Foundation of Value

Salviati: Did you hear? It has been discovered that the earth is round and orbits the sun!

Simplicio: Nonsense. The world is a flat plate supported on the back of a giant tortoise.

Sagredo: That doesn’t make sense. If the world needs something to hold it up, why not the tortoise? What is the tortoise standing on?

Simplicio: Another turtle.

Salviati & Sagredo: ??? So what’s that turtle standing on?

Simplicio: Why, it’s turtles all the way down!

Turtles all the way down economics

We have data for the value of about every imaginable asset. Stocks, bonds, commodities … you name it, you can find the price. Oddly, the world’s most widely used security, the US Dollar, is an exception. That’s because of our habit of using the USD as the unit in which we price everything else. If we try and price the dollar in dollars, we get nothing but the trivial value of 1. It’s useless because it’s always the same, even though we see evidence that it changes every time we pay the bills or go shopping.

The problem is really one of currencies in general. We do have forex data purporting to state the value of “the dollar”, but it’s only in terms of other currencies. Given that we have nothing with which to value those other currencies, though, the whole exercise is circular. It’s turtles all the way down.

A indirect measure, the Consumer Price Index (CPI), values a basket of goods and services in terms of the dollar, the implication being that the dollar is a stable unit while the value of goods and services fluctuates its way higher. No plausible justification has been advanced for such an assumption, despite how widely it is implicitly used in pricing just about everything.

But we can invert the CPI to find the value of the dollar in terms of a basket of goods and services. But that presupposes, without any logical underpinning, that a basket of goods and services itself is a stable datum, unchanging in value. How do we value the goods and services? In dollars! Turtles all the way down. Worse yet, we know it badly lags actual changes in the value of the dollar because the dollar itself lives the asset markets, where it’s changes in value are first registered. It takes time for those changes in value to work their way through to final consumer prices.

And it’s a highly questionable mission creep for the CPI, originally designed as a cost of living index, not a general index of inflation. Other purported measures of inflation, like the Producer Price Index (PPI), the Personal Consumption Expenditures (PCE) deflator, etcetera, are all similar, in that they assume a “things” based standard of value.

They assume things are an unchanging reference. But not only has there been no serious attempt to defend the assumption, it’s demonstrably false. A buggy whip does not have the same value in 2025 as it did in 1925. And an iPhone certainly did not have the same value in 1925 as it does in 2025!

