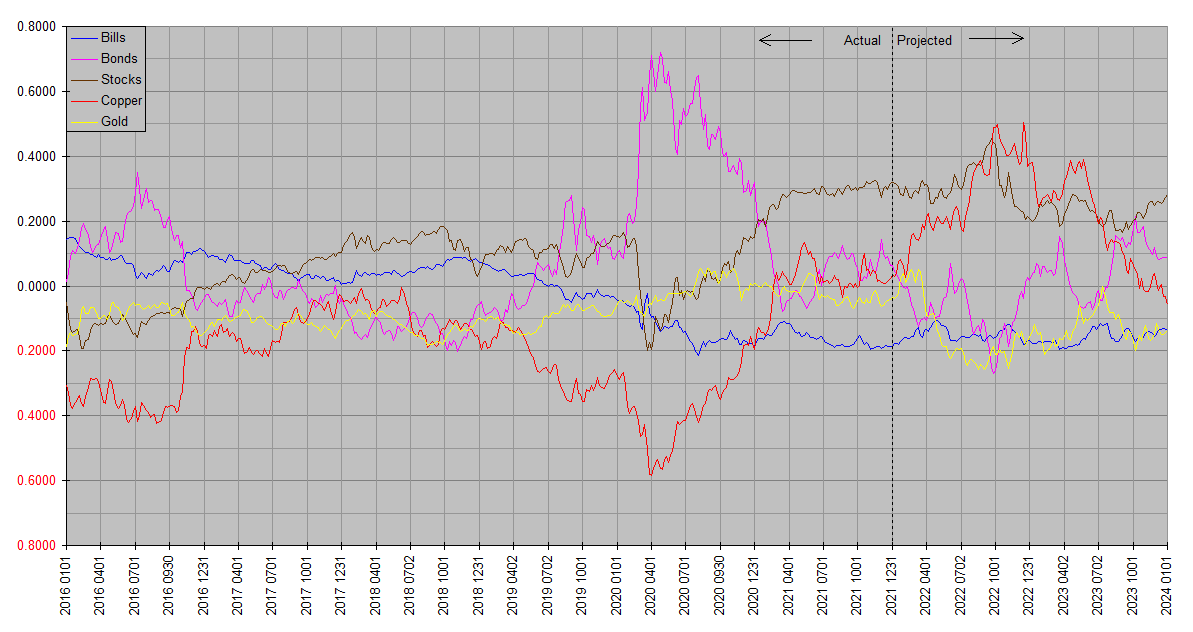

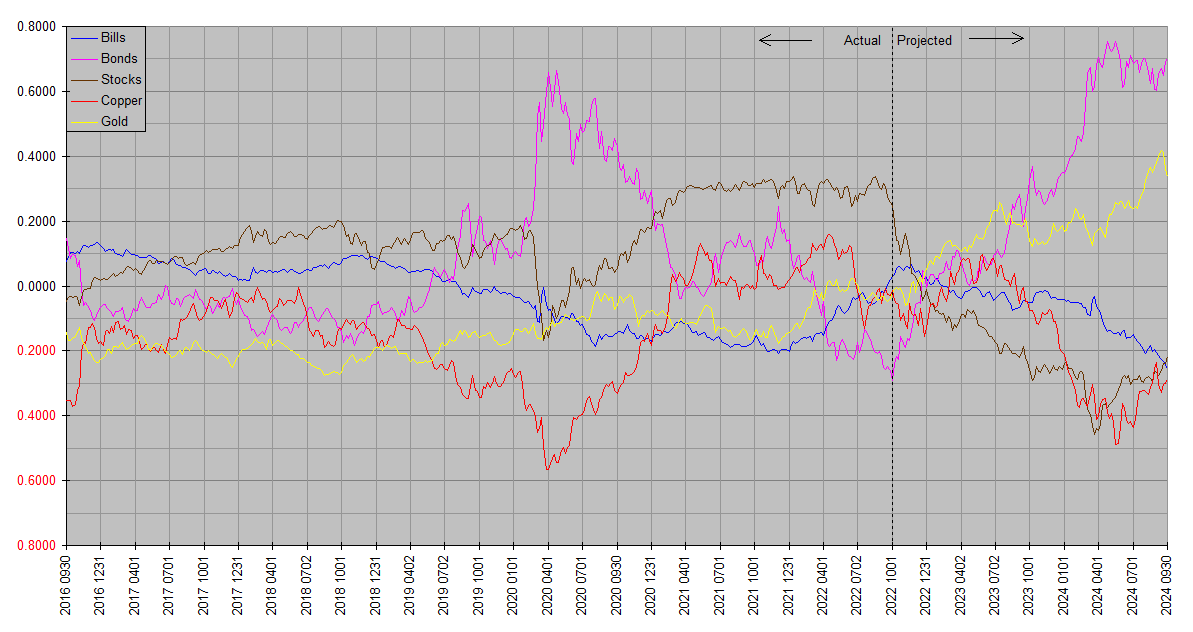

Financology has been following the long term bond space for the current time frame for a couple of years. Until recently this has been based almost exclusively on Synthetic Systems forecasts. At the beginning of 2021 for example, SS saw a deep bear market in TBonds continuing until around October 1, 2022, then reversing into a bull market:

At the beginning of this year, it reiterated the call:

It was again reasserted at the beginning of this quarter:

SS provides no fundamental argument for its market calls. This can be a negative, because it doesn’t gives us any basis to inquire whether they seem sensible. On the other hand it can be a positive, because if we have a sensible fundamental argument, we know that it is independent of SS, and therefore in order for the market call to be wrong, not just one but two, independent analyses have to both be wrong.

We’ve cited some fundamental arguments more recently in Comments, for example this September 14 analysis from Michael Lebowitz at RIA:

Yields are Defying Yesterday’s Logic

On December 2 two articles appeared on Advisor Perspectives supporting this view:

In Defense of Defensive Fixed Income: The Case for Adding Duration

2023’s Best Asset Class: Long-Term Treasuries?

The day before yesterday Financology reiterated its overweight bonds underweight stocks stance. The next day it received a stamp of approval in an excellent analysis by Chris Yates December 7:

Besides the SS medium term outlook and the fundamental case, we also watched the shorter term technicals for indications of a bottom. We found it on October 27, as noted in this comment:

The bottom SS had long anticipated for around the beginning of this quarter occurred on October 24. Since then long term Treasuries have bounced smartly. As of yesterday’s close, TLT is up 18.5%, the broader VGLT 16.7%, and the super long EDV (the closest proxy for SS TBonds) is up 27.9%. Even the comprehensive meat-and-potatoes 1-30 year Treasury fund GOVT is up 5%. All these are exclusive of dividends, which are now meaningful due to higher yields.

Even with substantial gains now in the rear view mirror, in light of the SS outlook and the more fundamental based analysis linked above, it’s likely more remain ahead.

Your article helped me a lot, thanks for the information. I also like your blog theme, can you tell me how you did it?

Thanks … the theme is a stock WordPress theme called Argent.