Which has returned most over the past five years?

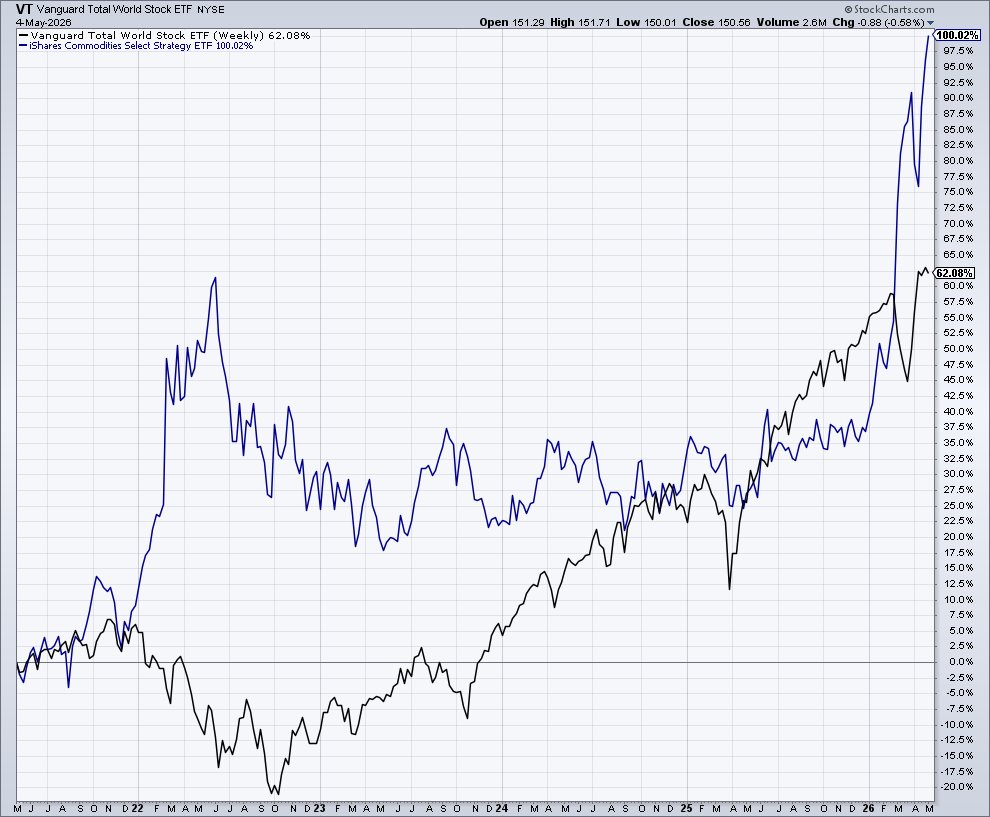

We know commodities have had a great run lately, but how about over the longer term? Commodities (COMT) have now outperformed stocks (VT) by nearly 40% over the past five years. The chart is of total returns, accounting for dividends. So had you put $10,000 into either COMT or VT five years ago, you would have come out ahead in COMT. $20,002 versus $16,208.

But this is not to suggest that you should have, let alone should now. Because fortunately the world doesn’t force us to choose one or the other. As the chart indicates, COMT was lumpier over the time frame as compared to VT, with its returns concentrated in fewer time periods. But those returns also tended to come when VT was weak. A mix of the two, say 3:1 VT:COMT, would have both outperformed stocks alone and provided a steadier more reliable ride to boot. Add some treasuries (GOVT) and gold (IAU), and you have a complete portfolio.

What about the S&P, with its higher concentration of the Mag 7, by the way? It was beat by commodities too, (VOO) returning 82.70% over the same time frame.

In case you missed it …

Our friend Mega has posted some of his best work – Mega’s Dispatch From England – here. You can catch all four episodes of his latest installment at any of the following links:

https://financology.net/2026/04/08/geopolitics/#comment-9679

https://financology.net/2026/04/08/geopolitics/#comment-9681

https://financology.net/2026/04/08/geopolitics/#comment-9690

https://financology.net/2026/04/08/geopolitics/#comment-9691

“I’m not saying to go out and sell all your pricey stocks. What I’m recommending is diversifying into alternative investments. Natural resources, emerging markets, and precious metals.”

A point in favor of diversifying commodities investments beyond metals and energy.

Excellent explanation, thanks!