reductio ad absurdum

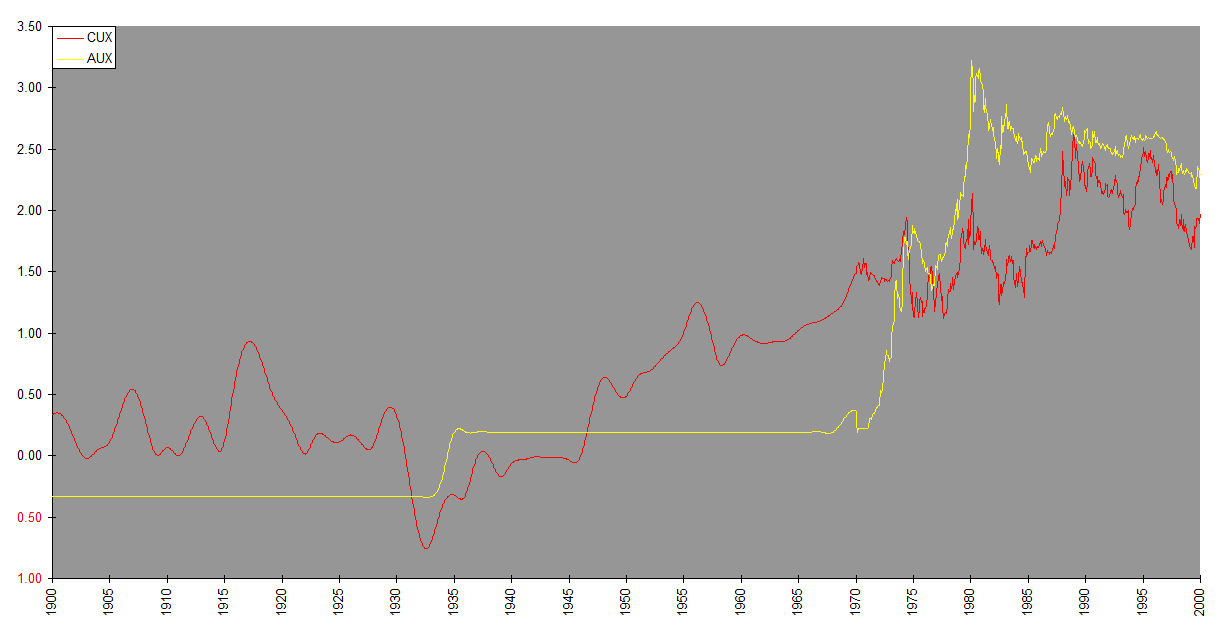

What about gold? Classically gold has been used as a unit of market value. It’s an improvement over other currencies, with their political control and manipulation. We could invert the price of gold to express the value of the dollar in terms of gold. But despite the appeal based on gold being a naturally uninflatable money, and its record of holding its value over very long periods of time, it is also a “thing” and over years and decades undergoes changes in market value of its own.

For example, the value was artificially suppressed for decades by being tied to the dollar via a gold standard. The following chart shows its dollar price compared with that of another elementary commodity, copper, which was not subject to the same artificial restraint.

That may be questioned as exceptional, yet even in times when gold was not artificially tethered to the dollar, its value has fluctuated widely. The price of gold in dollars declined over the twenty year period from 1980-2000, which inverted would imply an appreciating dollar … quite a stretch given the depreciation of the dollar visible against other assets and consumer goods and services.

When you think about it, it’s remarkable that an entire field with a pretense to science, and that regularly uses units of market value, has defined no reliable such units. No wonder its practice has produced such poor results over the decades.

Contrast that with much more successful science and technology based on reliable units like kilograms, meters, and seconds.

The last turtle

Do we have any alternatives to the widely accepted but deeply flawed “turtles all the way down” economics? I believe we do. I propose human time as the natural unit of value.

It is the one thing every one of us has the same amount of every day, every year. No matter what. Moreover, that amount has remained unchanged since the dawn of the human race.

I take it as axiomatic that human time is the fundamental invariant of economic value. There is no economic value without it. What for instance would be the economic value of an iron mine, an ounce of gold, a golf course, or an iPhone without humans?

So why might consumer goods and services have become the de facto standard in the economics community?

It results in a lower reported rate of inflation. As technology lowers the real cost of producing goods and services, they become less expensive in real terms. So using consumer goods and services as a standard makes inflation appear less than it really is. And the field of economics is dominated by political and financial interests that benefit from inflation.

The Financology Dollar Index

I have been publishing an index of the value of the dollar since Financology’s inception. Longer, really, going at least as far back as 2008 on iTulip. It is unlike all other means of measuring the value of the dollar in that it is not based on “things”, but on human time. If we accept the premise that human time is the fundamental unit of value, the question remains of how we could use it to track the changes in market value of other things, including the dollar itself.

This is not so simple. How in the world do you measure the value of something in terms of human time?

Wages and salaries present themselves as obvious candidates, since they represent the rate at which people actually exchange their time and dollars. But whose wages? Americans? The rest of the world’s population doesn’t count?And trading one’s time for dollars is more than a statement about the value of dollars and one’s time. There are all the other factors besides the value of the currency that come into play in arriving at wages, such as working conditions, taxes, etc. I for one would demand more dollars for spending an hour as a window washer on the fiftieth floor of a skyscraper than I would in the comfy office on the other side of the glass. Wouldn’t you? It would also fall short of being universal by virtue of excluding some forms of compensation, for instance, benefits, stock options, etc. It also needs to account for time spent in other than formal employment; leisure time has value too, or people would not want it.

