It’s become fashionable in the financial press to dismiss the near supernatural level of US stock market valuation by countering that you have to consider interest rates. At these low rates, it’s suggested, stock valuations are reasonable. Whether on price to sales, price to dividends, or whatever, the context of low interest rates means stock prices are just fine at these stratospheric levels.

Let’s unpack this. Given the inverse relationship between price and yield, low interest rates mean high bond prices. The argument boils down, therefore, to don’t worry about high stock prices because bond prices are really high too.

So what’s wrong with this argument? Let me count the ways. First, it tacitly assumes that there aren’t any other investments besides stocks and bonds. Since the total of stocks and bonds in a portfolio is automatically 100%, if bonds and stocks are both overvalued then it makes no difference to your asset allocation. The flaw in this is so obvious no further comment is needed.

Second, there’s a more subtle issue being completely ignored. Even if the only options on the investment menu were stocks and bonds, and that bonds are just as overvalued as stocks or even more so, the argument assumes that a reversion to normality in bond valuations would result in just as large a decline in bond prices as in stocks.

Not so. The reason for this is duration. Bonds are typically much shorter duration assets than stocks. This means that a commensurate rise in yields for both bonds and stocks would result in a much smaller price decline for bonds. A portfolio of Treasuries, for example such as the iShares Treasury index fund GOVT, includes a range of maturities from one to thirty years. While the long end of this range may have durations comparable to stocks, it’s only part of the portfolio; the rest of it is shorter. Even in the event valuations simultaneously contracted in both by the same amount, the bond portion of the portfolio would decline by much less in price. And this ignores the tendency of bonds to zig when stocks zag, that is, a negative correlation over relatively short time frames. The result is that including Treasuries in a stock portfolio – even if they are as richly valued or even more so than stocks – nevertheless reduces risk.

The bottom line is that an overvalued stock market and an overvalued bond market means returns on a portfolio of stocks and bonds are likely to be well below their historic rates. Rather than jump to the conclusion that low interest rates don’t justify caution in allocating to overvalued stocks, isn’t the more sensible takeaway that maybe some other assets should be considered?

agree 100% also wish to add that the negative correlation between stocks and bonds is not a law of nature. there have been periods of positive correlation and, as you say, both are ripe to go down together.

one other thought which i think will appeal to you – although many are waiting for markets to crash, they could just as easily crash via a sharp devaluation of the dollars in which they are denominated.

Right … correlations are certainly not a law of nature. This is why I limited my comment about negative correlation to a “tendency” over “relatively short time frames”. Not only do correlations differ from one year to the next or one decade to the next, but even within a specific date range correlations differ depending on the intervals you choose for analysis. In analyzing any particular range of dates you more often than not find that bonds are negatively correlated with stocks on a daily or weekly or even monthly basis, but that they’re positively correlated over periods of years or decades. For instance bonds and stocks both returned poorly in the 1970s, while they both returned well in the 1980s and 1990s. On the other hand, they sometimes have very low or even negative correlations across even longer time frames, such as the decade of the 2000s. The only broad statement we can make about bond and stock correlations is that they’re low.

What’s “low”? Low enough to provide an important diversification benefit.

Even then, that further assumes we’re talking about Treasuries and other bonds with very low expected default odds. Junk (high yield) bonds of course are much more correlated with stocks. Corporate bonds are more correlated with stocks than government bonds just by virtue of sharing a common issuer – corporations.

The fact that Treasuries and stocks are far from perfectly anticorrelated is another way of looking at the reasoning supporting my concluding suggestion that stocks and bonds alone are not sufficient for a well diversified portfolio and that other assets need to be considered, a point dealt with in more depth in the preceding posts.

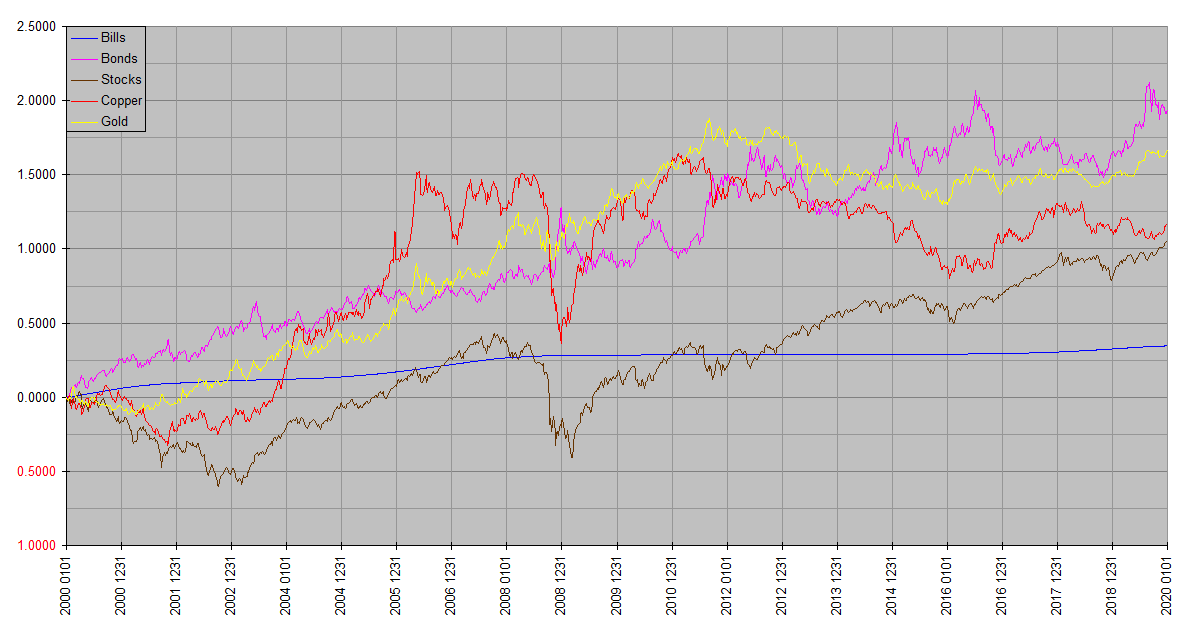

The best way to sum up these relationships may be graphically, as in the post Outlook for the 2020s:

Plotted semilog:

Correlations also vary depending on your choice of unit of measure. As noted in another recent post, physical commodities are highly long term correlated by virtue of being quoted in the same currency, usually US dollars, This ties in with your concluding observation about devaluation or depreciation of currency. If all assets seem to be rising together, it’s generally reflective of a declining value of the unit of account. This is something we’ve even seen recently where stocks, gold and other commodities are all rising in dollar terms. Not surprisingly, since the Federal Reserve has been mounting an all out, $100B a month, drive to inflate asset prices. The Fed can’t actually sustainably make assets worth more, but it certainly has been working hard to debase the security it issues, the US dollar.

low correlation is over long time frames. but given my age i can’t assume a long enogh time frame, so i’m doing more tactical allocation than strategic.

just a remark to any other readers to think about their personal circumstances

It’s the other way around. Generally the shorter the time frame, the lower the correlation. E.g. “risk on” day; stocks up, Treasuries down … “risk off” day; stocks down, Treasuries up. Correlation below zero. Conversely, in the seventies, stocks and bonds both stunk together … eighties and nineties, they both boomed together. Correlation much higher.