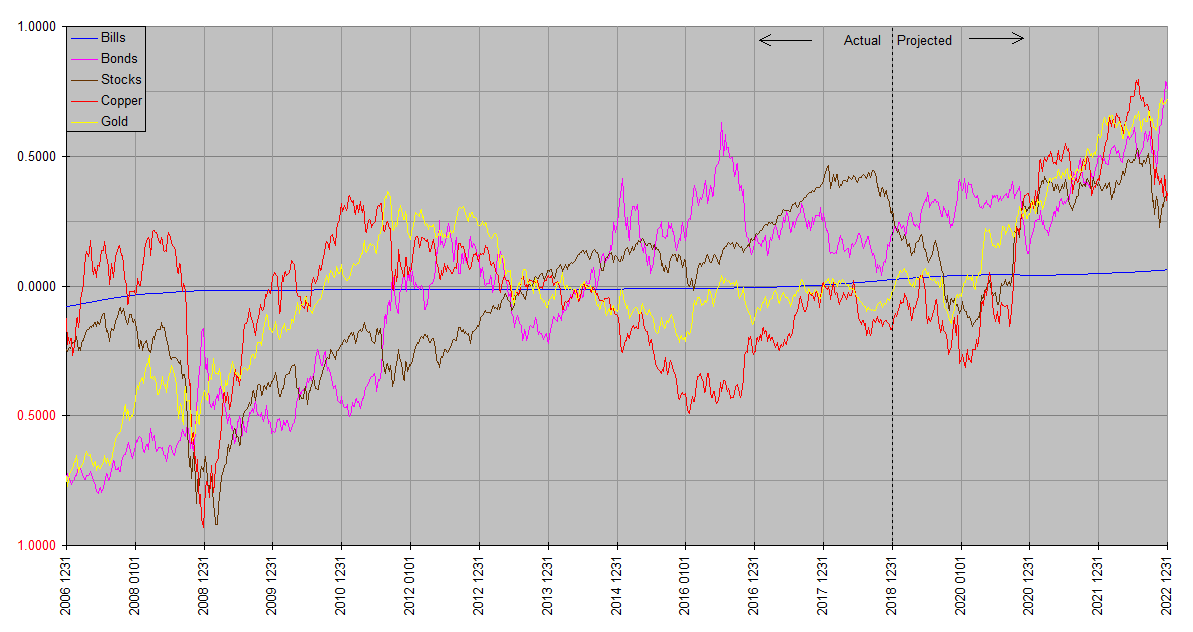

Two years later in 2019, it continued to project soaring commodity prices and inflation in 2020-2021.

