Fed head Jay Powell made the news a couple of months ago when he said it was time to retire the term “transitory” as applied to the wave of inflation. But as we have been saying all along here at Financology, the inflation will indeed be transitory … as transitory as the policies causing it. Powell wasn’t wrong when he said it would be; he was merely wrong in suggesting it would go away by itself. The Fed would have to begin to reverse its massive money printing and interest rate repression.

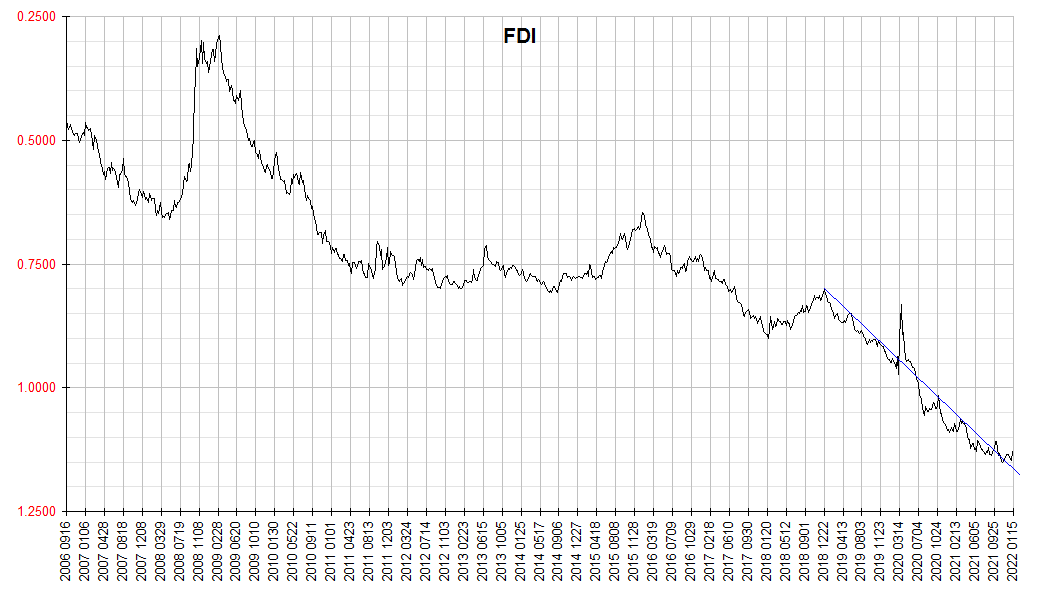

The latest FDI update shows the first tentative signs of progress. Notice at the far right of the chart the steep plunge in the market value of the dollar has begun to moderate. The Fed may have yet to put its first rate target increase in place, but the bond market has already begun the job for it, and QE tapering is in progress. So long as the Fed follows through on its rhetoric, it will succeed in taming inflation.

We have to recognize, however, that conventional inflation metrics lag badly. The FDI in contrast is a coincident indicator. This means the inflation it registers will take time to be reflected in lagging indicators like the CPI. So it’s quite possible CPI growth will continue or even increase before following suit.

As an interesting aside, note that the wave of inflation being tamed did not begin with covid. It began in late 2018 as the Fed abandoned its last policy normalization effort. It was interrupted by the deflationary crash (FDI spike) associated with the outbreak of covid but reaccelerated by the policy response.

So how far does the Fed have to go to mission accomplished? Some analysts have suggested it needs to get real Fed funds positive. We could nitpick that assessment, but it’s a very empty one, because it fails to define the inflation rate against which Fed funds is compared. With CPI growth in the 7% range, they come up with Fed funds in the neighborhood of 8%.

This is the kind of garbage economists excrete when they ingest faulty premises like CPI=inflation. Fed funds lives in the capital markets. The yield on the S&P500 is in the neighborhood of 1.2%. The yield on the ten year treasury is around 1.8%. Foreign stocks yield in the neighborhood of 3%. These are the relevant neighborhoods. So the Fed need only get Fed funds somewhere into the 1.5%-3.0% ballpark to be competitive. Even 1% will mark substantial progress. The exact level is a moving target but will be apparent when it is approached.

From there, it gets easy. The Fed then just needs to renounce interest rate targeting altogether.

re: how far the fed has to go to reach “mission accomplished.”

i do not believe they will ever go far enough for long enough until there’s been sufficient inflation to lower the gov’t debt/gdp ratio to perhaps 80%.

