No it didn’t.

December 2023 CPI was released this morning. Financial media reported the rate of inflation accelerated. Predictions of Fed rate cuts were postponed; stocks sold off. This was based on dividing the latest December level by that one year earlier, and comparing that result with the same operation applied to the prior month.

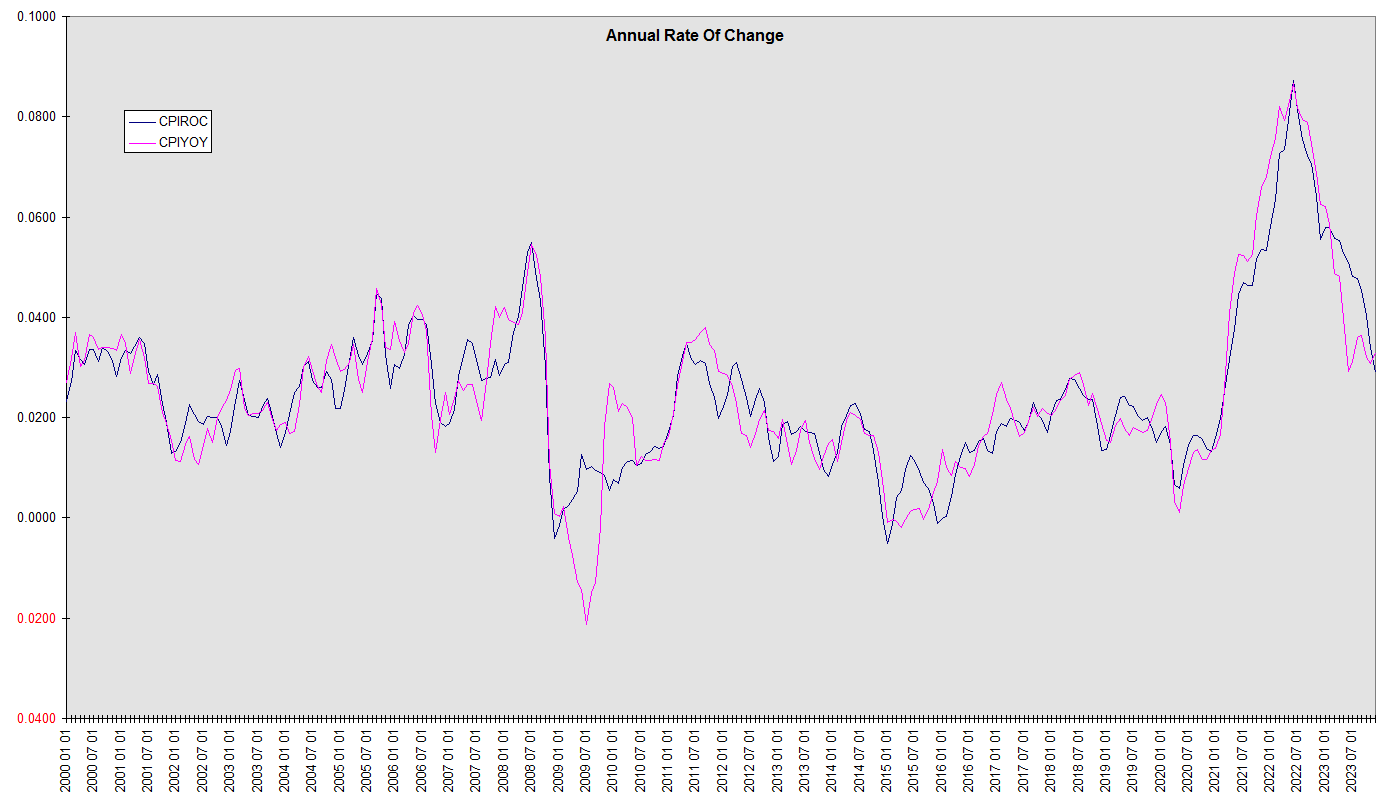

In November the year-over-year CPI change was 3.14%. In December it was 3.35%.

The trouble is there was no actual CPI acceleration … it was a reporting artifact. We criticized this method last month as introducing base effect distortion, and proposed an alternate method which eliminates it. Without this base effect distortion, November’s trailing annual CPI inflation rate was 3.46%. December’s was 2.94%.

