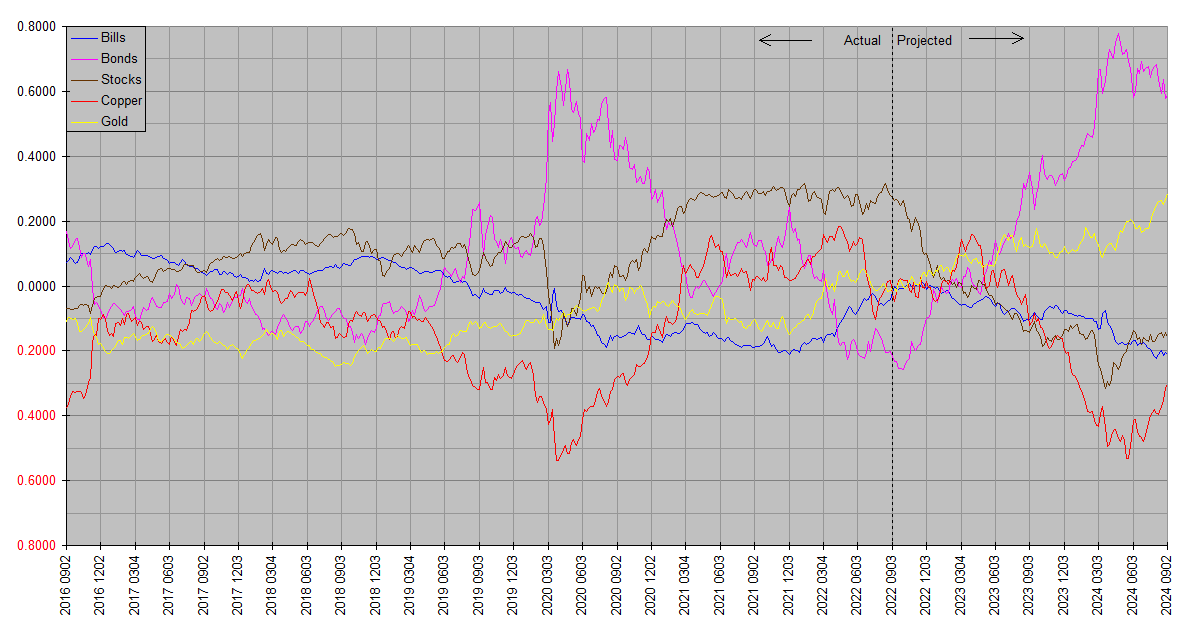

The latest weekly Synthetic Systems.

Apart from the hiccup we cited a few weeks back, SS has been tracking pretty well. The main lingering weakness has been underestimating the strength of the dollar. This shows up in the charts as Bonds, Stocks, Copper & Gold following SS projections closely while Bills rise more than projected. In the tape, where dollar denominated prices are used, prices have been lower across the board than would have been expected based on SS forecasts.

This dollar strength is not confined to the Financology world view. Recall that we use the entire spectrum of assets to gauge the value of the USD, whereas most financial media use terms like “strong dollar” in an exclusively foreign exchange context … i.e. “strong dollar” means merely that the dollar is rising compared to other currencies. But this doesn’t truly tell us much about the dollar, as it could merely represent weakness in foreign currencies. So we use other assets like bonds, stocks, and commodities to assess the value of the USD in asset markets. We attribute the common movement in dollar prices of these disparate assets as reflecting movement in the dollar itself.

As it happens, unsurprisingly these gauges of dollar often yield similar signals. This is one of those times. The dollar has been notably strong both in terms of foreign currencies and in terms of just about everything else. For investors that do their accounting in USD, this appears as falling asset prices.

So while even as most media will look around and conclude asset values are falling, we insist this is illusion due to an expanding unit of measure. When the whole universe of dissimilar assets appears to be moving jointly in one direction, Occam’s Razor dictates we look for a unifying interpretation. All the more so when using different units of value gives a different conclusion.

