Framework makes a difference

Let’s start with the usual way of thinking about investing. The basic framework is you put your savings into cash. At some point you’ve accumulated enough to start investing it. Some long term goal such as retirement often motivates this move. At that point you’re not just stashing away money for the future but hoping to earn returns on it, making it grow. You’re taught that in order to do so, you must take risks, accepting the possibility of loss in exchange for the hope of gain. In this paradigm, the investment menu divides into safe assets such as cash and risk assets such as stocks. How you allocate between them determines how much risk you’re taking on in pursuit of return.

There’s just one problem with this mental model … it’s a grossly distorted way of looking at the investment world and can lead to poor decisions about how to save and invest.

There’s a better way. Take a step back and reflect on it … a deeper view of the financial world reveals that there is no such thing as a safe asset. If you have any assets at all, there is no such thing as being uninvested. The only way to invest in nothing is to take a vow of poverty and join the brotherhood.

Cash is a security

The biggest challenge is overcoming the assumption of stability in cash. Own securities issued by General Motors or Microsoft, and you’re assuming risk. Stay in cash and you’re not. At most in cash you’re just failing to keep up with inflation. You may not earn returns, but you’re avoiding all volatility.

A little reflection reveals that this is just an illusion. In fact cash is a security too … in the case of dollars, one issued not by General Motors or Microsoft but by the Federal Reserve. No need to take my word for it; just take one out of your wallet and read the inscription: Federal Reserve Note.

But isn’t it still fundamentally different than other securities? After all, they can be volatile, jumping up and down in value, while dollars just sit there doing nothing. No, it’s pure illusion. The apparent stability is an artifact of our choosing them as our unit for measuring value. If we were to choose to measure value with shares of GM or MSFT, their volatility would disappear too. Instead we’d think our dollars were jumping around. In fact, without taking on an exhaustive analysis, there’s no way to tell just how much of the apparent volatility in GM or MSFT shares is really volatility of the shares themselves and how much is volatility of the dollars you’re measuring them against.

Financial Relativity

There are simply no absolute values in the asset world. All are relative … merely the ratio of one value to another. The price of oil is not the value of oil, but the ratio of the value of oil to the value of the currency in which you’re pricing it. The value of the dollar is as much a participant as the value of the oil.

What about physical commodities like gold? They are not securities. Given its multi-thousand-year history of use as money, gold is arguably a better candidate than dollars as a default asset … the thing you put your savings in when you’re not aiming to invest. But even gold is volatile … even over decade time frames it can decline in real purchasing power.

See where this line of reasoning is going? Instead of deciding how much of your portfolio is invested, realize that all of it is, and that the real question is in what. Instead of thinking how much is exposed to risk, realize that it all is, and that the real question is what kinds of risk. Dollars, stocks, bonds, funds … to properly evaluate them is to put them all on the same footing, and avoid the temptation to pigeonhole them into risk on, risk off, or whatever misleading misclassifications the financial media may apply.

It’s easier said than done though. Our entire lives have been spent using our currency as a unit of value, and after a lifetime of immersion it’s a hard habit to avoid. Your bank, your broker, and anyone else that handles your finances reinforces it with every statement. But your ability to clearly understand your finances depends on your ability to see through it.

