Overview

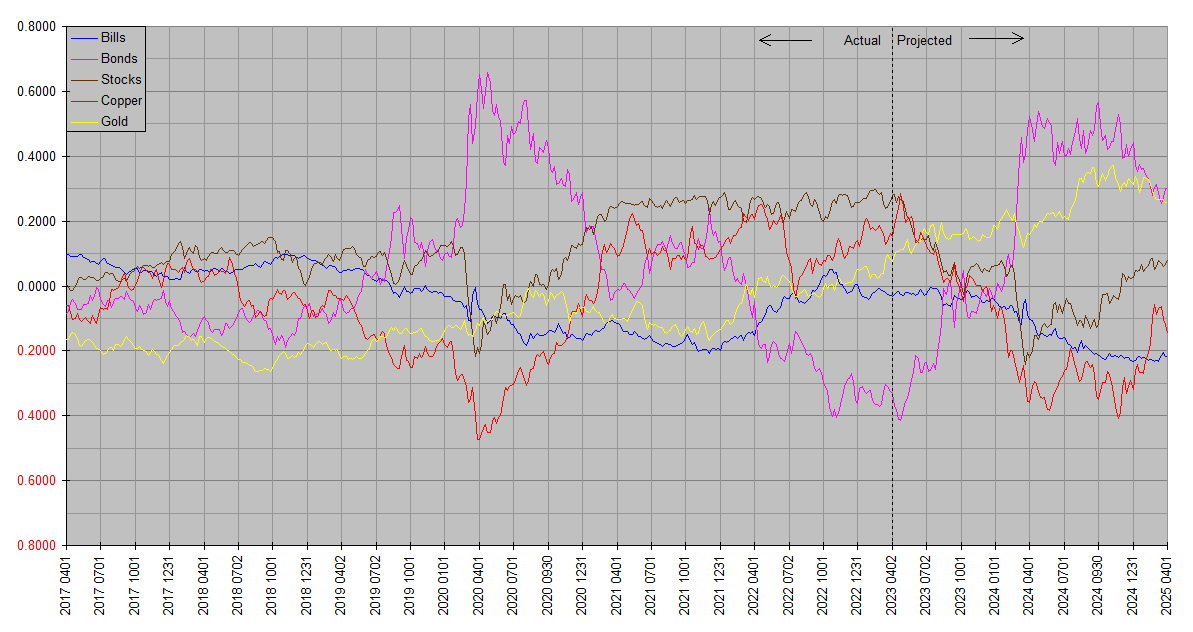

Synthetic Systems is a computer forecasting model covering five asset classes: Treasury bills, Treasury bonds, stocks, copper & gold. The plots are all on the same basis so as to be directly comparable – total return. So the slope of one asset rising more than another indicates outperformance, and vice versa. Plots are in natural log space so that the same vertical increment means the same proportional (percentage) increase regardless of vertical position. The total returns are not denominated in dollars or any other currency, but are relative to each other.

Bills refers to US Treasury securities of effectively zero maturity and duration, similar to a Treasury money market or ultrashort bond fund. Bonds refers to US Treasury securities of effectively infinite maturity (duration reciprocal of yield), but approximates the returns of real world extended duration Treasury funds like EDV, and to lesser extent VGLT and TLT. A broad UST fund like GOVT is around midway between Bills and Bonds. Stocks refers to the entire asset class (not just US or any one country). Copper and Gold represent the respective elementary commodities, except to note that copper is broadly indicative of physical commodities as a class and suggestive of trends in goods and services price inflation.

The charts are best considered together. Annual and quarterly charts are respectively grouped together on dedicated pages under Market Analysis to facilitate this. The forecasting accuracy of Synthetic Systems is best evaluated by comparing successive charts, as the “Projected” time frame of an earlier chart slides to the left into the “Actual” time frame of later charts. Moreover, similarities between the latest update and earlier updates indicate areas of greater confidence in contrast to differences which indicate greater uncertainty.

Readers should bear in mind that Synthetic Systems forecasts comprehensively reflect financial and economic forces (e.g inflation, interest rates, monetary policy, money flows, seasonality, natural resources, technology, demographics, the business cycle, global economic trends, consumer sentiment, investor psychology, momentum, mean reversion, etcetera), but do not reflect external noneconomic factors (e.g. natural disasters, pandemics, unexpected geopolitical disruptions) until they are incorporated into the financial and economic sphere. It’s most applicable over time frames from one quarter year to four years … its accuracy is limited by noise and news flow on the shorter time frames and it also does not attempt to model drivers of longer term returns such as valuations.

Readers are encouraged to consider Synthetic Systems forecasts in conjunction with fundamentals and valuations. Synthetic Systems however often forecasts trends long before the fundamentals fall into place; for this reason it’s useful as a medium term planning guide, with the appearance of fundamentals consistent with a Synthetic Systems forecast serving as confirmation, the lack thereof nonconfirmation. Final confirmation occurs when the trend is actually in evidence.

Discussion

The current forecasts should be taken with an extra grain of salt, especially with respect to the shorter term outlook. SS has missed on the shorter term for a couple of quarters, which generally persists until a more successful forecast is confirmed. It’s particularly missed on Stocks, having predicted steep declines for two quarters which have not occurred. Despite this, SS continues to insist stocks should fall. Based on my experience, SS could easily be correct about its broader outlook for a bear market extending from 2022.75 through 2024.25, but unable to resolve detail. That is, that the prevailing trend is down, but when it’s all said and done, the declines will have been concentrated in lumps, rather than the relatively smooth slope the plots connote.