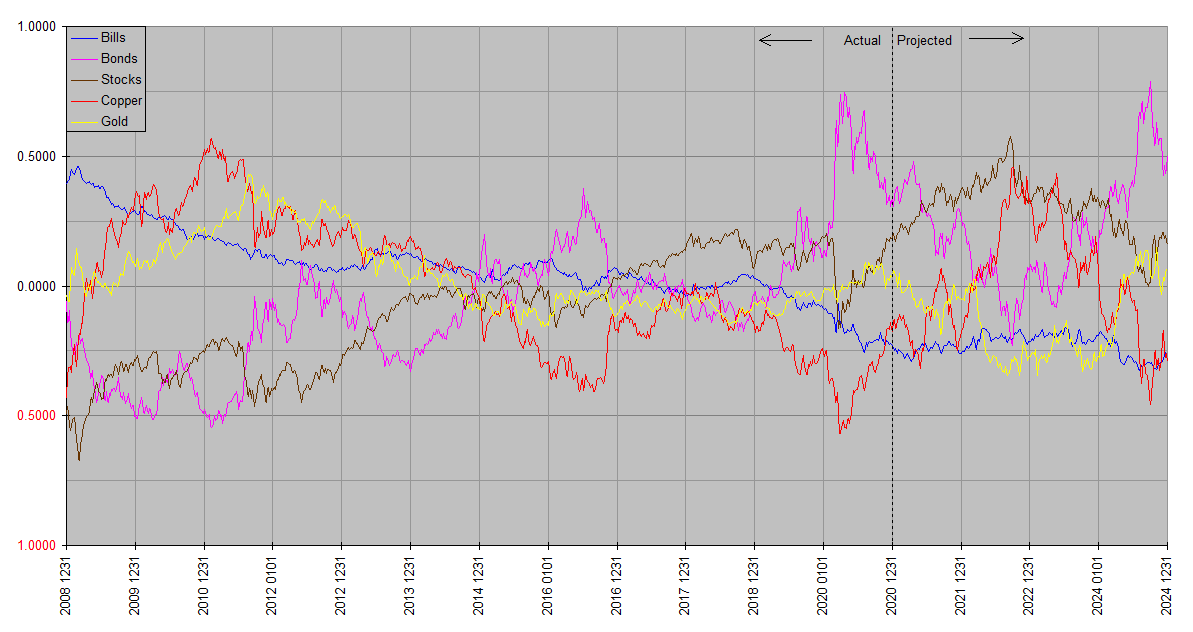

It again highlighted the emergence of rising commodity prices at the beginning of 2021:

There are some important corollaries to this. One is that the narratives the corporate media treat you to on a daily basis are grossly misleading. Prime among them is the fallacy that inflation has been caused first by Covid-induced “supply chain disruptions” and then by Russia’s invasion of Ukraine.

Wrong. The cause of inflation predated both Covid and the Ukraine war. If it didn’t, how could Financology have seen it coming as early as 2017? As its designer, I can tell you with absolute certainty that Synthetic Systems knows nothing about viruses, pandemics or war. None of our fundamental analysis foresaw either of those developments either. The cause is really bad economic policy, especially among the world’s central banks. Financology has said so outright and repeatedly. The false narratives promoted by the media are worse than useless, or these same media would also have been able to see this coming. Covid and the war are scapegoats for the miserable failure of US government policy to do anything but enrich the powerful at the expense of the welfare of the general public. If anything the responses to them – reckless monetary and fiscal policy – have only accelerated the problem. For instance in its response to Covid, the Fed hammered interest rates down to zero and printed trillions of dollars, ostensibly to “support the economy”. That has been all but forgotten in most current reporting on the inflation crisis.

Do not trust media narratives that blame spooky alien nanobots or foreign powers for our economic problems. They’re Made in the USA.

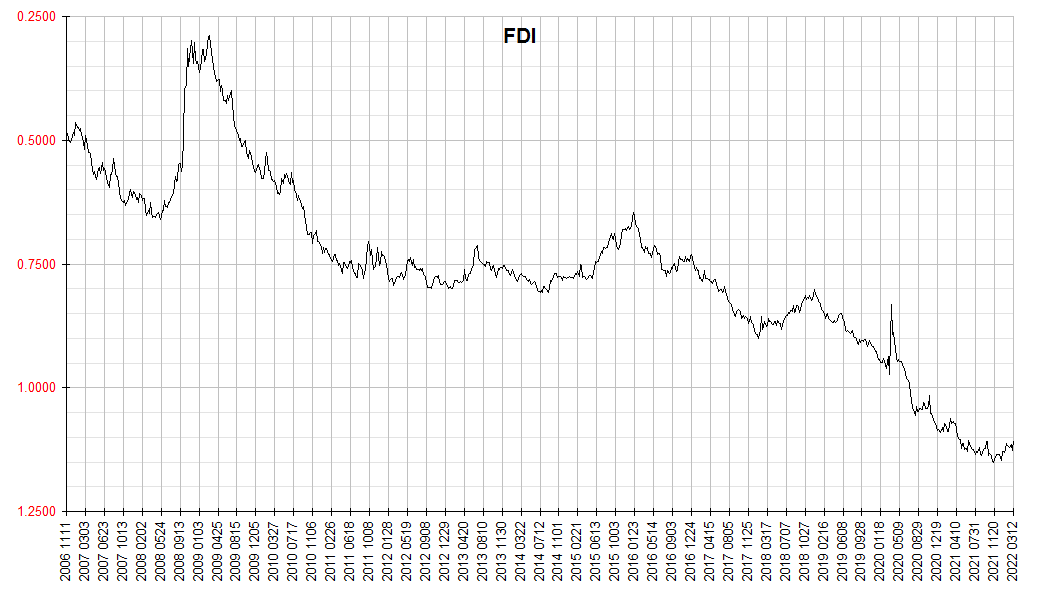

Another angle of approach is via the Financology Dollar Index. Updated today, here is the latest chart. The big “inflation” news this week is that the CPI has risen 7.9% year over year. Consumer price inflation is accelerating. The dollar is rapidly losing purchasing power in the world of US domestic goods and services. The FDI indicates however that recently, overall, the dollar is if anything modestly increasing in value. Put another way, inflation is not increasing … it’s moving from the realm of asset prices to consumer prices.

