Let’s take another look at the latest Synthetic Systems forecast, except in the light of what know about the financial context as of April 27. First I want to remind readers of the limitations I described along with the release; see Synthetic Systems 2022.25. There I pointed out that SS doesn’t reflect the impact of events outside the financial system until they have been incorporated in it. The impacts of Covid and Ukraine fall into that category. Covid has been incorporated, but the recent resurgence in China is less certain. The Ukraine war and the ongoing emergence of new responses is far from fully digested.

Another major market influence is the newly hawkish Fed. We have to acknowledge that this hawkishness is for now all rhetoric; concrete policy remains extraordinarily dovish. But this is a different kind of influence than pandemic or war … it does originate within the financial system and should be fully accounted for in SS forecasts. The only caveat to be added there is that as far as the talk goes it’s sufficiently far out in terms of standard deviations it arguably approaches black swan status.

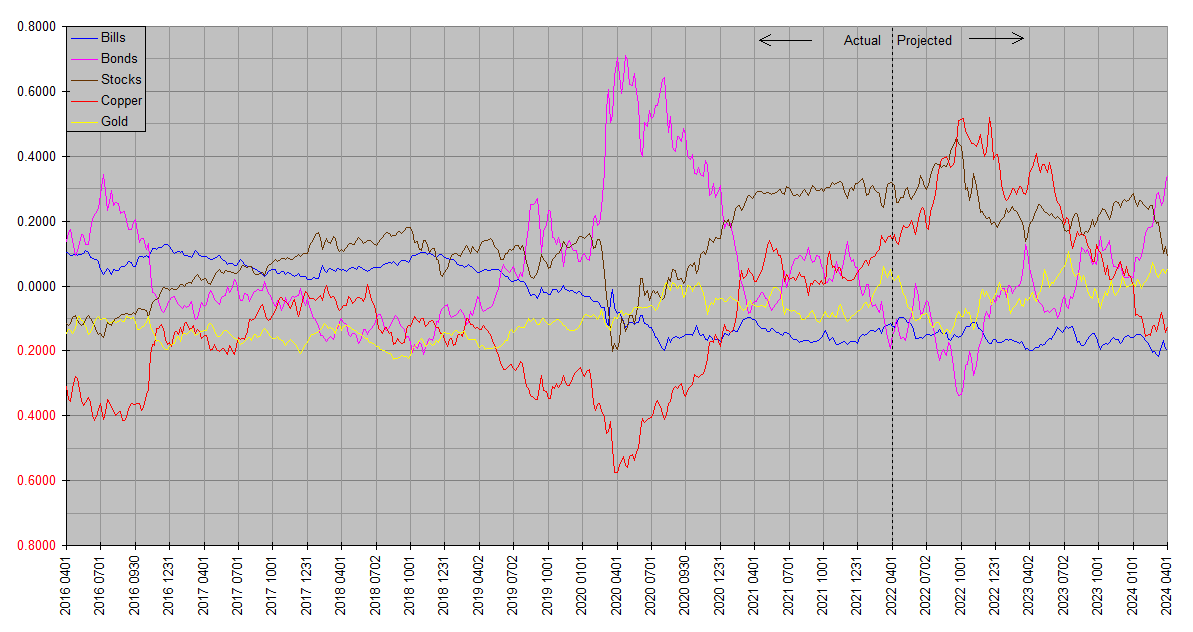

But it’s important to bear in mind that even in the absence of extenuating factors Synthetic Systems is not infallible. It is the best forecasting I’m aware of, but is still only a tool, not a substitute for fundamentals and judgment. It produced stellar results last quarter. It called the bond market crash to a T as well as pretty much nailing stocks, bills, copper and gold. That’s just unheard of in financial forecasting. But that’s why I want to remind readers that such performance is not typical, especially on time frames that short. It’s not even designed to be that accurate on less than a quarterly basis. Moreover with the above factors considered it’s prudent to take the latest forecasts with an extra grain of salt.

Let’s take stocks as an example. SS is unequivocally calling for a summer rally. Yet it’s hard to imagine such performance in light of a Fed that’s barely stopped just short of coming right out and saying it wants stock prices to go down. That’s a tough nut to crack. How might SS err on that front? I can only speculate that there very well could be such a summer rally, but from what levels?

Or maybe against all apparent odds stocks do proceed pretty much as SS expects, and it’s my judgment that’s all wet.

The reemergence of covid in China may be pressuring commodities like copper. Meanwhile the latest action in gold may actually be following the SS script much more closely than it has a right to. It shot up on the outbreak of the Ukraine war, but then sold off, appeared to stabilize, then began to sell off again. We are well within the time frame where we would have to call that a successful call. Gold is trading at a historical premium to other elementary commodities, but has powerful fundamental arguments in favor of owning it. If it does indeed fall much further in price in the coming weeks, those fundamentals will come to the fore and if I’m smart enough will take it as an invitation to increase positions.

Thanks for further elaborating on SS and its strengths and limitations. Honesty in the financial arena is almost non existent.

I once heard an Australian politician refer to another politician by stating that “he’s fairly economical with the truth”. I thought that was a rather diplomatic way of saying “he’s lying”.

commodities [including commodity-related stocks] look like a better bet than equities, both in your ss projections and for fundamental reasons [energy shortages, fertilizer shortages most notably]. today my commodity positions are getting hit, but not as badly as the broad market.

Thanks, JK. Agreed. I see the same thing from another angle … the rising blue line. Commodities are strong but the USD is too, a horse race where each takes turns in the lead. Commodity prices rise or fall depending on whether commodity values or dollar values get ahead by a neck. Own both and your odds of outpacing the equities crowd are pretty good.