SS 2023

SS 2023.00

Commentary

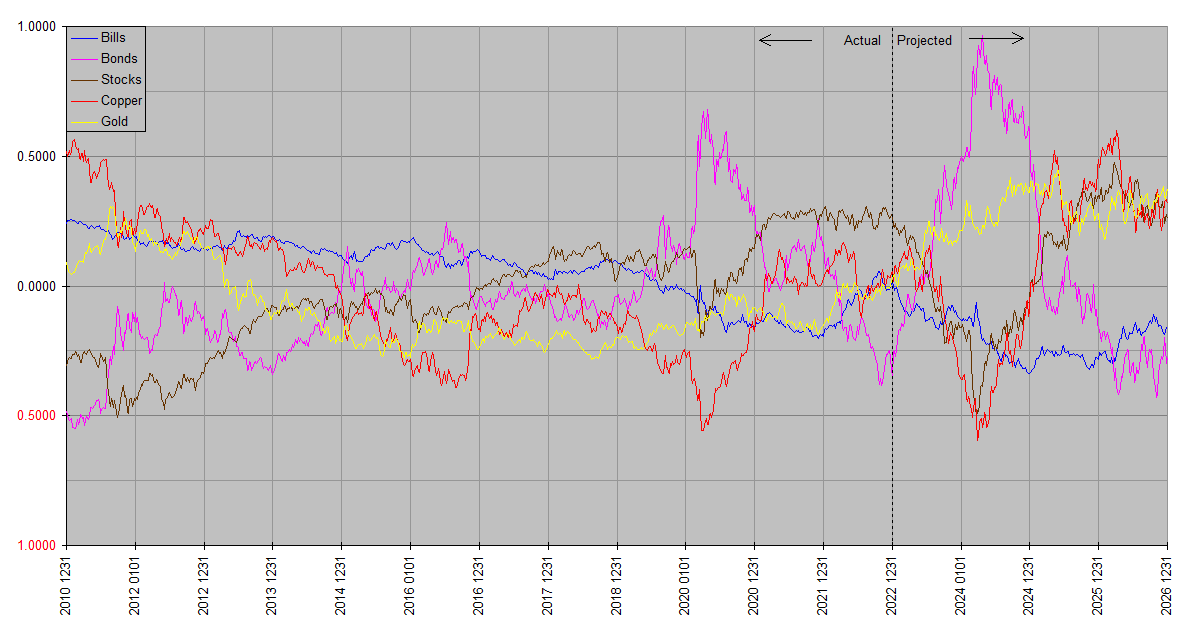

Let’s take a look over the past year first. (See the Market Analysis page for sequential comparisons.) The first three quarters of 2022 were notably bullish for cash, in particular the US dollar. Synthetic Systems however only hinted at that at the beginning of the year … it consistently underestimated the strength of the USD relative to other assets. My call for cash outperformance on January 18 and at several subsequent points was based at least as much on subjective impressions of the state of financial markets, consumer price inflation, and the outlook for Fed policy response. This call was in effect until I withdrew it on November 11, having concluded on October 27 that the bottom for bonds was likely in.

The value added by SS was minimal in the second half of the year. It bailed on stocks at the beginning of the third quarter as they continued to rally into December. This is not unusual; its resolution dissipates below about one quarter of a year. It did however help us identify the bottom in bonds … SS pegged it for October 1, and it came October 24. The likelihood that a low was due in that time frame helped us recognize it much sooner after it occurred than otherwise be the case.

Rather the major contribution of SS came in the first half of the year. Financology went deeply underweight bonds at the beginning of the year and remained so until returning to neutral around mid year, finally going overweight at the beginning of the fourth quarter.

The overarching theme for the SS 2023 forecast is for Bonds and Gold to outperform and Stocks to underperform. Bills have a moderately bearish outlook but given the failure of SS to clearly call the bull market of 2022 it’s not a high confidence call. Copper has a moderately bearish outlook as well but has been unstable between successive forecasts and so I likewise hesitate to draw any firm conclusions there.

