Some assets are popularly regarded as strong inflation hedges, while others are less so. But if we look closely, some of those differences don’t represent degrees of strength, but effectiveness at different phases of the cycle.

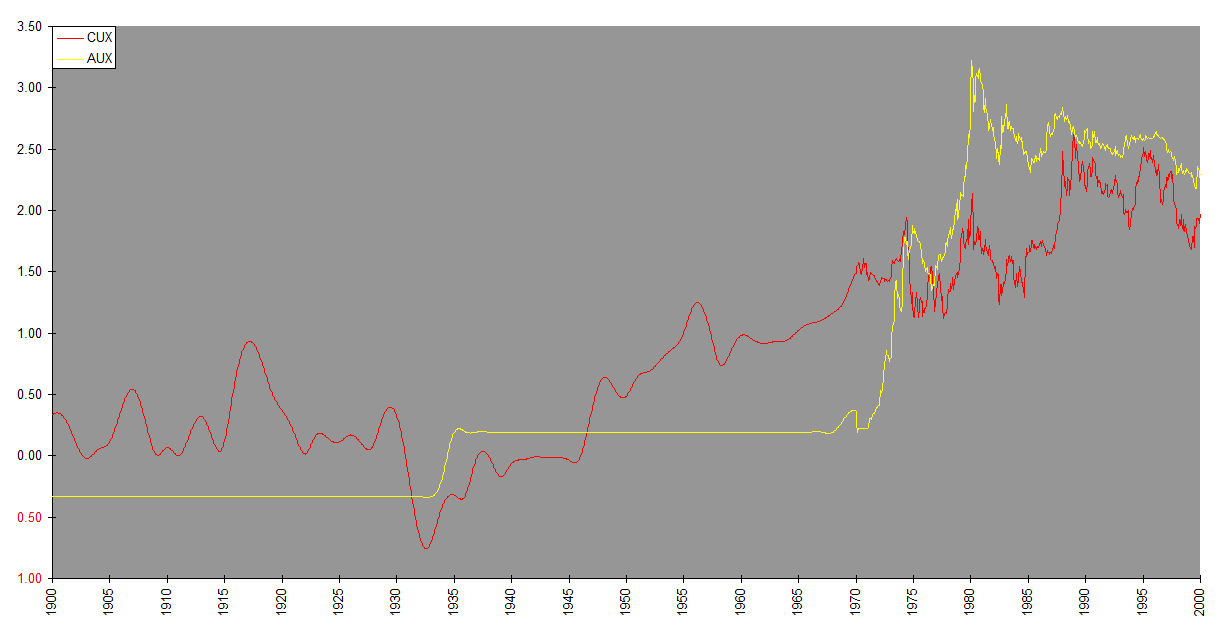

To illustrate, let’s compare the effectiveness of copper and gold as inflation hedges. Below is a chart of copper and gold prices for the twentieth century. They’re log scaled and vertically shifted to facilitate comparison.

Gold has a strong reputation as an inflation hedge, while copper is instead regarded an indicator of economic “strength” (whatever that is). This is due partly to the tendency of gold to correlate more closely with bonds while copper correlates more closely with stocks. Stock investors therefore benefit more from leaning on gold. Copper would be more useful only in portfolios dominated by bonds.

This chart shows another reason. During the infamously inflationary 1970s, gold prices shot up far more than copper prices did. This, even more than the aforementioned, explains gold’s reputation as an inflation hedge. But was this because gold is inherently a better inflation hedge than copper?

No. It was a function of gold prices having been pegged during the prior era. This first supported gold prices, in the deflationary crash of 1929-1932, then suppressed them for decades afterwards. Copper meanwhile was free to respond to market forces throughout. Look at the chart, especially the period in the middle of the century, before and after the dollar-gold peg was abandoned. Notice how copper prices rose powerfully from their 1932 deflationary lows through the 1970s. In contrast, from the dollar’s devaluation in 1933 through the closing of the gold window in 1971, gold prices were frozen. The spectacular rise in gold after its release in the 1970s was due largely to the beach ball effect. Having been held under water for decades while the rest of the world registered inflation, and then being suddenly released, gold prices exploded upward. The momentum of the rise was such that gold had overshot by 1980, with the result that it trailed in the aftermath.

The crucial takeaway here is that while gold is correctly viewed as an inflation hedge, the notion that it is uniquely powerful in that respect is a myth based on a historic anomaly. And because here in 2021 we are not exiting an era like 1933-1971, the 1970s provide no basis to expect gold to now be any more effective than other physical commodities as an inflation hedge. Gold’s truly differentiating property is that among the major commodities, it is least industrially dependent, least correlated to stocks, and therefore most helpful in the context of a portfolio dominated by stocks, most likely to carry the day in those periods when stocks are not pulling their weight as inflation hedges. In a time when inflation threatens as both stocks and bonds are overvalued and vulnerable, a robust inflation hedge includes not only gold but industrial metals and other physical commodities as well.

…

2 thoughts on “Copper & Gold”