The Fed is on the case, but it is years too late. As we have been saying all along, the purchasing power stored in assets cannot exceed the body of goods and services available for purchase. So there is only one possible outcome from years of asset price inflation. Either asset prices must come back down or consumer prices must rise to meet them. Or some messy combination of both.

That’s exactly what we’re seeing now.

“the purchasing power stored in assets cannot exceed the body of goods and services available for purchase.”

————————————————

can the purchasing power in assets put a call on the future manufacture of goods and services?

If I understand the question right, yes. From the point of view of the buyer, assets are a way to store purchasing power for future use.

Take for example the very common asset issued by the US Federal Reserve, the US dollar. You exchange your labor for a sum of these securities. You put them in your bank account and wallet, where they represent claims on consumer goods and services. You are using these securities as assets to store value.

But because the government, via the Federal Reserve and banking system, creates more of these securities – without creating more goods and services like you did when you earned them – they lose value. For this reason they’re unsuitable for storing value for very long.

So we turn to other securities, such as those issued by corporations. Common stocks for instance. Businesses do produce goods and services, so their securities can potentially store value better. If dollars depreciate while these corporate securities don’t, the corporate securities rise as measured in depreciating dollars. They appear to appreciate. Along the way, because the corporations can earn profits on their productive enterprise, you may even be paid a return in the form of dividends.

The first part – the apparent rise in value due to a depreciating unit of measure – is not a real increase. It’s asset price inflation. It usually roughly keeps pace with the inflation in the products the economy produces. But aggressive monetary policy can cause asset price inflation to far exceed the real goods and services the economy produces. In this case the amount of apparent value stored in such assets can far exceed the value of actual stuff that can be bought with them.

It is this mismatch between the value investors think they have stored in assets and the actual value they can buy with them that results in crises of the kind I refer to in the penultimate paragraph of this post:

Either asset prices must come back down or consumer prices must rise to meet them. Or some messy combination of both.

That’s exactly what we’re seeing now.

Hey Bill,

As you have stated, you are no EJ, but when EJ’s in hibernation, you’re an excellent replacement. Once again, thanks for the above post, it helps to keep at least one other person in this world grounded economically, and to see through all the smoke and mirrors.

Peter

Thanks Peter. I think of my analysis as complementary to the kind EJ does, as opposed to an alternative. But I try to cover the bases either way. Glad you find something of value in it … and thank you for your comments!

This is great analysis Bill, thank you.

Another correlation that I observed and trying to get my head around is the inverse relationship between bonds and commodities (represented by copper) in the SS charts. This is punctuated by short timeframes where they move together either up or down around the time when they swap directions.

Can you please elaborate on the mechanism that drives this relationship?

Thanks for your continuing insights – clarifying the noise and confusion surrounding finance and investment!

Thanks Sunpearl … great question. I’m not sure I have an adequate answer. In fact bonds and commodities do tend to trade inversely over at least over medium time frames. My guess is that it springs from their inherently different characteristics. Commodities – particularly industrial commodities like copper – outperform in the later phases of the inflationary cycle. As I discussed above, inflation first shows up in asset prices. Bond prices rise first as the Fed cuts interest rates and buys bonds. Stocks follow. Late in the cycle commodity prices rise, if only because that’s when it becomes acknowledged as inflation. At this point, the Fed finally begins to move into tightening mode, raising interest rates and ceasing to buy bonds if not outright selling them.

This makes it sound simpler than it is though, because throughout the cycle there are mini-cycles where bonds and commodities trade inversely. So it’s not just monetary policy. The value of bonds depends on the future value of the currency they’re denominated in, so when markets sniff out inflation – which tends to raise commodity prices – they also begin to factor in a lower value of the currency in which their bonds will be repaid. So industrial commodities and bonds inherently respond inversely to perceptions of trends in the value of currency. This is probably the main driver of that tendency to trade inversely.

Yet this is still not the full story because gold is a commodity too, but marches to a different drummer. Investors tend to use it as a bond alternative. So gold actually has a tendency to correlate with bonds; at least much more so than copper. My earlier versions of Synthetic Systems used a single gold and copper composite commodity series; but the starkly different patterns in industrial and monetary commodities ultimately led me to treat them separately. Silver and platinum, incidentally, are intermediate in nature, so their behavior is more in line with a combination of the gold and copper plots.