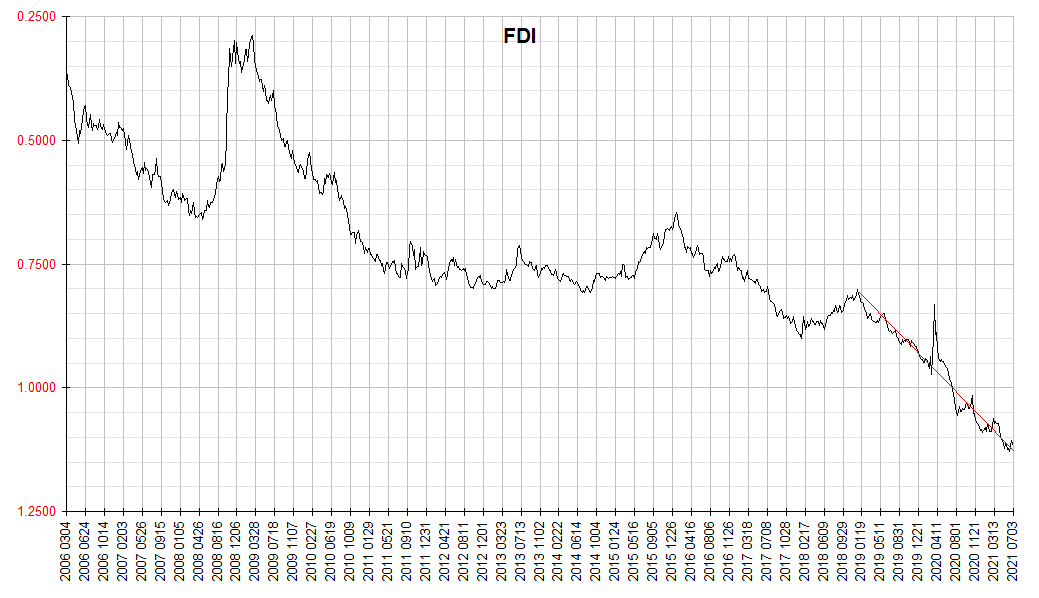

We have tools that can help. In fact, besides just measuring trends in purchasing power, this is a key raison d’être for the Financology Dollar Index. In many Financology articles, we focus on using the FDI to measure the rate of inflation, that is, the rate of depreciation of the US dollar, or to identify spells of the opposite, deflation, or increases in the value of the dollar. But the charts also reveal high frequency volatility … as a weekly index the FDI resolves “inflation” and “deflation” on a weekly basis.

This raises an interesting contrast with the conventional take on inflation and deflation. Conventional measures such as the CPI (which I would argue aren’t even proper measures of inflation, but rather of consumer prices), are only calculated on a monthly basis, using averages across a month. Even then the “inflation” rate extracted from them is usually reckoned over longer time frames like a year. This gives the impression that inflation is a slow moving, evolving phenomenon that lacks volatility. As if it’s something that happens to “the economy”, not merely the currency. But is this because inflation is really that way, or just because conventional metrics are only designed to measure it that way?

The terms “inflation” and “deflation” are convenient, but have accumulated so much baggage our understanding of the economy and markets would be clearer without them. It would be better to talk about dollar depreciation and appreciation instead. Inflation, stripped of the excess baggage, is nothing more than a bear market in currency.

Investing through a clear lens

So how might this affect how you invest? For starters, it should make securities investing less intimidating. If you have cash, you’re already doing it. Including stocks or bonds is just adding new categories of securities.

If you’re properly diversified, it should make you less fearful of losses. If you have for example a Permanent Portfolio type of asset mix, with 25% each in cash, treasuries, stocks, and gold, or an even more broadly diversified global market portfolio, the majority of any losses as measured in dollars are arguably fictional … due to one of those occasional bouts of dollar appreciation. Although such accounting declines are unlikely to persist, even if they did you would soon likely see prices of the goods and services you buy decline in kind … leaving your real purchasing power intact.

You also might be less inclined to be taken in by tales of impressive historical stock market capital gains. While individual stocks and sectors have departed materially, most of the price returns of the stock market as a whole are mere artifacts of currency depreciation … when the value of currency falls it simply takes more currency units to buy the same stuff …and stocks are no exception. In other words, most of the stock returns you see cited are just inflation. Even most so called “real” return data are inflated by virtue of understating inflation.

This spurs the realization that most of the real returns on stocks as a whole come from dividends. With this knowledge, you can readily see that at current prices, at which the S&P 500 yields only about 1.4% … far lower than most of its history, the real return potential from owning this index is also far lower than most of its history. Without having to analyze sophisticated arguments about valuations. You would also see that bonds yielding 1%-3% are likely to produce negative returns if held for the long run. You’re unlikely to be comfortable holding the majority of your nest egg in cash either. As you can see from the FDI, dollars are usually in a bear market, punctuated by occasional and brief bull markets. And since stocks, bonds and cash have bleak long term return prospects, you might also be more inclined to consider investments outside the traditional financial asset arena such as commodities and realty. At least you will have a better appreciation for the value of diversifying your investments across the asset classes … that no one asset is safe and that safety can only be found in combining assets.

It also opens up a new perspective on how to improve returns. Warren Buffett has said his number one rule of investing is don’t lose money. And that rule number two is don’t forget rule number one. That’s pretty emphatic advice from one of the most successful investors of all time. But if Buffett only thought of “money” as cash, he would never have achieved that status. In our enlightened way of thinking about investments, it becomes apparent that one of the surest ways to succeed is not to focus on which of the asset classes seems most likely to gain and put all our chips in it, but to think about which of them seems most vulnerable to loss and check our exposures. It may seem counterintuitive, but one of the most powerful keys to gains in investing lies in minimizing losses. Defense is the best offense. With this framework for thinking about prices and values, we have a clearer view on what that means.

This might be the most astute financial observation and best financial advice I’ve ever read. Thank you!

Thanks for the kind feedback, Amrit. This perspective is a recurring theme on Financology, but this is the first time I’ve devoted a post to developing it from first principles and connecting it to investing. I’m glad you found value in it.

Nice answer

back in return of this question with real arguments and explaining everything

on the topic of that.