That would be like a dog chasing its tail. The Fed cannot get the debt/GDP ratio down with artificially low interest rates alone because the selfsame artificially low interest rates encourage more debt accumulation.

In other words, ultralow rates are the first cause of excess debt. Paradoxical as it may seem, rate normalization is a precondition for getting debt under control.

A popular meme holds up the post WWII experience as precedent and assumes interest rate repression will work the same way as then. But that glosses over the fact that the core ingredient in the WWII debt cure was ending the war. Interest rate repression only aided because the problem underlining runaway debt accumulation was addressed.

I think the Fed has the opportunity to succeed. Among other things, President Biden has actually come out in support of its efforts to rein in inflation. This is an encouraging development, not seen since President Reagan gave the Volcker Fed similar cover four decades ago.

This leaves Wall Street as the main corps of resistance. It will ultimately set a limit of how far the Fed will go, but there is every reason to believe that limit is much greater than before.

My point above is that it will not take as much as some fuzzy-minded economists project. Again, it’s a moving target, but my best estimate is that short term rates in the neighborhood of 1.5% would be enough to fully arrest the inflationary juggernaut. That’s within shooting distance of the 1% hiking already widely anticipated this year, yet not enough to be a budget buster for the Treasury.

the correlate to ending wwii will be the death of the baby boomers, relieving the stress on social security and medicare costs. that cohort was born between 1946 and 1964, so they are currently 58 to 76 years old. by around 10 years from now let’s assume the first wave is dead, or at least decimated. at that point the expenses are going down. that also correlates with what neil howe predicts will be the resolution of our current 4th turning. interesting times ahead.

Demographic shifts are overrated in comparison to the size and scope of economic financialization and the effects of fluctuating interest rates. They pale next to the difference between double digit interest rates and low single digits. I fear demographics are being hyped as an excuse for not examining more sustainable solutions. The passing of the baby boom bulge will be followed by subsequent declines in the birth rate resulting in fewer people paying in, along with growing life expectancies. But Social Security is a bedrock government program counted on and popular with millions and has to be strengthened, not hollowed out.

One big problem is that so far Treasury has missed multiple opportunities to issue fifty and hundred year bonds at historically low rates. Those are generation bridging time frames, capable of smoothing out fluctuations in birth rates and life expectancies. It’s excuse of having done surveys and not seen enough interest from bond dealers is weak. Why not issue a few and see what the actual market response is? If rates came out too high there’s nothing to prevent reducing issuance. I’m afraid Wall Street is being allowed to run a show that is better left to the long term interests of the American people at large.

By far the more important priority should be getting the economy back on track. With a sufficiently robust economy and sensible fiscal and monetary policy these budget problems could practically take care of themselves.

issuing a few very long duration bonds to test the market sounds sensible, but i’m afraid that the market isn’t there, like the emperor’s new clothes. right now everyone can maintain the fiction that long rates are as they should be, i.e. that it’s a real market. but i think the fed itself has bought much of the long paper and the rest resides with pension funds, insurance funds and so on which are mandated to hold such paper. if the treasury holds a long dated option and it is poorly received, i think the wheels will come off treasury paper in general, and the currency as well.

Yeah Mnuchin mumbled something like that when he passed on longer dated bonds. Easily explained by his being too close to Wall Street. Although Yellen is no better, having all the vision of Mister Magoo. It’s the same kind of short sightedness that, by concentrating its issue at the short end of the curve, has already cost Treasury so much in terms of missed opportunity to lock in so much debt so cheaply for so long. By extension, the risk of issuing a bit of fifty and hundred year paper, even if only to test the waters of the real world, pales in comparison to the opportunity cost of failing to do so.

The worst case scenario is it falls back to the Fed to absorb some of the issue. So what. As a vocal Fed critic I think I often get pigeonholed as an opponent of QE. I actually don’t have much of a problem with QE so long as the Fed confines its activities to Treasuries and gold. The dollar gaining value? Buy. Losing? Sell. Child’s play.

Interest rate targeting gets a pass because it’s been done longer and has become viewed as conventional. But it’s far more destructive. It obliterates the price signals that form the neural network of the financial system. QE by definition instead fixes quantities and lets prices do what they may. It’s interest rate targeting that the Fed used to back itself into the corner from which QE emerged and encouraged debt to grow to an existential threat in the first place.

Treasury and Fed. Of Wall Street, by Wall Street, and for Wall Street.