I don’t spend a whole lot of time with historical facts and figures on this site. Facts are boring. Opinions are more fun … much more there to debate. Not to mention that you can never get historical returns … what you do today can only affect future returns. And historical facts don’t tell you much about those future returns. At least not without a lot of interpretation, which just takes you full circle right back into the world of opinion.

One thing I do spend a lot of time thinking and writing about is how bad the mainstream financial media is. At least when it comes to helping its readers and viewers invest better. From their point of view, it’s best regarded as useless infotainment … and if taken seriously, even counterproductive to their investment performance. The badness of the mainstream financial media is why this site exists.

One example is its perennial obsession with what the Fed will do next and when. Unless you are a professional bond trader, such speculation is useless to you. If not worse. After nearly thirty years, I only comment on Fed policy for amusement, and even then don’t spill tanks of digital ink on when the next 25 bp move might come. We ordinary investors are much better off watching the Treasury yield curve. It’s not speculation, it’s hard fact, and it moves before the Fed does anyway.

Another is the financial media’s obvious bias. It’s a promotion platform to sell financial products, meant to be lucrative for their sponsors, not for you.

Here’s where opinion meets fact. Given the amount of coverage given to say, stocks versus gold, which would you expect to have been better to own so far this millennium? Everybody knows stocks have been the better investment in the long run. The trouble is that the applicable “run” is too “long” to be of much use to you. Longer than most investors’ investing careers. If you invested solely in an underperforming asset class for two decades, that’s a bit long of a run to accept. Extrapolating past returns to future performance is bad enough, but using a century or more of raw return data to draw conclusions about what you should be doing now is worse.

So which outperformed? Gold. That’s historical fact. But don’t expect to hear it on financial media lite. They are there to sell stocks. And in more recent years, other things their sponsors can make money selling, like cryptos.

So let’s look at the historical fact. Suppose WTBFOTS (when the ball fell on Times Square) at the beginning of the year 2000, you had put $10,000 into the S&P 500, diligently reinvesting dividends ever since, while a friend put $10,000 in gold and just stuffed it into a box, only to be forgotten about for 24 years. Who would be ahead today?

I’ve already given away the answer, but let’s take a look at the actual numbers. It turns out that the underperformance of stocks is not trivial. It’s not even close.