About Synthetic Systems

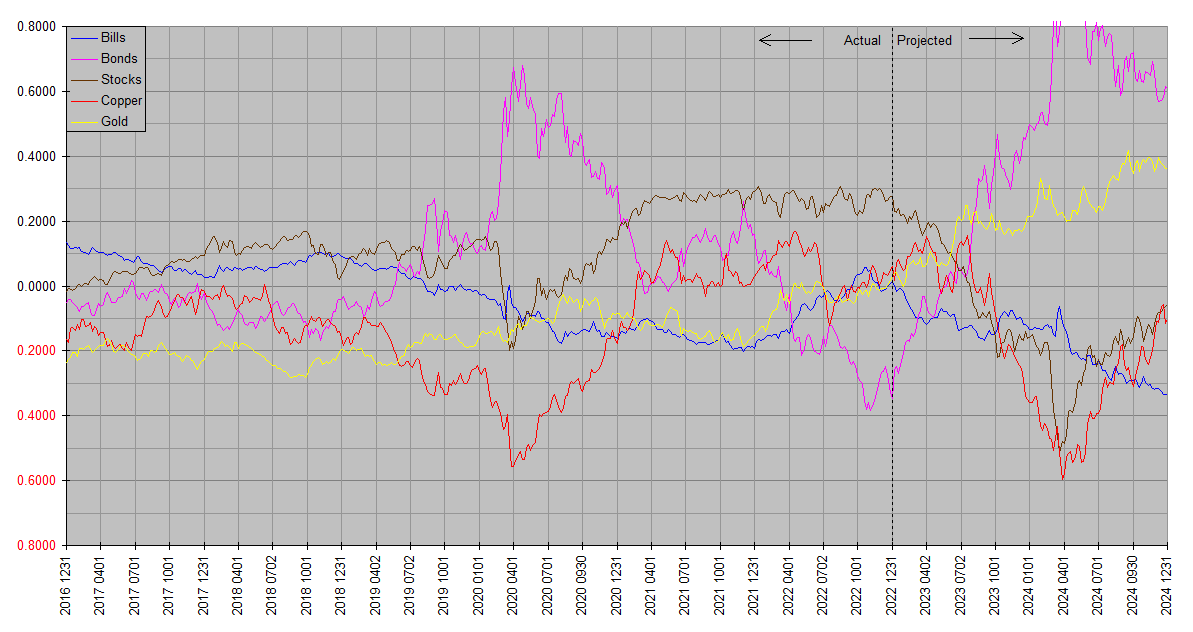

Synthetic Systems is a computer forecasting model covering five asset classes: Treasury bills, Treasury bonds, stocks, copper & gold. The plots are all on the same basis so as to be directly comparable – total return. So the slope of one asset rising more than another indicates outperformance, and vice versa. Plots are in natural log space so that the same vertical increment means the same proportional (percentage) increase regardless of vertical position. The total returns are not denominated in dollars or any other currency, but are relative to each other.

Bills refers to US Treasury securities of effectively zero maturity and duration, similar to a Treasury money market or ultrashort bond fund. Bonds refers to US Treasury securities of effectively infinite maturity (duration reciprocal of yield), but approximates the returns of real world extended duration Treasury funds like EDV, and to lesser extent VGLT and TLT. A broad UST fund like GOVT is around midway between Bills and Bonds. Stocks refers to the entire asset class (not just US or any one country). Copper and Gold represent the respective elementary commodities, except to note that copper is broadly indicative of physical commodities as a class and suggestive of trends in goods and services price inflation.

Because the Bonds plot represents infinite maturity bonds, it is greatly exaggerated in relation to most real-world bond investments. The Vanguard extended duration Treasury fund EDV tracks it closely. Other popular long term treasury funds such as TLT and VGLT can be interpolated as a roughly 90:10 mix of Bonds and Bills. The broad iShares treasury fund GOVT is roughly a 40:60 mix.

The choice of modeling infinite maturity bonds may seem odd, but was motivated by a desire to put long bonds on an equal footing with stocks, which are infinite maturity securities. It does however ask the viewer to interpolate between the Bills and Bonds plots to visualize the performance of real world treasury investments. But this is true of many real world assets … junk bonds for instance can be read as intermediate bonds and stocks, and silver as intermediate copper and gold. SS asset choices are intended to represent the ‘corners’ of a region in which most real world assets reside.

Another unrelated factor could exaggerate the bond performance forecast. SS frequency response focuses on time frames from about one quarter year to four years. This means that it does not attempt to take into account very short or very long term trends. On the second count, if the secular trend of bond prices has turned lower, it won’t much be reflected in the forecast. A multi-decade trend would be overwhelmed by the cyclical trends SS focuses on, so it wouldn’t invalidate the bullish bond forecast over just a couple years, but it would reasonably be expected to moderate it.

At the other end of the spectrum, if forecast accuracy fades as the time frame grows shorter, why don’t I just filter that information out of the plots? The answer is that it’s still better than random. Even odds of 51%-49% on a forecast have utility, even if less so than trends in SS’s sweet spot. The practical impact is that readers of SS charts need to be aware of the time frame factor. It’s more work for the reader, but the cost of throwing out information of even modest marginal utility is difficult to justify.

The charts are best considered together. Annual and quarterly charts are respectively grouped together on dedicated pages under Market Analysis to facilitate this. The forecasting accuracy of Synthetic Systems is best evaluated by comparing successive charts, as the “Projected” time frame of an earlier chart slides to the left into the “Actual” time frame of later charts. Moreover, similarities between the latest update and earlier updates indicate areas of greater confidence in contrast to differences which indicate greater uncertainty.

Readers should bear in mind that Synthetic Systems forecasts comprehensively reflect financial and economic forces (e.g inflation, interest rates, monetary policy, money flows, seasonality, natural resources, technology, demographics, the business cycle, global economic trends, consumer sentiment, investor psychology, momentum, mean reversion, etcetera), but do not reflect external noneconomic factors (e.g. natural disasters, pandemics, unexpected geopolitical disruptions) until they are incorporated into the financial and economic sphere. It’s most applicable over time frames from one quarter year to four years … its accuracy is limited by noise and news flow on the shorter time frames and it also does not attempt to model drivers of longer term returns such as valuations.

