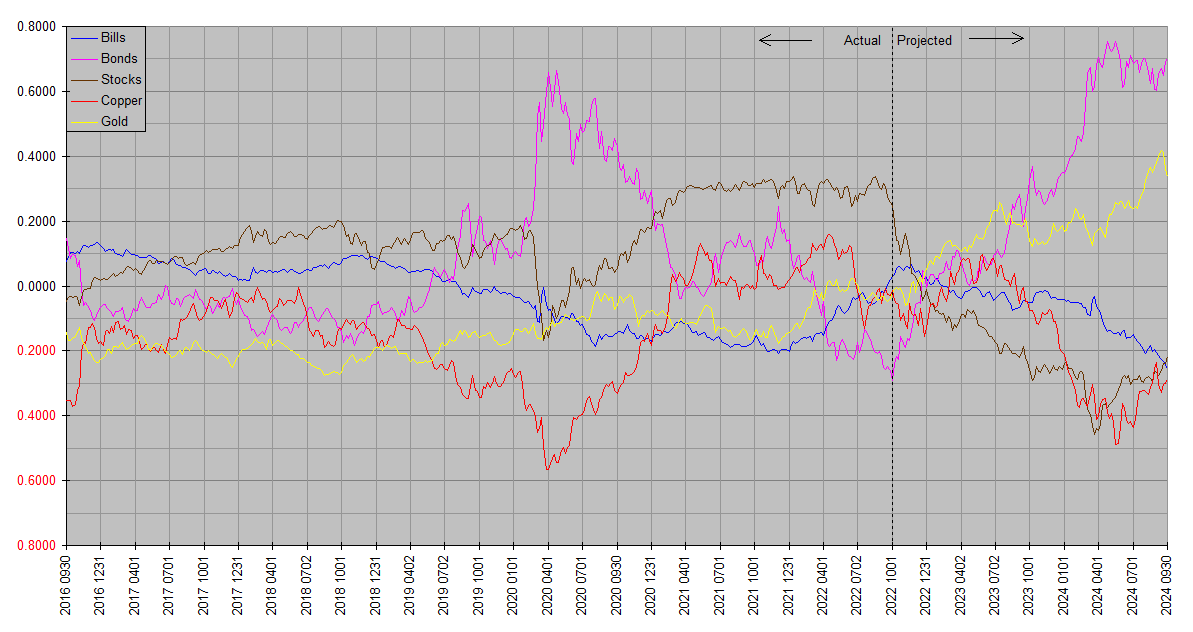

Let’s recap our recent market play-by-play. Synthetic Systems called a bottom in bonds around October 1. It had been pretty consistent on 2022 Q4 for a couple of years. For example at the beginning of 2021, it forecast a major bear market in bonds lasting until around the beginning of this quarter:

It reiterated that call most recently at the beginning of 2022 Q4 in Synthetic Systems 2022.75:

(For a full review of SS archives, go to the site menu and click Market Analysis.)

As we’ve discussed in our quarterly SS updates, the SS forecasting target is medium term; roughly from one quarter year to four years, bridging the gap between short term technical analysis and longer term fundamentals and valuations. So we expect about a quarter of uncertainty surrounding any given forecast. We’ve nevertheless kept tabs on the short term market action since. On October 17, we said Not Yet.

The turn turned out to be a week later. On October 27 we could tentatively identify the bottom as having been made on October 24:

https://financology.net/2022/10/19/gold-loses-its-luster/#comment-2651

A few days ago we took a more in depth view of the market picture, particularly the most recent bear market stock rally, in Enjoy The Halftime Show, and followed up this morning with an update:

https://financology.net/2022/11/10/enjoy-the-halftime-show/#comment-2718

The key issue remains the interplay between Fed policy and markets. The Fed wants to see tighter financial conditions, i.e. lower stock prices, before it softens its hawkish stance. Yet stocks rally on any perceived softening, putting such softening further away. So markets are stuck in a Catch-22 where their behavior affects policy at least as much as the other way around.

At the root of it is a fact I’ve pointed out for years but until recently has gotten little recognition: that asset price inflation leads consumer price inflation. The Fed is determined to get the latter down and now realizes it has to go through the former to get there. So as long as this is the case, there is no scenario in which stocks are in a bull market. As a result, there is enormous pressure on the Fed to give up on its inflation fight from Wall Street as well as Washington. And the principal risk to our market scenario is the same as that facing the average citizen, that the Fed yields to this pressure. Yet even if it does, it is by no means a given that there’re not already enough interest rate and yield increases in the pipeline to further pressure corporate profits and stock prices.

Investors also should take notice of the broad and deep inversion in the US Treasury yield curve. The ten year closed at 3.67 today versus the one year at 4.62 … a stunning spread of 95 bp. The thirty year is at 3.85 versus 4.32 for the three month.

In conclusion, the forecast outperformance of bonds appears to be in progress. Although the gold picture is slightly less clear, this most likely extends to gold as well. As outlined in the linked comment, I continue to be overweight both bonds and gold and underweight stocks.

One thought on “Second Half Kickoff”