A couple weeks ago we updated the Financology Dollar Index (FDI), showing a decline in the rate of inflation. The index itself shows the level of value of the dollar. This is comparable to the level of the CPI (inverted).

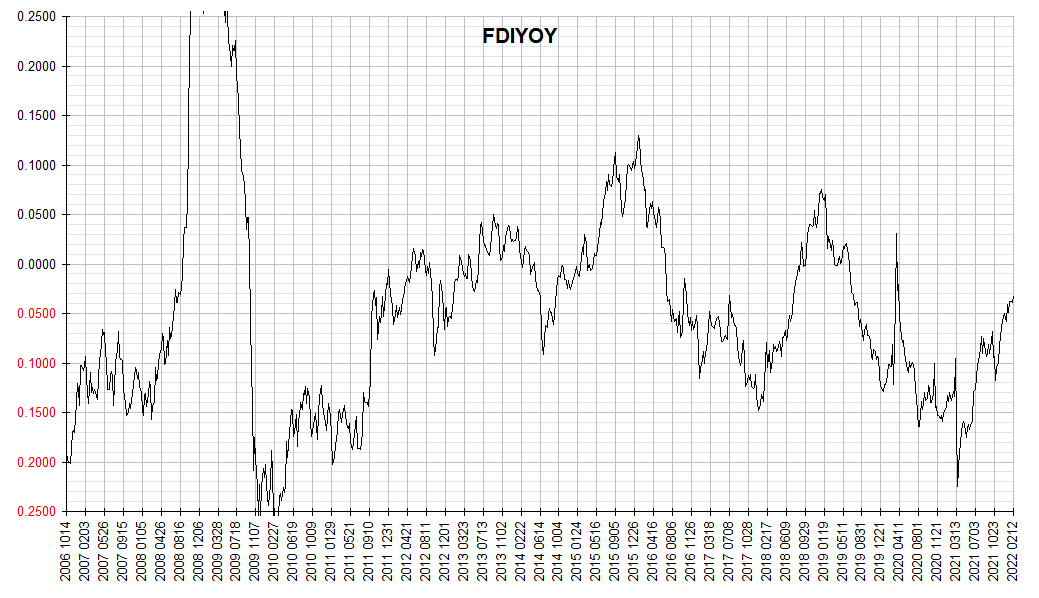

This week we cited the latest reported year over year change in the CPI. This is not directly comparable to the FDI itself, but we can analogously plot the year over year change in the FDI. The 800 week chart of the FDI itself hasn’t changed much over the course of a mere 2 weeks anyway, so for this FDI update let’s instead plot the annual change in the FDI.

We can compare this to the reported change in the CPI. Reading from the chart source data, the latest value is -0.0319. We don’t want to put too fine a point on it because the weekly data are volatile, so let’s say this indicates a loss in market value of the US dollar of 3.2% over the past year.

Put another way, the year over year rate of inflation is 3.2%.

This is actually less than the reported CPI increase of 7.5%. The rising trend of the FDIYOY indicates inflation – as measured by the rate of decline in the market value of the dollar – is falling.

This stands in stark contrast to the widespread characterization in the media of increasing or accelerating inflation.

Note that this method of processing the FDI invokes some of the same weaknesses of reporting year over year changes in any statistic like the CPI. It is prone to so-called “base effects”. That is it’s equally sensitive to changes that occurred in the year ago base period as it is to changes in the present. Notice for example the sharp bottom in the FDIYOY in March 2021 … this reflects the sharp peak in the FDI in March 2020.

It also introduces a half period delay … since we’re finding the change from one year ago to the present, the center of the period being examined is actually one half year ago. So, as with the latest CPI report, the current year over year data point does not tell us the current rate of inflation, but that around six months ago.

But with these issues in mind, it’s nevertheless clear that the rate of inflation has been declining. As we’ve explained before, consumer prices are lagging indicators. It’s also safe to say the rate of inflation peaked in the second half of 2020.

Let that sink in. This is how far behind the curve the Fed is. The rate of inflation peaked in the second half of 2020 and the Fed is responding in the first half of 2022.

So what are we saying here? The Fed should abort its hawkish policy shift? No, because the main reason the inflation is waning is because the bond market has already hiked rates. If the Fed were to fail to follow through, inflation would turn up again. But we are saying that if it does follow though, it won’t need to hike anywhere near the 6-9% range that some pundits are pegging based on flawed theories about real rates based on CPI data. And we’re saying that an awful lot of trouble could be avoided if the Fed quits the habit of falling behind the curve.

The yield curve indicates Fed funds should already be in the 0.75%-1.50% range. The Fed could get there very quickly, except for another bad habit … assuming short term rates should move only in long, unidirectional cycles. What is the basis for such an assumption? Nothing but dogma. If there is a rational case behind it, it’s one of the best kept secrets in economics. Fed funds at 0.75% tomorrow would be utterly no problem at all, except that if the Fed did that, markets would freak out trying to handicap how much more it had up its sleeve for the next twelve months.

Instead of plotting a whole course of policy for months at a time, why not just adjust Fed funds at every meeting? For that matter, why not every week? Nothing about the next move implied. End this ridiculous obsession with how many quarter point moves will happen in 2022. What market ever acts like that in real life anyway? As Financology has stated for years, the Fed should confine policy activity to the buying and selling of Treasuries and gold, and leave the determination of short rates up to the market. Next best thing would be to at least let them look like a market.