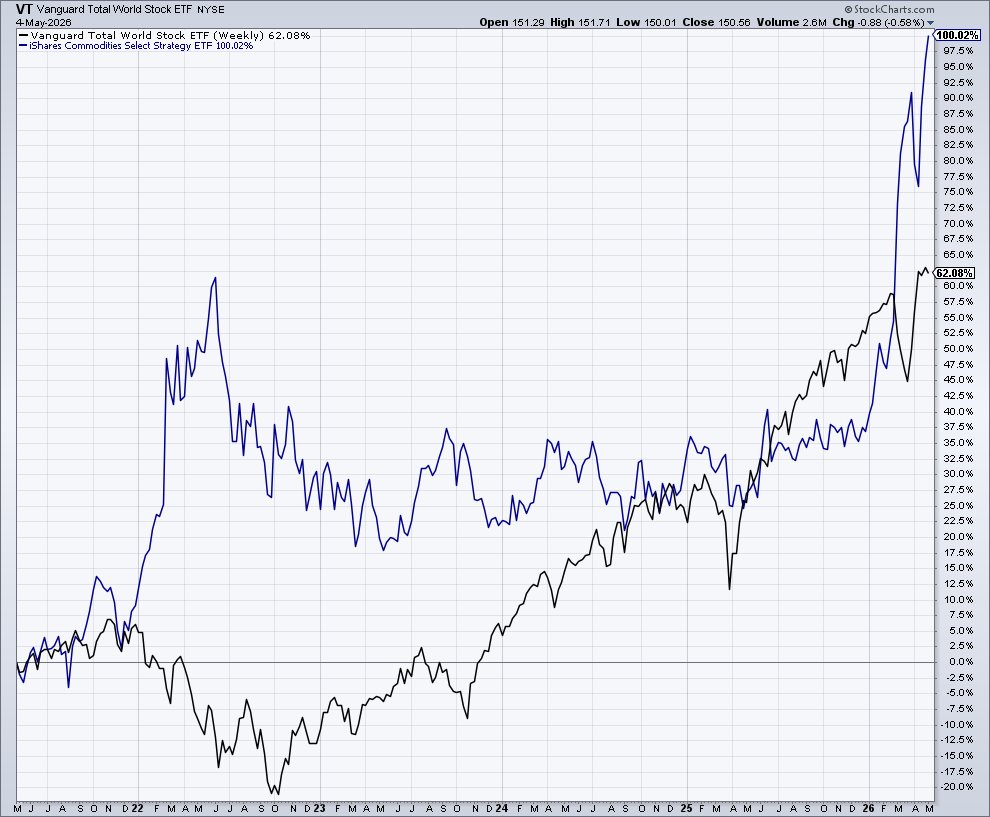

Which has returned most over the past five years?

We know commodities have had a great run lately, but how about over the longer term? Commodities (COMT) have now outperformed stocks (VT) by nearly 40% over the past five years. The chart is of total returns, accounting for dividends. So had you put $10,000 into either COMT or VT five years ago, you would have come out ahead in COMT. $20,002 versus $16,208.

But this is not to suggest that you should have, let alone should now. Because fortunately the world doesn’t force us to choose one or the other. As the chart indicates, COMT was lumpier over the time frame as compared to VT, with its returns concentrated in fewer time periods. But those returns also tended to come when VT was weak. A mix of the two, say 3:1 VT:COMT, would have both outperformed stocks alone and provided a steadier more reliable ride to boot. Add some treasuries (GOVT) and gold (IAU), and you have a complete portfolio.

What about the S&P, with its higher concentration of the Mag 7, by the way? It was beat by commodities too, (VOO) returning 82.70% over the same time frame.

In case you missed it …

Our friend Mega has posted some of his best work – Mega’s Dispatch From England – here. You can catch all four episodes of his latest installment at any of the following links:

https://financology.net/2026/04/08/geopolitics/#comment-9679

https://financology.net/2026/04/08/geopolitics/#comment-9681

https://financology.net/2026/04/08/geopolitics/#comment-9690

https://financology.net/2026/04/08/geopolitics/#comment-9691

“I’m not saying to go out and sell all your pricey stocks. What I’m recommending is diversifying into alternative investments. Natural resources, emerging markets, and precious metals.”

A point in favor of diversifying commodities investments beyond metals and energy.

Excellent explanation, thanks!