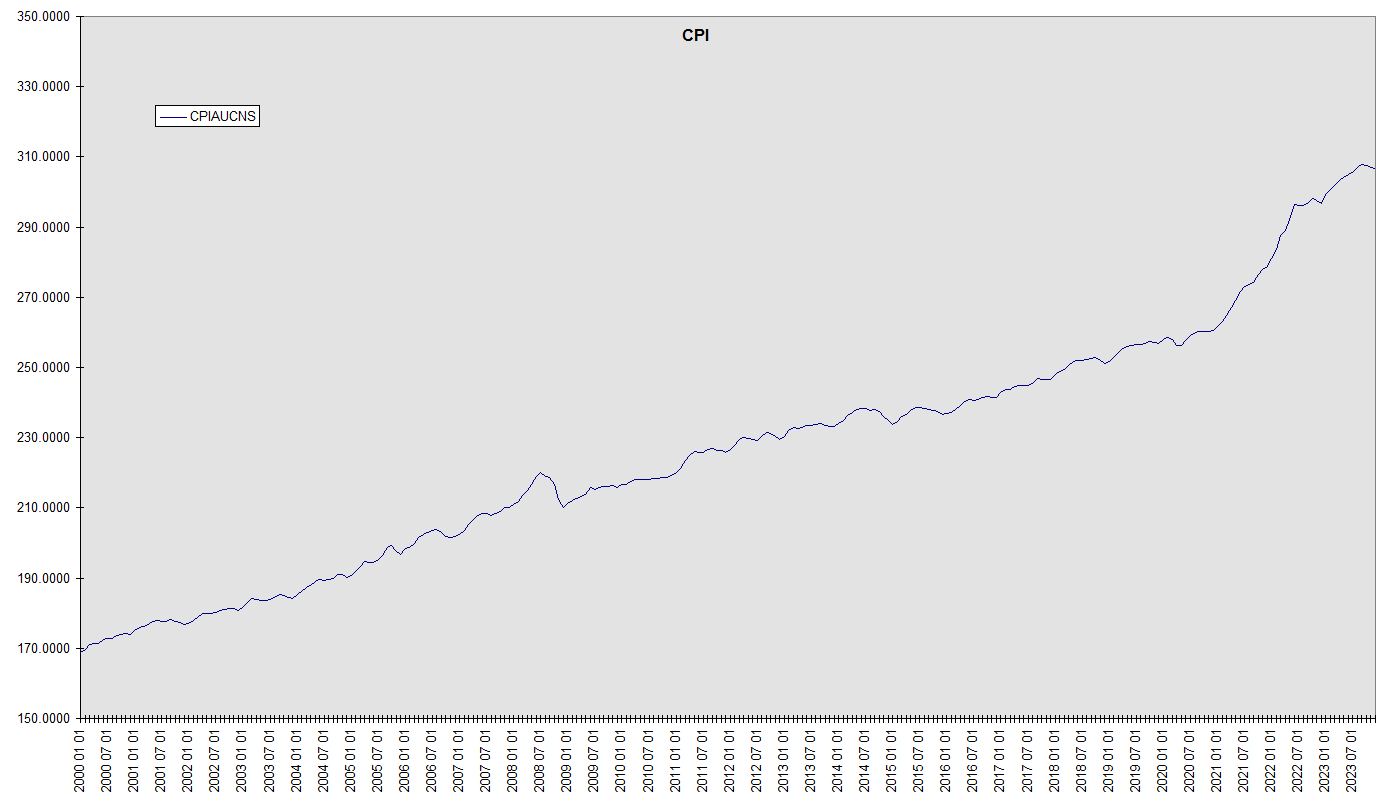

In fact the CPI itself – the actual, raw data – decreased from 307.051 in November to 306.746 in December. It is the third consecutive monthly decrease … the CPI itself actually topped out in September. The CPI from the beginning of 2000 to the end of 2023 is shown here. Even on this 24 year chart you can see the 3 month decline zooming in on the little jog lower on the far right:

Far as the CPI is concerned, that’s three months of outright deflation.

BLS seasonally adjusted monthly CPI still managed modest increases, but the media freakout is nevertheless unwarranted. It’s not that consumer inflation isn’t at risk of reacceleration; but this wasn’t it.

The next chart compares the widely reported simple year over year change (CPIYOY) and the Financology version (CPIROC) sans base effect distortion.