Of course this doesn’t mean that asset values can’t go down … both phenomena can happen simultaneously. But we can’t emphasize enough that finance is not physics … there are no unchanging units like meters, kilograms and joules to gauge value in finance, so we must dig deeper than nominal prices if we want to suss out what’s really happening to asset values. And no, using the CPI to adjust for “inflation” won’t do the trick, because it’s really only looking at inflation’s exhaust fumes, finding it possibly years after the fact.

It is of course a two way street. When asset prices are broadly rising, it means your unit of measure is falling. This is the more common circumstance, almost universally misbranded as “growth”. But it’s not … it’s inflation … depreciation of currency. It’s just not recognized as such until it spills over into consumer prices … which, as we’ve seen yet again, is inevitable. When asset prices as a whole are going up, concluding that asset values are rising is like standing on the deck of The Titanic and concluding the ocean is rising.

Synthetic Systems does not use dollars or any particular unit for this reason. It instead reports and projects only relative returns, thus avoiding presenting an illusion of something that’s not there.

While we’re focusing on first principles here, there is a timely message. The inflation we’re now seeing in consumer prices is not new. It’s been there for years, merely hiding in asset prices (“hiding” in plain sight, where Wall Street and Washington economists refuse to look!). Had the Fed not indulged in this denial, we wouldn’t have the mess we do now. On the positive side though, these broad declines in asset prices are leading evidence the Fed is winning the inflation battle, despite it not yet being obvious in consumer prices.

are the fed meeting dates an input to ss? as much as i doubt that, the bottom in bonds sure looks like the september meeting.

You could be excused for wondering … it does look like that. I can confirm that SS knows nothing about Fed meeting dates. It also happens to closely coincide with the autumnal equinox, although SS knows nothing about that either.

It’s hard to eyeball on the charts, but looking at the data series behind the plots allows the forecast Bonds minimum to be pegged at October 1. Ten days of course is nothing in the context of the inherent uncertainty of such a forecast … if it actually came within a week or three it would be unusually accurate. Let’s just say that I’d look for the low just about any time between Labor Day and Halloween, if it isn’t already in (or SS is just plain wrong). Also since SS doesn’t plot dollar prices, the dollar low could differ by a bit even if SS hits the bull’s eye (bear’s eye?;-).

Morgan Stanley’s Mike Wilson yesterday was remarkably consistent with the Synthetic Systems outlook:

https://on.mktw.net/3cOrJTU

https://www.zerohedge.com/markets/here-comes-part-two-morgan-stanleys-fire-and-ice

“… While the June low for stocks and bonds was dramatic, we’ve consistently been in the camp that it wasn’t THE low for the S&P 500 in this bear market. Having said that, we are more confident it was the low for long-term Treasuries in view of the Fed’s aggressive action that has yet to fully play out in the real economy…

… In short, part deux will be more icy than fiery, the opposite of 1H22. That’s not to say rates don’t matter – they do – and we expect bonds to perform better than stocks in this icier scenario…”

Wilson also echoes our view of Will Stocks And Bonds Decouple? that corporate earnings will help drive a wedge between stocks and bonds.

It’s not at all unlikely Treasuries do take out their June low … GOVT today is trading a little above that level and VGLT a little below. But taking into account analysis like Wilson’s as well as the Synthetic Systems outlook, Treasuries appear much closer to their cycle low than equities and poised to outperform over the coming quarters.

More support today from Jeff Gundlach:

«The next shock is that we’re having to put in a big overreaction to the inflation problem which we created from our initial reaction of excess stimulus,» Mr. Gundlach says.

«My guess is that we will end up creating momentum that’s more deflationary than a lot of people believe is even possible.»

«As I said, bond yields are probably in the process of peaking out. … That’s why I think investors should own bonds instead of stocks; bonds are cheap to stocks.»

https://themarket.ch/interview/the-period-of-abundance-is-over-ld.7369