Three months ago Financology declared a bear market in force for stocks and bonds. If anything it’s intensified since. Given the recent market turbulence, let’s do a special update of Synthetic Systems. The focus here isn’t the forecasts – they haven’t changed much – but on recent market activity … we want to assess how closely the SS forecast is tracking. Is it still valid? Or have events gone so far off the rails that its guidance has too?

We have at least two major extraneous processes at work … the collision of China’s Zero Covid policy with a Covid resurgence and Russia’s Ukraine War with an extreme western response. In addition we have Federal Reserve policy that, while intrinsic to the economic and financial system, has been so far removed from historical experience as to behave in a quasi-extrinsic way. It seems possible these developments could stress SS to the point of failure. So let’s take a look and see how far on or off track SS is so far.

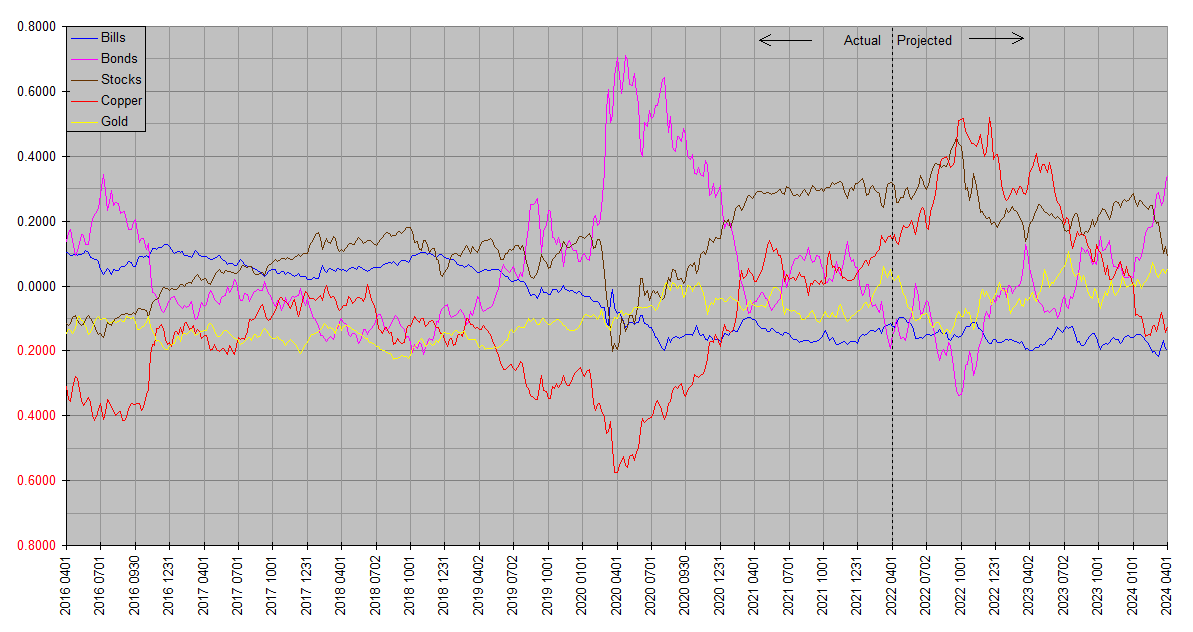

Hmmm … not as far off as you might think. The action is in the blue line. Stocks have barely sold off in real terms, but the dollar has risen sharply. It takes fewer dollars to buy the same stuff, so you get lower prices. Nominal bond prices have sustained a double whammy, having plunged in real terms and declined nominally versus the rising dollar.

Let’s take a fresh look at the FDI for a bit more color.

Here we see a similar picture. The dollar has been appreciating, and at an accelerating rate into this past week. Not to raise alarms, but the picture bears a close resemblance to the early days of the 2008 crash. Compare the far right part of the plot with the far left part. In both cases there is a transition from a steep inflationary decline to a deflationary rise.

The FDI by itself sheds no light on whether this rise will reverse imminently or accelerate further into a 2008 style spike. Synthetic Systems however weighs in on the side of reversal. In which case the recent dollar surge would pivot into a decline, manifested in a sharp rebound rally for stocks, bonds and commodities. This could easily kick off as soon as early next week.

My conclusion is that such a scenario shouldn’t be surprising at all. Yet at the same time the factors identified above, exogenous and quasi-exogenous, are undeniably at work and throw more than the usual amount of doubt on the reliability of the SS outlook. Not to mention that we’re putting a lot of stock in a very short time frame well below SS’s range of competence. My instinct and experience suggest that the forecast summer rally in stocks and commodities is still in play, but that the question of from what levels is quite open. I’m still stoutly overweight cash but have far from completely exited stocks and maintain around neutral allocations to bonds and commodities including gold.

Difficult as it may be for the investorate, the rising dollar and nominal declines in asset prices to date are a silver lining for inflation. The most positive development on the latter front would be if that summer rally for stocks and commodities does not materialize, or that it springs from much lower levels. If SS turns out to be correct and it does come to pass, the likelihood is that the fall declines SS has penciled in will be devastating and that we are indeed courting a 2008 like scenario or worse.

Thank you, Bill. Much appreciated as always.

Thanks, Amrit!

“In which case the recent dollar surge would pivot into a decline, manifested in a sharp rebound rally for stocks, bonds and commodities. This could easily kick off as soon as early next week…”

There is a potential catalyst in tomorrow’s CPI report. If it comes in substantially below last month’s 8.5% YOY rate, it could light a fire under depressed markets. Ordinarily that might not be the case, but the markets are deeply oversold and the reaction could be exaggerated. The financial media would likely take a softer advance as a victory narrative and a sign the Fed will be less aggressive. As usual, whether that narrative is accurate is secondary … markets looking for an excuse to rally won’t question it too deeply.

Conversely, a hot CPI report would be like throwing a lead weight onto a sinking ship. That’s a less likely scenario though … although it’s very early, the first tentative incursions of the rising FDI could have begun to filter into consumer prices and offer a bit of relief. The bigger risk is that the rebound in asset prices is more than temporary and consumer price trends again worsen.

Thanks for your ongoing updates… Just thought it might be good for you to know that there those of us out here who often read but infrequently comment.

Thanks, Peter!