Why we haven’t seen more tangible evidence of such a bear market is a question about which I can only speculate. SS is likely taking its cue from the massive bear market in bonds extending from roughly 2020.5-2022.75. Mechanistically that left stocks exceptionally overvalued in comparison to bonds, and historically they have tended to follow suit. That is, stocks “should” have responded with a correspondingly massive bear market. That kind of interest rate and yield increases – the rise in the cost of borrowing money – should reduce borrowing, and historically has. My guess is that fiscal policy has simply failed to respond as it rationally and historically has to increased borrowing costs. The US government is the 800 pound gorilla in the borrowing market and has continued to borrow as if borrowing were much cheaper. This has resulted in dollar depreciation – inflation – failing to respond as acutely to rising interest rates and yields as it otherwise would. Corporate sector borrowing may be responding with a longer than usual lag as well due to having taken advantage of ultralow long rates.

This may in turn result in interest rates rising more than they otherwise would. Real capital being finite, the oversized federal demand must result in less capital being available to the private sector. If this hypothesis bears out, either government demand for capital will fall or the private sector will go wanting. This is of course in real terms … in dollar terms the capital available to each can grow via depreciation of the dollar. In other words, either nominal private sector capital will fall or the slack will be taken up by dollar depreciation. Either inflation will re-accelerate or stock prices will resume their decline.

In either case, commodities of finite supply such as copper and gold should outperform. As with Bonds, SS has so far been more accurate on this front. In the case of copper, however, it currently forecasts a deep bear market. Recall however that this is predicated on markets following their logical and historical pattern in response to large increases in interest rates and yields. So if the SS outlook for a deep decline in stocks continues to be off the mark, I expect the copper forecast to be as well.

A depreciating dollar favors strong prices for commodities like both gold and copper, and as well outperformance of foreign stocks relative to US stocks. This we have been seeing … whether it will continue depends on policy variables I can’t predict, but I nevertheless remain convinced either stock prices will fall or consumer inflation will not be brought to heel.

Take your pick.

re the phantom bear market: 3 stocks have accounted for 49% of the ytd gain in the s&p. just 8 stocks have supplied over 100% of the gains. the other 492 stocks are down. narrow leadership, you think?

You can say that again, JK. The US market is narrow as an old world alley. I might have highlighted it except we’re not getting as clear a signal on the global level. The ex-US portion of the stock market often turns down before the US … 2018 was a prominent example. Ex-US powered far ahead of US into mid-January, briefly underperformed as the US megacaps surged, then since has traded in line.

It still has superior long term prospects, but has lost a bit of its edge through this upvaluation. FWIW, I’ve cut my cap-weighted exposure. While the market is roughly 60:40 US:XS, I’m more like 40:60, and have been been more selective on both sides. Especially underweighting non-dividend-paying megacaps using the ETF mix I highlighted earlier. And within the context of some underweighting stocks as a whole.

The hard part is everything has risks … it’s a least dirty shirt kind of environment. Stocks are pricey while corporate profits are vulnerable, cash (USD) doesn’t have the tailwind it had most of last year as the Fed tries to “balance risks”, while a de-dollarization trend is building in international trade, notably visible in gold and oil. Yet with the massive debt burden and rising rates, a deflationary squall could hit at almost any time, so I still want some Treasuries, despite the bleak long term outlook.

Crosscurrents.

Is the dollar or dollars (US) an asset class?

If so, why aren’t they tracked among the other 5 asset classes that you have chosen?

The Treasury bills are the equivalent of U.S. dollars. Note that the explanatory text near the top of the article says they are of zero maturity.

Thanks, Milton … absolutely correct. The Market Analysis page is even more explicit:

“US TBills is calculated at a maturity and duration of zero (no principal change with changes in interest rate), and effectively represents Treasury money markets, US dollars and “cash equivalents”.”

The only performance difference between physical cash dollars and “equivalents” is interest, generally a small contributor to SS plots in the form of a slight slope. Even then, few people use physical cash as an investment … TBills are the “equivalent” of choice.

I think this chimes with what Darius Dale said at the beginning of the year when I posted this…”there will be more tightening for longer than is priced in but it won’t hit stocks till later in the year. That was back in January and he also alluded to how strong both corporate and private balance sheets were and predicted the Fed would exacerbate the downturn by keeping rates higher and for longer than is necessary.

Thanks for weighing in llanlad. The Fed boxed itself into a corner by delaying getting started in reversing the explosive accommodation of 2020 … it practically built in a delay in ending its tightening cycle. Erring only on the side of being too accommodative is an error in itself. The financial system had recovered from the spring 2020 corona crash by fall … stocks had fully regained their losses … yet the outsized ZIRP and QE continued until spring of 2022, by which time the inflation had worked its way through the system and become entrenched in consumer prices. Had the Fed responded more timely it’s unlikely rates would have ever reached current levels. The whole question of higher and longer would have been moot.

Where I part ways with the mainstream is that I don’t see a “recession” as evidence of having tightened too much. The option of controlling inflation without a recession was rejected when the Fed eased too much. When you’re barreling down the highway at 150 mph there’s no way to get back to a safe speed without slowing down.

Enough With The Rate Hikes

So where does that leave us now? Tightening has already hit stocks once, but I agree with your thesis there’s a Round II still to go. Later this year would be consistent with the positioning of the bond market.

Markets Update