Readers are encouraged to consider Synthetic Systems forecasts in conjunction with fundamentals and valuations. Synthetic Systems however often forecasts trends long before the fundamentals fall into place; for this reason it’s useful as a medium term planning guide, with the appearance of fundamentals consistent with a Synthetic Systems forecast serving as confirmation, the lack thereof nonconfirmation. Final confirmation occurs when the trend is actually in evidence.

Thanks for this.

To clarify, if we were to assume that the next decade is one of moderately higher CPI inflation coming out of the predicted recession (say 3.5% per year vs 2.5ish% over the previous decade) then SS is overstating the rally in bonds?

What would be favoured in this scenario?

I guess growth stocks will underperform vs value in a higher inflation scenario?

There would be little to no effect based on consumer price inflation, because SS plots asset returns relative to each other, as opposed to dollar terms. It only considers assets. Generally the Copper plot most closely tracks consumer prices, and that connection is tenuous. The above post goes into more depth on what SS takes into account.

But I nevertheless think SS is overstating expected bond returns. This is because it doesn’t reflect very long term trends, and I suspect the multi-decade bull market in bonds has reversed and that the very long term trend is now bearish. So to most accurately interpret SS forecasts, imagine them superimposed on the very long term trends. The latter are best understood on the basis of fundamentals and valuations. SS is designed to reflect the middle ground between short term trends driven by technicals, positioning, and news flow on one hand, and long term trends driven by fundamentals and valuations on the other. The very short and very long term trends are presumed provided by other means better adapted for the purpose.

Generally speaking these medium term trends dominate in the cyclical arena where SS works, but in a long term bullish trend, the rallies would be somewhat bigger and the declines somewhat smaller. In a long term bearish trend, it would be the opposite … rallies would be somewhat smaller and declines somewhat larger. Notice for instance that SS correctly forecast the recent bear market in bonds, but somewhat underestimated its depth.

Also bear in mind that the Bonds plot is of infinite maturity bonds … the longest of the long … so as my post outlines, most real world bond investments lie somewhere between the Bills plot and the Bonds plot … shorter maturities closer the the former and longer maturities closer to the latter. Bills and Bonds bookend the extremes of Treasury maturities.

Growth versus value depends on exactly how you define each … there are no bright lines, but you can rank stocks into longer and shorter duration. The former are traded more on expected earnings in the out years versus the latter which are traded more for more visible earnings. Their relative valuation changes with like changes in the yield curve, which also reflect how the markets are valuing nearer versus farther term future dollars.

But there’s another dimension as well … emphasizing far-in-the-future earnings also involves more speculation. When money is easy investors can more readily get caught up in fanciful stories about glittering futures and forget about hard numbers altogether. So part of what we’ve seen in the retreat of growth stock valuations is not only a change in how future money is valued today, but also in a more sober assessment of future prospects as momentum reverses and emotional tides ebb.

high inflation => high rates => low long duration assets like growth stocks.

inflation is probably undervalued right now – fwiw i have some money in a 6 year tips ladder as a conservative way to harvest this [if correct]. i use individual tip bonds, not funds.

commodities and equities should do well longer term, but not until after the significant recession that many are predicting and that is consistent with this year’s coming performance indicated in ss2023.

Thanks Bill and JK. I was aware that SS plots assets in relationship to each other.

I mentioned CPI as that is the metric that Government’s and Central Banks look at to determine interest rates even though it is the last place inflation shows up.

The explanation of SS as more of a cyclical tool is very clear as is why so called growth stocks will perform poorly when the cost of borrowing money is higher.

Oh, okay … for sure the CPI is a widely followed measure. Yet it’s practically useless for forecasting purposes. As you correctly observe, it lags actual inflation. Moreover the lags are multiple and variable, being distributed over time frames from weeks to years. The policy response is even more variable and lagging. Exhibit A is the Fed’s dismissal of consumer inflation as “transitory” for so long before finally mounting even a weak policy response.

We could also quibble that the Fed says its preferred gauge is the PCE deflator, but PCE suffers from the same weaknesses.

As far as monetary policy goes, the bond market itself is by far the most reliable metric. The bond market led the Fed out of the starting gate. You could attribute that in part to Fedspeak, but that still leaves the question of how to interpret Fedspeak. The Treasury yield curve hits two birds with one stone – it’s the best objective, quantifiable interpreter there is, and bypasses speculation as to what degree the Fed is leading markets versus following them.

It also turns out that of the asset classes SS is historically most accurate in forecasting the bond market. I can only speculate as to why, but would venture that the bond market is the Mister Spock of markets … the most logical and least emotional. As a Spock like entity itself, it would stand to reason that SS would understand the bond market better than the others.