Investors should pivot from tech to commodities ahead of a new ‘supercycle,’ top economist says

“”Even artificial intelligence is not purely digital,” he said. “It requires power, data centers, cooling, land, steel, copper, gas, and grid capacity. Those things super charge the demand for commodities, and the relative return profile of commodities versus tech.””

May be a little late to the party – we’ve been on this since last year – but could be correct that there’s much more to come.

“”I have always preferred exposure to commodities via the futures markets,” he said. “In short, if you think crude is going up, do not worry about the complexities associated with analyzing a particular oil company; just go long crude in the futures markets.””

If you want to invest in commodities, buy the commodities.

I also want to point out that in the big picture, the tech boom and the war are way stations in the inflation chain. The inflation started years ago, and is still working its way from its easy money origins through asset bubbles and finally to commodities and consumer prices. Financology 101.

As I’m already eyeballs deep in commodities(especially gold and to a lesser extent oil), I’m starting to look at Berkshire Hathaway(BRK) as a medium to longer term prospect.

BRK is lagging S&P YTD, 1yr, and 2yr.

This tends to happen when the S&P is driven by euphoric and narrow valuations.

BRK tends to lag narrow speculative tech booms( and the narrow-ish Nifty 50 oil booms), and win the aftermath(usually, but not always…. ie GFC).

BRK tends to win the recovery.

Thinking ahead 6-24 months, I’m wondering if BRK may be a strong prospect to consider rotating into when it’s time to start rotating out of gold/oil?

If BRK-B hits the low $400’s or high $300’s.

$400B in cash/treasuries, businesses with durable earnings, and blue chip equities.

My biggest concern is, will it be able to deploy that $400B?

Thoughts on it as a prospect for the post-Gold/Oil/Commodity medium to long term?

First a quick commodity caveat … timing can be a bitch. We were fortunate to have anticipated both the runup in gold and its denouement, and are on guard with energy and ag too … allowing for the possibility that this rapid rise serves a similar bubble busting role as in 2008. Or that there might be a pullback in the context of a longer rise. It’s fair to say we’re generally bullish on commodities, especially relative bubble assets, but even more so that we’re in favor of diversification. I’m a strong believer that just stocks and bonds never made a complete portfolio.

Some of the same things could be said of Berkshire Hathaway, especially the part about it looking good next to bubble assets. Though no single stock can be an all weather investment, it’s about as close as you can get. It would be even closer if it weren’t for Buffett’s antipathy towards gold. It’s cost Berkshire billions.

It’s a bit out of favor now, a good thing for prospective buyers. I have some exposure if only through index funds. But if I were looking to boost that, I would probably be accumulating bit by bit now and let its management make the investment it calls it does best. Buffett himself (as well as Munger), may be no longer running it, but I’d be confident they’re leaving it in good hands.

Six Flags – Cedar Fair (FUN) update.

I really hope the “sell off the real estate and become a tenant of the same real estate” ends forever. In my opinion, it’s nothing but a grift that gooses management’s bonuses and traders of the stock. Long term, it’s a disaster for everyone.

I’ve been watching defaults in the commercial real estate market and the write-downs make my jaw drop and even more jaw-dropping to me is how many of these defaults there are. I regularly see write-downs of 70% up to 90% on commercial real estate and I think to myself, “We hear incessant whining from businesses about needing tax breaks, new sports arenas, unlimited immigration of incompetents, reduced environmental protections, and even a weaker dollar lest we become ‘non-competitive’ with the rest of the world. However, wouldn’t reducing the real estate rents of companies by 50% or more make the U.S. quite a bit more competitive? And the best part of it is that it is not paid for through taxes; it would be funded by taking away the excessive economic rent of the landlords.”

I’m certain some of the biggest commercial real estate holders (we all know who they are so I won’t bother mentioning names) are lobbying for massive interest rate cuts or bailouts. I hope they get wiped out instead.

Rental and lease arrangements make sense when the tenant isn’t committed to long term occupancy. Amusement park real estate isn’t that kind of thing. The property is developed for the purpose. You don’t just pick up and move your amusement park whenever you feel like it. Your profitability is intimately linked with your capital. Land has returns of its own. Selling its land and renting it back just passes those returns on to another party. A few activists might make a quick buck off the transition, but at the expense of long term owners.

A bit of a change in dynamic showing in recent trading, including today. Gold (IAU) and broad commodities (COMT) have been trading contrary … but that pattern has broken.

Gold vs oil: Which offers better protection from rising prices during the Iran war?

This article misses a commonly missed point. The main reason for the difference in gold and oil’s responses to the war is not in magnitude, but time. Gold simply responded earlier. The huge runup in gold was due to inflation. The response of oil was too, but delayed.