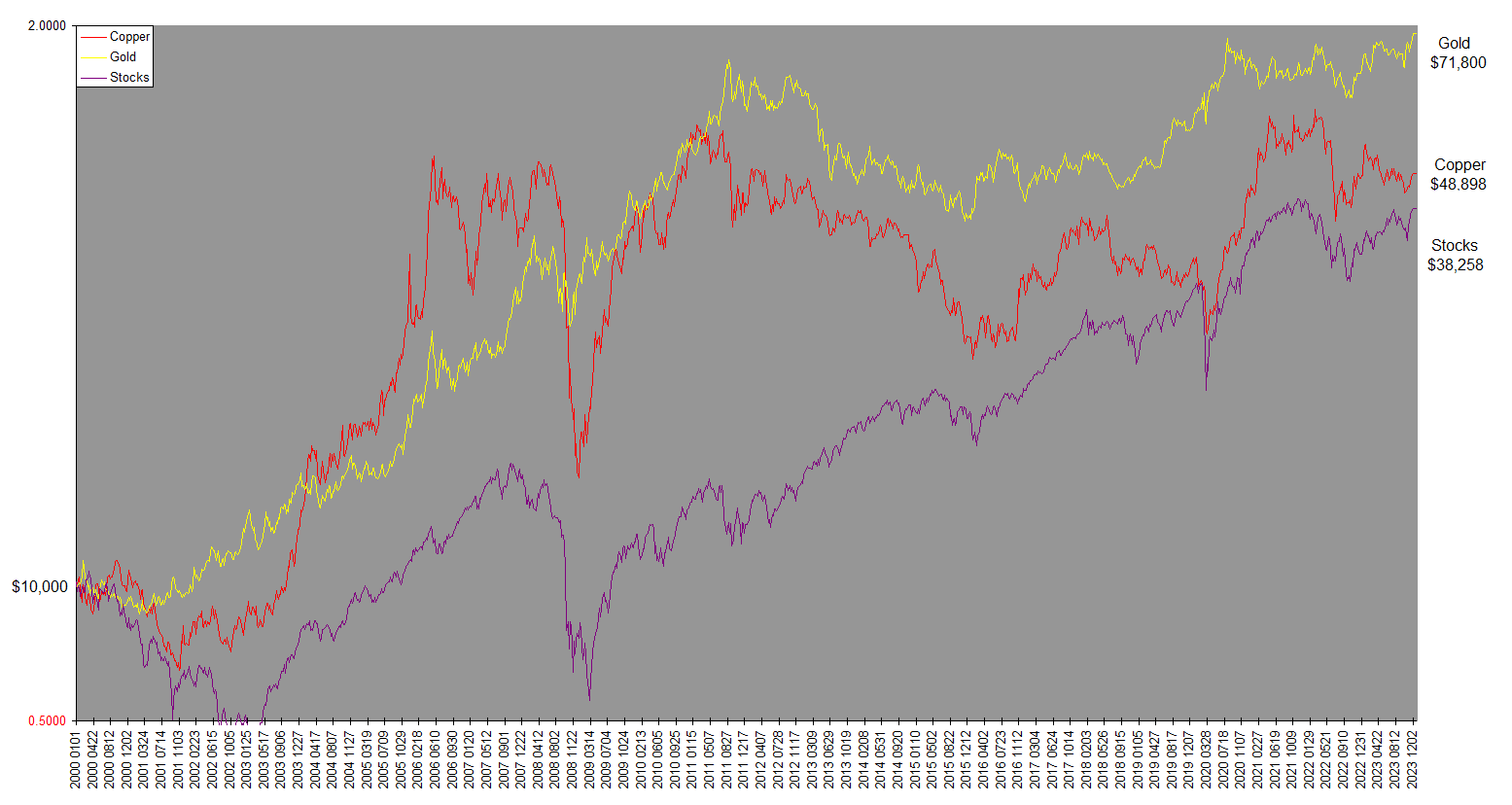

Your investment would be worth $48,898. Your friend’s would be worth $71,800.

It’s not even clear that you actually gained anything. That $48.898 figure only tells you how much you outperformed cash under the mattress, cash which has lost value to inflation. Measured in money which has not lost value to inflation, you are down 32%. That’s $3200 of your initial investment in the world’s most ballyhooed set of stocks down the porcelain receptacle.

Over a span of nearly 24 years. Much too big a part of your investing lifetime to dismiss as “short term”.

Let’s look at a few charts. The first one is of copper, gold, and stocks. It plots how much $10,000 worth of each bought WTBFOTS 2000 would be worth as of last Friday. These are total returns, stock dividends included.

The objects of media obsession, stocks, came in last place. Gold in first place. And just in case there is any temptation to ascribe magical properties to gold, even copper beat stocks. You could have dumped a bunch of copper wire or pipe in your basement and come out ahead of stocks. Imagine that, mere chunks of inert metal beat stock in the world’s great corporations over a multi-decade time frame.