Finally, notice that in the SS versions prior to 2020, the Bills plot is smooth. My original version of SS plotted each asset class in terms of a weighted mean. Several years ago, in an attempt to make them easier to read, I switched to a dollar denominated model. This resulted in the Bills plot being smooth, because TBills are nonvolatile in dollar terms. This however came at the expense of accuracy. So in 2020 I switched back to plotting each asset class in terms of a weight mean.

So what does this have to do with your question? The weighted mean basis actually further emphasizes the contrary behavior of the individual asset classes. If for example there were only two plots, and they were each plotted relative to the mean, they would be perfect mirror images of each other, like a mountain range behind a lake and its reflection. Just because of the math. Obviously this doesn’t account for the contrary behavior of Copper and Bonds, because it shows up in charts using both methods, and because it doesn’t show up in the other asset classes even plotted using the weighted mean, but it’s there and has to be acknowledged. Another interesting implication of the weighted mean method is that if the same weightings were used to plot a weighted sum of each plot, the result would be a flat line at zero.

So what about those brief periods in which Bonds and Copper trade in parallel? Again, I’m not sure I have a complete answer, but any time all asset classes seem to be moving in sync, check the unit you’re using to price them. A stable unit of value just doesn’t exist in finance. If for instance the dollar declines in value, all assets appear to rise. And vice versa (as in 2008). When “correlations go to one” you can bet that’s behind it. This is a key reason for the use of the weighted mean instead of dollars in the vertical axis … the latter completely ignores the fact that dollars themselves fluctuate in value. But it also means that this factor does not fully explain the occasional covariant behavior of Bonds and Copper. Maybe it’s just necessary for markets to break pattern once in a while so as not to be too predictable … easily predictable markets are an impossibility because then everyone could get rich trading!

Thank you for the detailed response Bill, much appreciate it.

I appreciate your answer Bill. Actually, I prefer assets that produce purchasing power for current use, whether through current deployment or saving, and that have an expectation of producing future purchasing power. At one time, when interest rates weren’t being suppressed, the dollar served this function. It could be lent at interest.

The basis, along with land, of a rentier economy?

Who is EJ?

CB, the only thing that produces purchasing power is production. You can’t buy what isn’t produced. If for instance you want a dog house you have to produce it. Or produce something you can exchange for it.

Or produce something, receive an asset in exchange for it, then exchange the asset for the dog house. In which case the asset stores purchasing power.

This last way of course is how an economy operates. The asset is normally currency, but the currency can be exchanged for another asset, which can then be exchanged for currency at a later time, and finally the currency is exchanged for goods and services. This is how retirement works.

But through whatever route, there is no purchasing power without production.

The complete failure of economic policy over the past couple of years is because policymakers failed to take into account this most basic of principles. They shut down businesses that produce things, and tried to fill in the hole by creating and handing out currency.

This was done in the name of “supporting the economy” … as if currency had some innate purchasing power in it.

But of course it doesn’t, so the only possible way for anyone to benefit from it would have been at the expense of others.

I’m not sure what you have in mind by assets that produce current purchasing power, but with the above in mind can you clarify? You cite currency as an example, but as we have seen it is not possible for currency to produce purchasing power of any kind. If you dig beneath the surface, you’ll find that even with dollars lent at interest, the purchasing power is actually coming not from the currency itself, but from somewhere else.

EJ is Eric Janszen, proprietor of economic and finance site iTulip.com

Is a dollar, lent out and earning interest, producing for the lender who receives the interest? or, is the interest received just “stolen” from productive activity?

Is the borrowed dollar producing for the borrower, who uses the dollar to buy raw materials, and forms those raw materials to create and sell a product for a price to exceed the dollar and interest on the borrowing of that dollar?

Neither the dollar nor the interest produce anything. Only production creates purchasing power.

The dollar is a claim on production. Interest on dollars is paid in dollars, and those dollars too are claims on production.

Take care not to confuse real things of value and claim tickets for real things of value. The dog house we referred to before is a real thing; the dollars paid for it are claim tickets.

Interest paid on dollars is consideration for use of those dollars. The borrower presumably receives some benefit for the temporary use of those dollars, and the lender makes some sacrifice for temporarily foregoing the use of the dollars. The interest is how the borrower compensates the lender.

It’s no different in principle from a tenant paying a landlord rent for the use of an apartment. Or the interest paid on a bond or dividends paid on a stock.