Inflation starts in the financial markets, not consumer prices.

The Nasdaq’s top winners are now running hotter than in 2000

This is some scary shit. The AI Bubble is back … with a vengeance. It’s as good a time as ever to make sure you’re diversified with global value, treasuries, cash and commodities.

Readers should well note the response of assets to this morning’s hot CPI release. Up 3.8% year over year. The dollar rose and bonds, stocks and gold all sharply sold off, a deflationary move. Gold in particular moves opposite to supposed “inflation”.

We’ve observed this many times before. Gold has a reputation as an “inflation hedge”, but has a low correlation with the CPI. How to resolve this apparent paradox?

Easy. The CPI does not report inflation. By the time it shows up in the consumer prices, the inflation has already happened. Gold has skyrocketed over the past several years, when the inflation was actually happening. When it’s finally making headlines in the CPI, policymakers come under pressure to respond … belatedly … and inflation hedges cool.

The CPI does not report inflation when it’s happening. Gold does.

‘The revenge of old economy in real time:’ Top Wall Street voice calls a commodity supercycle

“Currie opened the thread with a performance table tied to the October 2020 supercycle call he made while at Goldman. By his numbers, the QCI Commodity Total Return Index is up 217% since then.

The S&P GSCI Total Return is up 205%. Gold – as tracked by the iShares Gold Trust GLD is up 140%. The Nasdaq 100, tracked by the Invesco QQQ Trust QQQ, trails at 130%. The S&P 500 is up 85%.”

Something Historic Is Quietly Lifting Commodities To Records — And It’s Not Hormuz

“The Bloomberg Commodity Index ex-Energy topped 155 levels this week, breaking out above its 2011 high and sitting roughly 13% above its 40-week moving average.

…

It is a record set without crude oil. The move is structural. And it is wired directly into the AI race.”

Emphasis added.

I read his full thread on X on this topic. Very bullish and makes several interesting points. A notable omission, in my view, was him not considering the coordinated SPR release as a factor that has kept a lid on oil prices until now.

With the likely restart of the Iran offensive, and a projected July deadline for stopping SPR releases, the set up for higher oil prices is getting firmer. What levers could be deployed in the future is the big question.

Predictions in Polymarket are still at oil reaching USD 110 per barrell by end of June. It would be interesting to see what numbers are predicted for end of July.

I may have confused things a bit by citing two related stories. But I’m sure both Currie and Turnquist are well aware of the factors that have kept oil prices from rising further than they have.

If you’re referring to Currie, he may not have delved into it just because he’s making a longer term point … he’s taking about 10-12 year commodity cycles. It’s not germane to Turnquist’s point either; which is that in spite of oil and Hormuz getting all the attention, there is something else big going on that hasn’t been so well covered. Media tend to try to link everything to the latest headline drama, regularly overlooking deeper causes.

Buffett Indicator appears to have pushed to 2.3x market value to GDP.

Unprecedented territory.

Unlike the frothy Buffett Indicator Dot.com era, mega-cap earnings today are real.

However:

AI productivity improvement expectations are enormous

AI infrastructure spending is staggering

During the dot.com era, software demands outpaced the need for new hardware, until it didn’t.

My old employer Amazon’s “Get Big Fast” strategy nearly drove it off a cliff

I don’t know when the AI bubble will pop, but there certainly seems to be a “Get Bigger Faster” strategy for AI infrastructure.

Mag7 may have much, much deeper pockets today than the dot.com names of 25+ years ago, but the infrastructure spending is huge.

During dot.com, telecoms raced each other over a cliff to build out the internet, too early.

And Iridium built out satellite bandwidth too early with too high a cost basis.

Will more efficient A.I. LLM model demand sidestep compute(like boring hybrids outrageously outselling sports cars) supply?

AI infrastructure is being build with a combination of strong Mag7 cashflow and balance sheet strength.

But the trajectory is going to rapidly become increasingly hard to sustain.

My position is that the current A.I. bubble has a way to go.

But much like SR71 had a way to go above Mach 3.32 when throttled to the stops.

Much like how CPU has a way to go above 5Ghz when overclocked.

Much like how a forklift rated for 2tons has a way to go above that.

But that’s when things start to break. And break catastrophically.