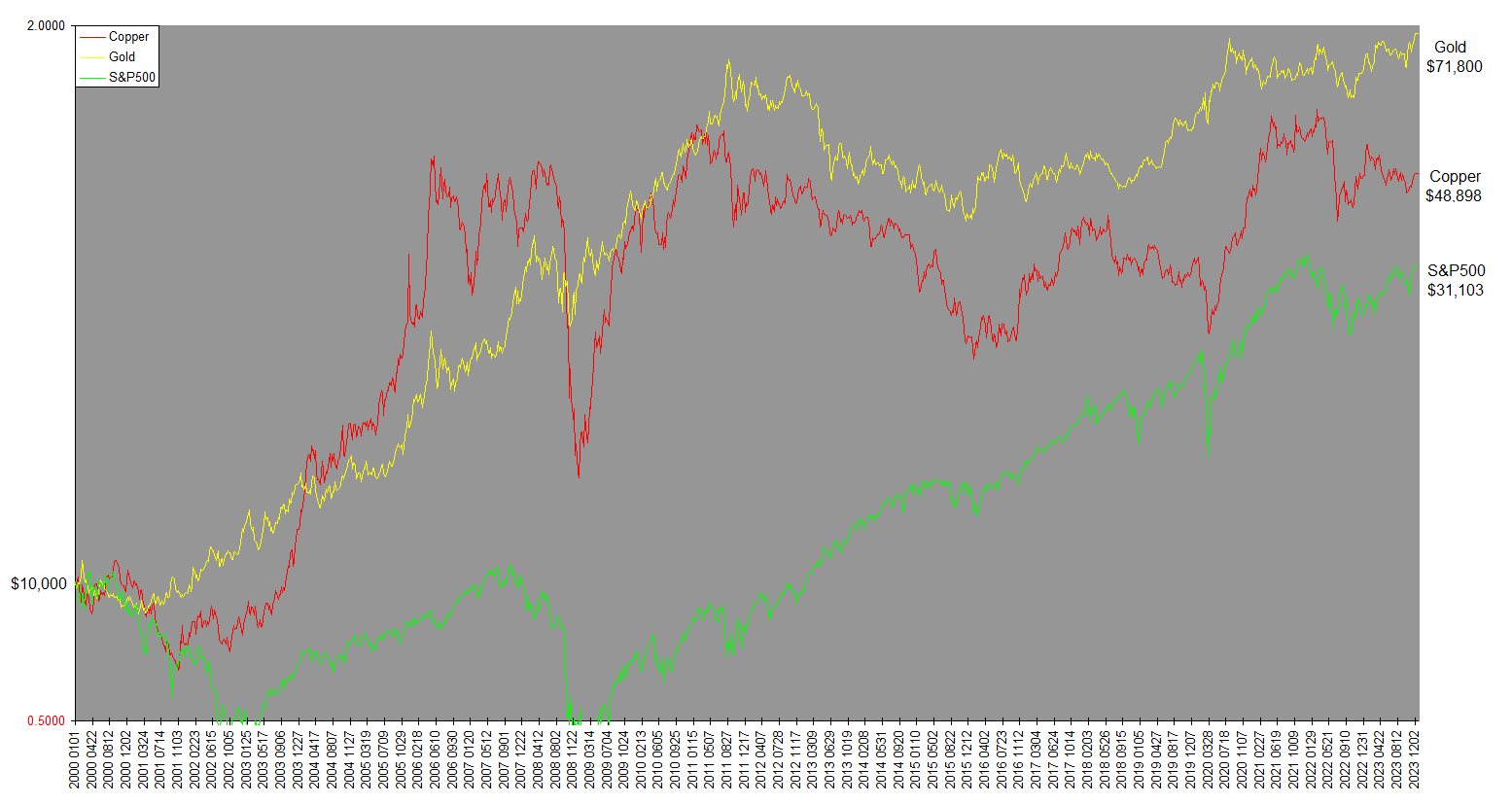

Next up we do the same with price performance of the S&P 500. This solidly puts asunder another financial media obsession: Capital appreciation. As far as they’re concerned the way you made the big bucks on stocks is from their “going up”. Dividends are an afterthought, worth a mere asterisk. You are treated daily to price moves of all the major stock indexes and popular stocks … dividend returns are about as common as unicorns in comparison.

The fact is that those capital gains left you under water. You would have enjoyed more “capital appreciation” from mere chunks of inert metal.