What about the so called “core” rate of inflation? This purports to isolate the “underlying trend” by eliminating the “volatile food and energy” components. In the real sciences, filters such as moving averages do that job with objectivity and precision. Only in economics could you pretend to look deeper into the data by discarding some of it. Financology doesn’t participate.

Of course, markets pay attention nonetheless, if only because the Fed does. But mainstream media do a fine job of reporting conventional economics, so we don’t bother. Our job is to find the story it neglects. Because perceptions rule the short term, markets sold off sharply this morning on the imaginary increase in consumer inflation. But in the fullness of time, reality prevails. As the saying goes, in the short run markets are a voting machine; in the long run they’re a weighing machine. Some weighing may already be in progress as markets claw back some of the initially ceded ground.

But so far this is just history, specifically of the CPI. What comes next?

As detailed in the above-linked previous post, consumer prices lag inflation. The CPI wasn’t even designed to report “inflation” to begin with. It’s just as the name says: “Consumer Price Index”. Only through slippery economic lexicography was it gradually transmogrified into a measure of inflation per se.

The more commonly raised question of whether the CPI even accurately reports consumer price inflation is a separate issue layered on top.

So do we take this three month decline as evidence the rate of inflation is negative or even falling? No. We look to real time asset markets for timely information. When the dollar loses purchasing power in the asset markets … against stocks, bonds, foreign currencies, commodities … that’s the first proof of inflation. Its loss of purchasing power in the consumer markets comes later. Consumer price inflation – measured via the CPI, PCE, or otherwise – represents not inflation but its second order price effects.

The conventional view is popular for two main reasons. First, inflation is fun … as long as it’s confined to asset prices. It’s taken as a sign of prosperity or growth. It’s something people want to believe. Only when it inevitably begins to spill over into consumer prices do they impose a negative value judgment. Second, the lags between its appearance in real time capital markets and consumer markets are multiple and variable. The only certainty is that it will. Either asset price inflation is reversed or it will appear in consumer price inflation. They’re both the same thing – dollar depreciation – with the price effects simply taking time to work their way through to final consumer prices.

Popular as it may be, however, the conventional view makes for extraordinarily bad science. Wreaking practical damage by leaving policymakers chasing exhaust fumes, chronically behind the curve, inflicting boom and bust volatility.

So after the inflation of 2020-2021, we saw the CPI record it in 2022. The deflation of 2022 was reflected in the CPI disinflation of 2023, most recently in the CPI deflation of the last quarter.

The inflation of 2023 has yet to show up in consumer price inflation…

“Because perceptions rule the short term, markets sold off sharply this morning on the imaginary increase in consumer inflation…”

I wasn’t necessarily expecting immediate validation, but this morning’s PPI release was “softer than expected”, leading media to “unpostpone” the Fed rate cut predictions that were postponed only yesterday.

The folly of jumping on the reaction bandwagon to each government data release is hard to overstate.

I find it incredible that the narrative seems to be that if inflation is near the Federal Reserve’s preferred 2% that rate cuts are warranted. This seems to ignore all of the 1990s when we had the “Great” Moderation. Going back many more decades and centuries, the economy seemed to function just fine with interest rates at around 5% even when inflation was very low.

The obsession with an agency of central planning should strike one as odd in this purportedly free economy. Worse, considering free market capitalism is being blamed for so many ills. (Don’t knock it till you’ve tried it!) You raise some fitting context … America somehow managed to grow from a ragtag bunch of colonies to world economic powerhouse without a central bank at all.

Now it’s the font of all growth?

Please.

The descent hasn’t been a straight line. The nineties for instance were practically a golden age compared to both two decades prior and the decades since. A president declared the era of big government was over. Deficits shrank to the point economists were debating what the financial system might look like without a government bond market. Prosperity was more widely shared, all without multi-trillion-dollar corporations or social media. And yes, somehow all that managed to happen with interest rates over 5%.

Red Closed, WAR,War & more WAR

https://www.youtube.com/watch?v=3rQyzuVgRB4

Inflation baby

You betcha. War is a double whammy. You expend resources to destroy resources.

If governments had to send a tax bill to voters to cover the costs of war, there would be very few wars. Even if they had to borrow and repay, there would be fewer wars, because the tax bill would still have to be paid. So it comes down to borrow and print. That is, inflate … central banks are the great enablers.