Surely the Buffett Indicator represents a warning light in the SR71’s cockpit, the computer screen, and the forklift dashboard,

Even with the incredibly slim possibility of explosive U.S. GDP growth(say 7% average for the next 5 years assuming and including high inflation), aren’t U.S. market returns likely to be flat to very weak(and pretty much baked into the cake) going out to 2030?

All valid. I think they’re saying the mismatch is that the bottleneck isn’t in chip or software tech, but in energy and materials. It’s like they’re spending a fortune building the fastest Lamborghini ever, but one that won’t have enough fuel to get very far. A classic Austrian malinvestment story … years of artificially cheap capital lead capital allocators to be less discriminating. That leaves a big gap to be filled as resources shift to the areas that have been relatively neglected.

No specific time frame implied … but the longer the imbalance goes on and the larger it grows, the bigger the ultimate reckoning will be. A number of analysts have concluded that these high valuation levels imply low returns going forward. Here’s a roundup from a couple years ago when the situation was less extreme than it is now:

Long Term Asset Class Outlook

I think the energy part is the greatest danger to everyone. Whether by luck or by insight, it seems the general populace seems to understand that having a datacenter in their city is a bad idea.

You know what the corporations are going to do. They will ask for new power generation facilities to be built and the stupid municipalities will agree to issue bonds to build the power plant for the paper promise of jobs and the corporations buying all that new power capacity.

However, when the bubble bursts, it’ll be the taxpayers that’ll be forced to pay off the bonds for the power capacity that they do not need. The corporations will either go bust or they’ll renege on their promises. I’m sure their lawyers will be very clever to put clauses into any sort of contract to allow them an out.

If any municipality agrees to have a datacenter, they should force the corporation to pay for the power generation in full, up front. Put the money into an escrow account or something but taxpayers should not be forced to participate in the AI bubble.

I hope it doesn’t come to that. With some grounds … there’s a lot of pushback. We’ve cited examples on a number of occasions; here’s one recent entry:

https://financology.net/2025/10/30/has-the-ai-bubble-sprung-a-leak/#comment-8798

Tough contest … ordinary citizens versus trillion dollar corporations … but there are a lot more of the former than the latter. It does underscore a fundamental problem with our financial system though … that it has encouraged concentration of so much wealth and power in so few hands. This is much more than the free market at work.

Data centers use less water than almond farms—and do more good

Nice try, but the overwhelming benefit of data centers is going to a small slice of insiders in Silicon Valley and Wall Street. They’re not spending hundreds of billions on them out of the goodness of their hearts. Average Americans need affordable food and housing much more than they need data centers.

I say this not as a socialist or redistributionist but as a libertarian. The AI bubble isn’t the product of a free market. It’s the product of years of central planners making capital artificially cheap to further enrich the already rich.

I was referring to Currie, reading my response now I realise it appears generic. Your framing makes sense, in terms of the longer term focus of his commentary. Thank you.

BTW as per your point about offsetting oil supply disruptions, here’s a good article expanding on that:

How the US and China’s oil markets are ‘shielding’ the world economy from spiraling prices

It’s just one day, but consistent with the broad commodity thesis that while the oil fund USO is down this morning, the broad commodity fund COMT is up. This despite COMT being nearly half oil.

Well that didn’t last long.

https://www.zerohedge.com/energy/oil-slides-iran-says-us-agreed-lift-oil-sanctions-during-negotiation-period

Hmmmmm

https://www.miningvisuals.com/post/silvers-emerging-role-in-ev-battery-chemistry

Finster,

I’d be interested in hearing your thoughts on Jim Rogers, if you have any.

I followed him thru his Indiana Jones-ish book Investment Biker over 30 years ago.

Actually ran into him in person very briefly 25 years ago on his Adventure Capitalist book global tour, which he followed quickly with Hot Commodities.

He’s been in Singapore for approx 20 years now mostly speaking about a rising China/Asia.

But he has recently been hitting the alarm bells on commodities and gold again.

Historically, he is a loud macro firebrand.

But he has a pretty solid track record.

Is Jim Rogers confirmation of investment themes here, confirmation bias, or ?

Always liked Jim Rogers. Right, wrong or otherwise, he always has something interesting and enlightening to say.

This would have been one of my earliest encounters:

CNBC Your Portfolio 1994 0624

This was must see TV for me as a beginning investor 32 years ago. Some interesting differences and similarities between then and now.

Step back in time to before the dotcom bubble. A bear market in bonds. Gold and commodities didn’t have to shoot the lights out to get mentioned on CNBC. Tech stocks selling at 8-12 times earnings. Come to think of it, P/E ratios getting attention to begin with.