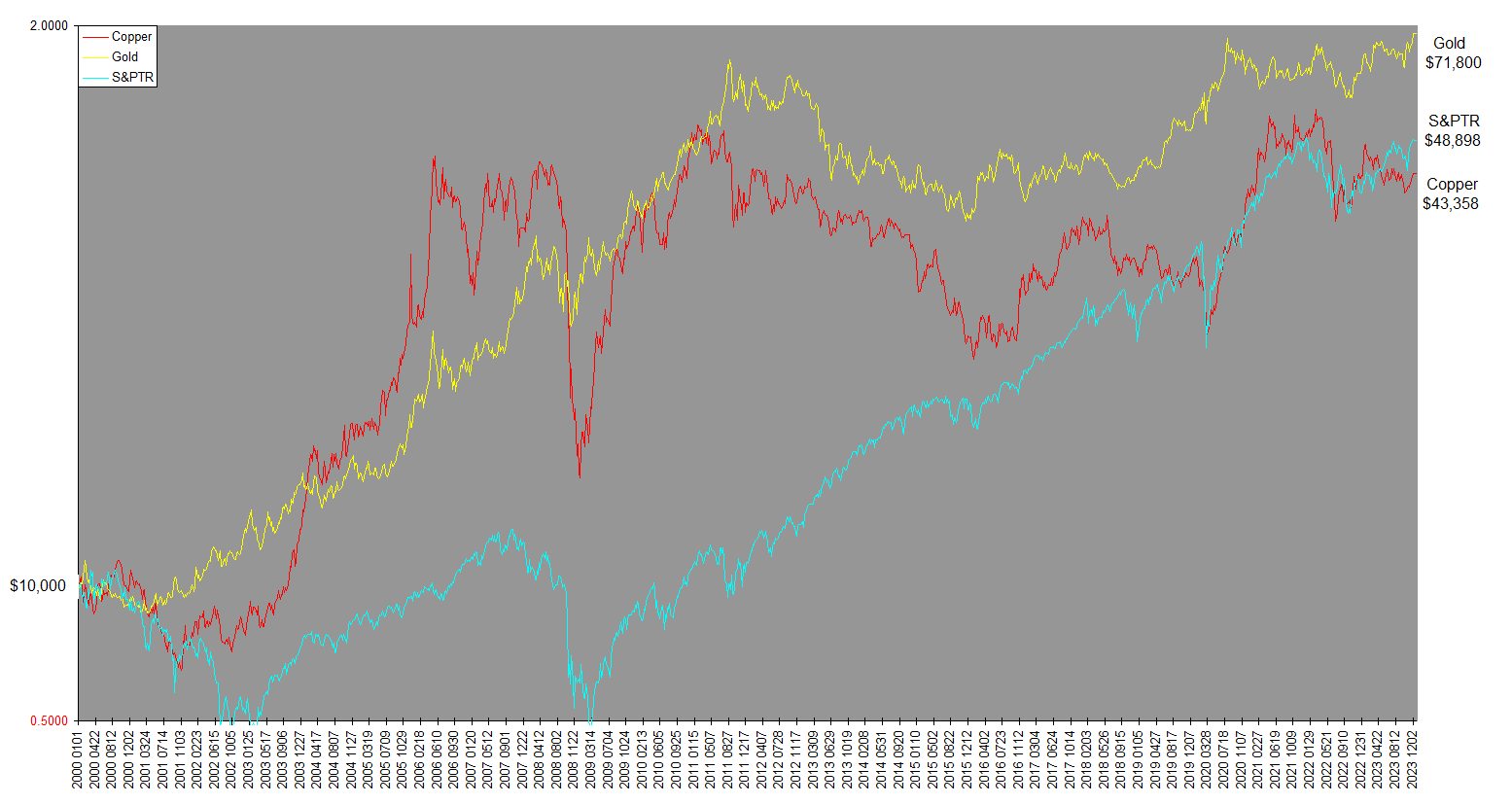

The third and final chart drives home the value of dividends. The S&P total return, including dividends, managed to at least squeak past copper … over the span of a generation.

(World stock data from Dow Jones and FTSE Russell. Gold and copper from Kitco and Norman’s. S&P data from Yahoo Finance.)

So if past returns alone are next to useless or worse as a guide to how to invest for the future, how in the world do you invest? For starters, you diversify. Financial assets alone are not a diversified portfolio. You must consider real physical things, like copper and gold. Add silver, platinum, oil, art, real estate or even fine wines if you fancy. Stocks and bonds alone are like two legs of a three legged stool … unstable and undependable.

Another crucial consideration is that the returns you receive do not merely depend on what you buy, but at what price you buy it. Why did you do so poorly – over 24 years – just buying stocks at the beginning of the millennium?

You overpaid. As Chuck Carnevale says, valuations matter, and they matter a lot. Stocks entered the century at very high valuations. You can’t expect to earn historical average returns by buying at valuations far above historical averages. Those historical average returns are reported for stocks bought at historical average valuations. And this is relevant right now, because valuations of US stocks, the S&P 500 and Nasdaq indexes especially, dominated by a few very big high flyers, are once again at very high valuations. If they were at normal levels, your losses since 2000 would have been much worse.

The takeaway is simple. Don’t just own stocks. Own bonds and physical commodities like copper and gold. Own less stocks when valuations are high, more when they’re low. And for your financial health, seek out alternatives to tout media. In the true long term, one of the most profitable investment habits you can have is to stay the heck away from anything it is excited about.

CB’s are all buying now……………

They’re losing confidence in their usual main reserve asset. It’s a bit ironic that this is happening as its issuer has been in a very high profile campaign to buck it up. Imagine what it will be like next time they feel like trashing it. Questionable as their motives often are, central bankers aren’t stupid. They see the same things we do … reckless fiscal policy, weaponization of the dollar … and come to much the same conclusions we do.

Got gold?

Ukraine looks like a lost cause, Putin is in the middle east & is being treated like a Rock star!

Putin also bought his central banker with him……why?

mike

The same reason I take my central banker with me wherever I go?;-)…

Ukraine looked like a “lost cause” almost from the beginning. Correct me if I’m wrong, but before Putin invaded Ukraine, didn’t NATO first try to subsume it, expanding its territory right to Russia’s border? Then after Putin invaded, did the Biden administration look for ways to de-escalate? Or practically every day find new ways to escalate?

The sanctions were an exercise in shooting one’s self in the foot. Taking Russian oil off western markets. Weaponizing the dollar, thereby lighting a fire under efforts to reduce its use as a reserve asset and trade currency. Seizing assets, demonstrating disregard for property rights by the Land of the Free. Then blaming the resulting economic train wreck on virus induced supply chain disruptions.

Meanwhile US debt is soaring out of control, to the point the central bank is likely to fall under pressure to monetize. This after the last round of monetization already saddled millions of working Americans with a crushing inflation tax. The cost of trying to be the world’s policeman is something the US can no longer afford.

https://nitter.net/jfarchy/status/1733146193532781030#m

DR Copper?

We could quibble about Dr Copper’s reputation as an indicator of economic growth, but it appears to be a better indicator of dollar depreciation (inflation) than the CPI…

“Better to leave it in the ground”

He lies………………then he tells EVERYONE how much more the Gas is now costing!

https://nitter.net/DagnyTaggart963/status/1733456599262298379#m

We may never know for sure who sabotaged the Nord Stream, but it’s not at all clear what motive Russia might have had. Meanwhile its foes have shown no hesitation to shoot themselves in the foot just to give Russia a splinter.

https://www.youtube.com/watch?v=OYfnkLurLA8

City of London