But just so there’s no confusion, this doesn’t have anything to do with the nature of assets as a means to store purchasing power. The dollar itself is an asset, as is a bond, as is a share of stock. These things are held as a means of allowing one to trade something of intrinsic value for another thing of intrinsic value, but not be bound to receive the second thing at the same time as he gives up the first.

The asset allows value to be stored for later use.

“the purchasing power stored in assets cannot exceed the body of goods and services available for purchase.”

This statement is mind-boggling. Very clever. If true, brilliant. Requires a lot of thought to think through.

Consider an nice affordable sea-front property in a rural area. Over the next ten years that particular property becomes very expensive, substantially exceeding the rate of inflation. I am not recognizing what the purchasing power stored in that asset has to do with the body of goods and services available for purchase?

We never said assets can’t change in value. In fact that’s one of their key features. Dollars do, bonds do, stocks do. But the fact that assets change in value has no heuristic value for the purposes of illustrating the point. It’s a complication best addressed once the basic principle is well understood.

Your example of the seafront property is further complicated by the fact that it is not a claim on real things, but is a real thing that has intrinsic value in itself. Real assets include things like commodities, real estate and collectibles. This is in contrast to financial assets like currency, bonds and stocks that derive their value indirectly from real things.

My statement about the purchasing power stored in assets is best understood in the context of our discussion of inflation … that money printing that inflates asset values but hasn’t yet inflated consumer prices is inflation all the same, and that ultimately that divergence must be reckoned.

So we’re not talking about any particular asset … we’re talking about assets in the aggregate.

The Fed’s monetary excesses inflated the US stock market by a factor of six over the course of fourteen years … far in excess of the productive capacity of the economy. The Fed pretended inflation was low because consumer prices were quiescent. It doesn’t recognize asset prices in its assessment of inflation. My point is that that was catastrophic error leading to the present crisis, and that this reconnecting between asset prices and consumer prices has major implications for investors.

Bill said: “Neither the dollar nor the interest produce anything. Only production creates purchasing power.”

———————————–

Note

Bill said: “Neither the dollar nor the interest produce anything. Only production creates purchasing power.”

_______________________________

Part 1

Provocative. Allow me to think out loud.

Is this a play on words? Must we distinguish the words – create vs exist vs manage vs provide vs receive vs transfer?

Is purchasing power inherent in the land? Is it inherent in ownership of the land? Will the land, unmanaged, produce a level of production and shelter? Will this provide purchasing power to an owner of that land?

Does an owner of dollars, who puts his dollars “to work” produce anything?

Does a person of wealth who rents their assets, or receives dividends from stock they own, produce anything?

Does a bank create purchasing power when it creates dollars to extend a loan to a borrower? Does that fraud not produce? Is that not a service to the borrower?

Must we distinguish between gross system wide purchasing power and individual purchasing power.

Must we distinguish the difference between creating purchasing power, earning purchasing power, meriting purchasing power, attaining purchasing power, holding purchasing power, storing purchasing power, etc.

Production produces something. Purchasing power from production is a function of the distribution, generally dollars, that comes from selling or renting those things produced. This distribution is generally between owners, employees, vendors, suppliers, lenders, consultants and lawyers, and the taxing authorities. So, the ultimate purchasing power goes to owners, employees, rentiers (land and money renters), and government (and it’s beneficiaries).

It’s not a mere play on words. It’s an axiom.

To best understand, consider it in the context in which occurs. If it were sufficient on its own to be understood, I could have posted it as a standalone article … but of course it isn’t and I didn’t. Would we expect a skeleton to eat, breathe and think?

So my answer is to re-read the statement in the full context in which it appears.

As an axiom, it should be acceptable as obvious, if not trivial. Put a dollar on the table in front of you. Watch it for hours, days, weeks … years … does it produce anything?

Turning back to my example of a dog house, the act of building it creates a dog house capable of being purchased. Without that act of producing a dog house, there is no possibility of purchasing one.

It is the production of the dog house that created the power to purchase one.

“the purchasing power stored in assets cannot exceed the body of goods and services available for purchase.”

————————————————

Let’s think about this statement for a minute.

We have in this country, infrastructure that has been built over centuries. We have buildings and housing that have been built over decades. Same for businesses and those structures used to support those businesses. We have colleges, churches, medical and other institutions.

The asset value for all of this is great.

Is a house not worth more than the current rent it produces?

