The financial media are having a field day over a recent NY Fed survey purporting to show that consumer inflation expectations over the next year have plunged from 6.8% to 6.2% over the last month.

Whoopee twang. For starters, as we’ve pointed out for years, the whole paradigm that consumer prices define inflation has never been established, merely assumed. Next, there is no evidence that “expectations” actually drive inflation … this at best is a theory made popular by the imperative to absolve policymakers from responsibility. After all, the greater extent to which inflation merely a psychological phenomenon, the lesser blame can be placed on policy. That such a theory, if true, would render the existence of a policy apparatus superfluous doesn’t seem to trouble the media.

Finally, the financial media is dominated by Wall Street, and Wall Street is in the business of selling stocks. The negative impact of inflation on demand for stocks has been acutely prominent this year, and with stock prices finally finding a bit of a footing, Wall Street and its media mouthpiece are desperately casting about for any shred of news that might suggest it’s falling. Especially urgent is that the Fed is at its most hawkish in generations, posing a grave threat to stock prices … this is a transparent public relations campaign to lobby the Fed in a more stock price friendly direction. Like so much highly promoted survey “news”, the aim is not so much as to tell its audience what people think as to tell its audience what to think.

None of this is to say that consumer price inflation won’t come down. But that’s contingent on tight financial conditions, as the Fed itself has come to recognize, and that means that if Wall Street gets its wish and stock prices continue skyward, the Fed will have to become more, not less aggressive. So the having of the cake would prevent it from being eaten … not exactly the Goldilocks scenario purveyors of stocks dream of.

Timing is tricky. Inflation doesn’t move from asset prices to consumer prices overnight … it filters through a little bit at a time … from weeks to months to years. The response to commodity prices is quicker, but nevertheless still not immediate. The cooling of commodity prices since spring could affect tomorrow’s CPI print even as prices have more recently rebounded.

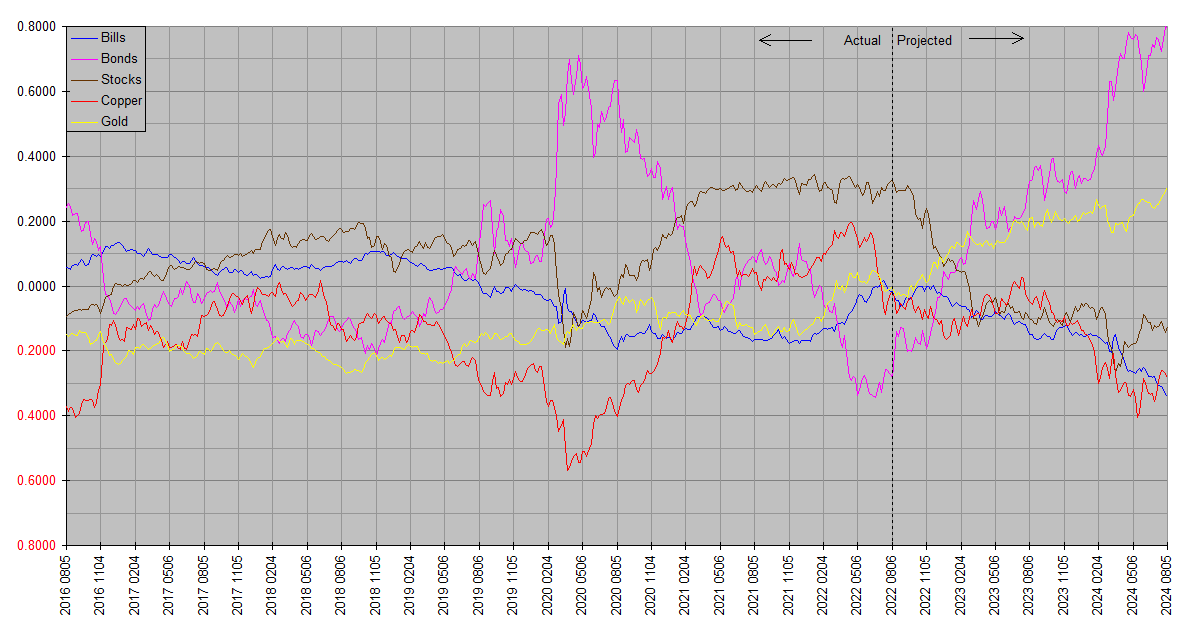

Yet a softer CPI print could fuel speculation of a less hawkish Fed and depress the dollar, sending nominal stock and bond prices higher. This in turn would mean upward pressure on future CPI data and, paradoxically, a more hawkish Fed. Sorting out how these countervailing pressures are likeliest to play out over time is too much for my mere mortal mind … we’ll leave that for Synthetic Systems.

“Yet a softer CPI print could fuel speculation of a less hawkish Fed and depress the dollar, sending nominal stock and bond prices higher…”

And that’s exactly what we saw this morning with the yoy roc CPI report of 8.5%. Although this would have been received as shockingly high mere months ago, it is below last month’s 9.1% and expectations in the 8.7% area. The USD sank against stocks, bonds, copper & gold as markets priced in a marginally less hawkish Fed. This is also consistent with the SS chart showing Bills retreating throughout this month.

The next regular FOMC meeting announcement is scheduled for September 21, and there remain additional monthly reports on both employment and inflation before then. But based on what we know today, I suspect the Fed isn’t pleased with the market reaction and wouldn’t be surprised to hear some pushback in the coming hours and days.

Notably, we can add to that list oil prices … they had earlier traded down from yesterday’s close but at last check are solidly up. This further confirms the paradoxical inflationary implications of the market reaction to a modestly disinflationary CPI print.

as ss has predicted for quite a while, it looks like we’re in for an exciting october.