Investors should pivot from tech to commodities ahead of a new ‘supercycle,’ top economist says

“”Even artificial intelligence is not purely digital,” he said. “It requires power, data centers, cooling, land, steel, copper, gas, and grid capacity. Those things super charge the demand for commodities, and the relative return profile of commodities versus tech.””

May be a little late to the party – we’ve been on this since last year – but could be correct that there’s much more to come.

“”I have always preferred exposure to commodities via the futures markets,” he said. “In short, if you think crude is going up, do not worry about the complexities associated with analyzing a particular oil company; just go long crude in the futures markets.””

If you want to invest in commodities, buy the commodities.

I also want to point out that in the big picture, the tech boom and the war are way stations in the inflation chain. The inflation started years ago, and is still working its way from its easy money origins through asset bubbles and finally to commodities and consumer prices. Financology 101.

As I’m already eyeballs deep in commodities(especially gold and to a lesser extent oil), I’m starting to look at Berkshire Hathaway(BRK) as a medium to longer term prospect.

BRK is lagging S&P YTD, 1yr, and 2yr.

This tends to happen when the S&P is driven by euphoric and narrow valuations.

BRK tends to lag narrow speculative tech booms( and the narrow-ish Nifty 50 oil booms), and win the aftermath(usually, but not always…. ie GFC).

BRK tends to win the recovery.

Thinking ahead 6-24 months, I’m wondering if BRK may be a strong prospect to consider rotating into when it’s time to start rotating out of gold/oil?

If BRK-B hits the low $400’s or high $300’s.

$400B in cash/treasuries, businesses with durable earnings, and blue chip equities.

My biggest concern is, will it be able to deploy that $400B?

Thoughts on it as a prospect for the post-Gold/Oil/Commodity medium to long term?

First a quick commodity caveat … timing can be a bitch. We were fortunate to have anticipated both the runup in gold and its denouement, and are on guard with energy and ag too … allowing for the possibility that this rapid rise serves a similar bubble busting role as in 2008. Or that there might be a pullback in the context of a longer rise. It’s fair to say we’re generally bullish on commodities, especially relative bubble assets, but even more so that we’re in favor of diversification. I’m a strong believer that just stocks and bonds never made a complete portfolio.

Some of the same things could be said of Berkshire Hathaway, especially the part about it looking good next to bubble assets. Though no single stock can be an all weather investment, it’s about as close as you can get. It would be even closer if it weren’t for Buffett’s antipathy towards gold. It’s cost Berkshire billions.

It’s a bit out of favor now, a good thing for prospective buyers. I have some exposure if only through index funds. But if I were looking to boost that, I would probably be accumulating bit by bit now and let its management make the investment it calls it does best. Buffett himself (as well as Munger), may be no longer running it, but I’d be confident they’re leaving it in good hands.

Six Flags – Cedar Fair (FUN) update.

I really hope the “sell off the real estate and become a tenant of the same real estate” ends forever. In my opinion, it’s nothing but a grift that gooses management’s bonuses and traders of the stock. Long term, it’s a disaster for everyone.

I’ve been watching defaults in the commercial real estate market and the write-downs make my jaw drop and even more jaw-dropping to me is how many of these defaults there are. I regularly see write-downs of 70% up to 90% on commercial real estate and I think to myself, “We hear incessant whining from businesses about needing tax breaks, new sports arenas, unlimited immigration of incompetents, reduced environmental protections, and even a weaker dollar lest we become ‘non-competitive’ with the rest of the world. However, wouldn’t reducing the real estate rents of companies by 50% or more make the U.S. quite a bit more competitive? And the best part of it is that it is not paid for through taxes; it would be funded by taking away the excessive economic rent of the landlords.”

I’m certain some of the biggest commercial real estate holders (we all know who they are so I won’t bother mentioning names) are lobbying for massive interest rate cuts or bailouts. I hope they get wiped out instead.

Rental and lease arrangements make sense when the tenant isn’t committed to long term occupancy. Amusement park real estate isn’t that kind of thing. The property is developed for the purpose. You don’t just pick up and move your amusement park whenever you feel like it. Your profitability is intimately linked with your capital. Land has returns of its own. Selling its land and renting it back just passes those returns on to another party. A few activists might make a quick buck off the transition, but at the expense of long term owners.

A bit of a change in dynamic showing in recent trading, including today. Gold (IAU) and broad commodities (COMT) have been trading contrary … but that pattern has broken.