Recall my admonition about taking the statement in context. It’s not amenable to interpretation as an isolated abstraction.

Cash, bonds, stocks, etcetera are used by almost everyone as claims on production … to store purchasing power to buy things with. They’re in their wallets, bank accounts, brokerage accounts, IRAs & 401(k)s. Colleges, churches, hospitals … aren’t.

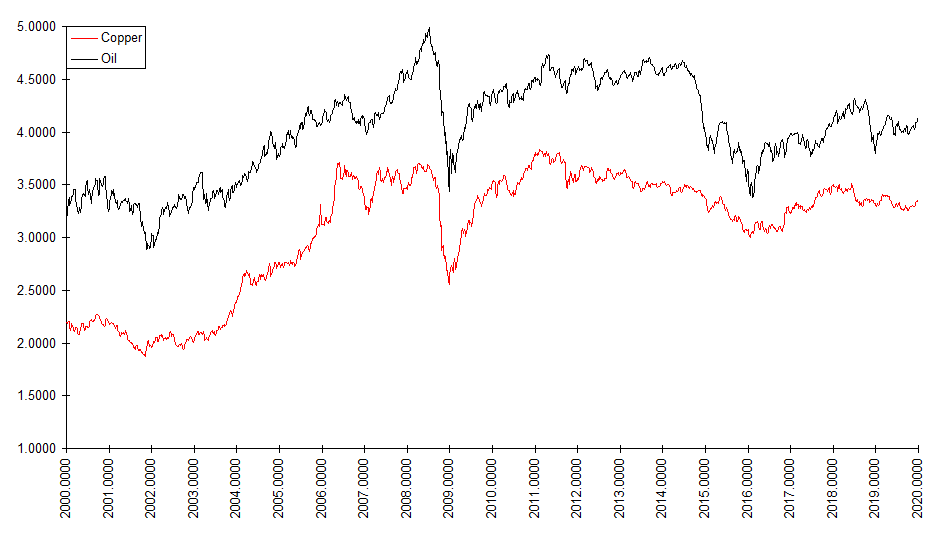

I noticed no mention of oil, is it just to be included in aggregate to other commodities? I would think since oil bolsters the production of all other commodities that it would garner attention on its own merit.

Good point, Rick. No question oil is a key commodity. Synthetic Systems uses copper as a proxy for physical commodities as a class for several reasons. Unlike oil, as an elementary commodity it is neither created nor destroyed … the planet’s stock is fixed … it’s a quintessential “hard” commodity. We can’t run out of it or convert anything else into it short of nuclear transmutation.

It’s also less subject to political manipulation … for instance the US Strategic Petroleum Reserve is often used to deliberately manipulate the price of oil.

Oil is also quoted in different grades which change in fungibility due to technology, for instance the processing of heavier more sour crude.

Oil prices are also surprisingly closely correlated with copper prices. While they may diverge on a daily, weekly or even monthly basis, over longer periods their price patterns converge, as can be seen in the twenty year chart below. Between the two, copper is just less “noisy” and helps make SS forecasts more reliable overall. We discussed the correlation issue in detail in Outlook for the 2020s (see comments section).

Copper & Oil, log scaled

Like most people’s writings, This article seem heavy on saying why things are wrong and bad but offers no options that would have been better.

I’d love to read it re written with what the right things would have been instead, and what results would have followed from doing the right thing.

Too often the complain is just that it wasn’t perfect (even when no better option existed).

Thanks for weighing in, Dave. Some other articles have been more prescriptive, for example in calling for the Fed to refrain from interest rate targeting and to limit its quantitative policy to buying and selling Treasuries and gold. Here I also suggest that policymakers broaden their consideration beyond consumer prices in their reckoning of inflation. I’ve tried to focus on what is actually happening as well to help serve as a road map for investors coping with the present and likely status quo.

But where I’ve left gaps, you’re welcome to fill in with your own ideas … please feel free to contribute in this space!

According to a report on Bloomberg, Bill Dudley said today that in order to get inflation down, the Fed needs to force bond and stock prices down. This would be the first recognition I’ve heard by any other economist of a point I’ve been making for years and the thesis of this post.

If Stocks Don’t Fall, the Fed Needs to Force Them

https://www.bloomberg.com/opinion/articles/2022-04-06/if-stocks-don-t-fall-the-fed-needs-to-force-them

This is big news, folks … I think this will factor into the Fed’s policymaking … that ultimately the Fed will actively seek to force asset prices down.