Well at least the October forecast is exciting;-). We can be sure reality will depart from SS in some way, but where, how and how much is an open question. But at minimum I think we are looking at an “interesting” fourth quarter, and would be surprised if treasuries didn’t outperform stocks between now and April.

As it relates to the current data, the scenario most consistent with SS is where the Fed remains unmoved by the CPI rate downtick. That’s also consistent with the Fed’s recent rhetoric and that’s what I think it should do. But I want to emphasize that SS doesn’t share any of my biases … it is purely a ‘just the facts’ proposition … however accurate or inaccurate it may be, it is completely objective. Its current outlook is also consistent with the deeply inverted yield curve.

What’s your take on the economic outlook JK? Personally I think the “recession” question boils down to how you define “recession”, but that still leaves unambiguous data like the course of the CPI, the unemployment rate, etc. And of course the path of asset and commodity prices…

when i look at this graph

https://static01.nyt.com/images/2022/08/09/business/inflation-overall-promo/inflation-overall-promo-threeByTwoMediumAt2X-v3.png

i’m impressed by how the markets will grasp any straw and run with it.

Great chart JK! Notable absence of any big CPI spike not accompanied by a major bear market in stocks. Especially given valuations, it’s hard to imagine what we’ve seen so far this year as adequate, absent a whiplash-inducing about-face from the Fed.

re: “recession”

i’ve been mulling over the jobs numbers and read somewhere a comment that if we could have a “jobless recovery” as occured after the gfc, perhaps we could now have a “jobless-less recession.” this would be a function, mostly, of demographics: the higher level of pandemic-triggered retirements among boomers. the lower participation rate among even the prime working-age population. thus unemployment numbers would remain low even as the economy contracts. if so, i would expect a long duration but shallow recession, a perfect setting for slow but prolonged financial repression. it’s not clear to me how this would be manifested in the financial markets. got any thoughts? [i guess ss is your thoughts.]

The thing that strikes me about the “real economy” is that there has been so much excess demand for labor that it could fall a lot without a dramatic increase in unemployment. Demand just catches down to supply. Unemployment could rise moderately just reflecting a more normal labor market … 5% would hardly be a disaster. Getting there might technically qualify as a “recession”, but a healthy one like being on the highway slowing down from 120 to 80.

The catch to this goldilocks scenario is what stops interest rates from rising? 2% is a long way down from 8%+. Have we ever had a several point decline in consumer price inflation while Goldilocks just enjoys a nice afternoon at the park and a smooth ride down the slide? And we either get down at least to ~4% before the Fed could colorably justify easing off the monetary brakes … or there is a financial accident.

What we’ve been seeing is just so reminiscent of 2008 … rising consumer inflation, bubbly housing market, stocks peaking last fall, energy prices soaring into mid year … except for one thing … an obvious focal point like subprime. Sure the banking system is much more solid, but so much of the financial system has moved out of the banks, and we know that debt and leverage is massive. And things you never heard of have a way of surfacing fast and causing market mayhem in short order like LTCM.

So what causes rates to stop rising is either inflation makes an unprecedented smooth disappearance or there is a financial accident, for which there is ample precedent. The SS forecast would be consistent only with the latter.

i keep coming across comments about a lack of liquidity, even in the treasury market. and isn’t it next month that the fed is supposed to jack up qt to a full $95b/mo? i suppose a liquidity squeeze would show up in rates, but maybe it would be in the repo market like 2018 [although it was only after equities swooned a few months later that powell pivotted]. i’ve read of an increasing number of fails in repo.

also qt includes either rolling off or selling $35b of mbs per month. that should further squeeze the mortgage markets, raise rates further. i’m under the impression that real estate is currently in its frozen phase, with significantly fewer closed deals as sellers have yet to accept that their prices have to be adjusted for higher mortgage rates.

so there are 2 candidates for a financial accident.

The relationship between Fed buying and selling UST and rates is complicated. At first blush you’d assume buying (QE) would raise prices and depress rates, and selling (QT) would depress prices and raise rates. And it probably would if Fed volume was overwhelming all else. But it at least as often as not seems to have the opposite effect. Fed buys bonds, markets go “risk on”, stocks go up. And vice versa. It ironically negates the stated purpose of QE … to lower rates out the curve.

I don’t worry too much about Treasury liquidity … the ones complaining are probably trading eight-nine figure blocks. And it cuts both ways anyway … unless you see asymmetric illiquidity – eg easy to buy but hard to sell – the effect on rates should be negligible. And if you do see that, prices ought to adjust quickly to the point that buying and selling liquidity balance. Unless something is getting in the way of price discovery, and as far as we know even the Fed isn’t doing that … QE and QT by definition target quantity not price.

So while the Treasury market itself doesn’t, the repo and mortgage markets look like candidates. Yet there are still others … some kind of China blowup, a mega Orange County, derivatives debacle, currency run, hyper-leveraged hedge funds…

Even putting SS completely aside, I can’t help but suspect some kind of blowup is bubbling up under the crust. Deeply inverted yield curve, Fed poised to lift short rates higher than any time in years … and even if it didn’t, you’d have to wonder what turned it around. Sure, we had a softer CPI print, but the market reaction lifted oil right along with stocks … can’t be pleasing Powell & Co.

i think we need to add european banks to our list of crisis candidates.

I haven’t been following European banks.

What are you seeing?

here’s a thread worth reading re the effects of qt:

https://twitter.com/concodanomics/status/1557495348704198656