Moreover, not every currency-time transaction in the world involves an exchange of dollars. It might involve an exchange of some other currency, through which we could infer a dollar equivalence via exchange rates. If we want our measure to be truly universal, it can’t just be based on domestic goods and services prices, but has to be global in scope.

We have to take an indirect route. We know the total of human value; we can derive it from our definition. It’s the total world population times the time for which it exists. So the total economic value of 2025 for example would be about eight billion human years.

We have estimates of the total world dollar value of GDP, GNI and related statistics. Using this data a conversion factor between total economic value in human hours and the total economic value in dollars can be derived to yield hours per dollar.

For illustration purposes, recent estimates for world population and GDP are 8.23B and $115.49T respectively. This gives us an exchange rate of 1 USD = 0.000,071,26 human years. Converting to hours, 1 USD = 0.62468 hh.

That’s for the year 2025; an average over the course of the year. Obviously it changes (usually drops) from year to year. But that hardly means it doesn’t change more frequently. We would like to have higher frequency data, for instance weekly, and in fact that is the interval I use for the FDI. But that gets still more complicated. So besides the fact that even measuring economic aggregates like world population and GDP is itself an exercise in estimation, we have to take a less direct approach, using data that is available weekly, taking advantage of the fact that the total purchasing power of value storage assets is tautologically equal to the body of stuff available for purchase, as I outlined in The Claw Machine. This means we can use asset market capitalizations – currencies, commodities, stocks, bonds – to infer intrayear values between annual data. The uncertainty factor is however somewhat offset by the greater accuracy of the market data we have for these assets. All told, the FDI is an imperfect measure of the value of the dollar, leaving room for refinement in light of the available data. It is, however, much less so than any other published data I am aware of, conspicuously including the CPI and PCE.

Other dimensionally correct measures can be envisioned; for example per capita retail sales per unit time. Retail sales over the course of a given time frame would be divided by population, yielding a quotient in units of dollars per unit of human time. This of course would leave open questions of which population and whether retail sales were sufficiently comprehensive to represent the entire economy. As suggested in the post, hourly wages would also be dimensionally correct, but likewise subject to similar questions. To the extent they could be made comprehensive though, we would expect various such measures to converge to a common value.

Republicide

House GOP will not allow amendment vote to extend ObamaCare subsidies

War Tonight?

9pm EST ?

I dunno … I’m not gung ho on any war, but guess if the US is gonna get involved better it be in its own hemisphere. It might be too much to hope it’s about something more constructive.

I was wrong. My hope that this was not about warmaking wasn’t too much. I’m not sure how constructive it was, but the President’s speech apparently turned out to be more of a mini-State-of-the-Union in which Venezuela wasn’t even mentioned.

It’s the usual Trump braggadocio and promises of great things to come. It sounds like he knows his popularity has flagged but doesn’t understand why. It really is affordability, not helped at all by his polices of a tax cut feast for corporations, table scraps for people, and inflationary deficits and interest rates.

The war over Warner Bros Disc is a little disturbing. Netflix should not be allowed to monopolize classic content. Where are the anti-trusters? Will consumers be forced into a particular service to access content it didn’t create? There needs to be more light of day between media and content.

On a related vein, copyright renewals have gotten out of hand. Indefinitely renewable copyrights are inconsistent with the constitutional provision of “limited times”. Generations old content should be public domain by now.

Gold is approaching its record high again, but this time at a more sustainable pace. Silver is breaking new records practically daily. Rotation continues in stocks. Synthetic Systems indicates an elevated probability of significant downside in 2026 Q1. As a whole, I expect 2026 to be a better than average year for cash and bonds.

Non-gold-silver commodities also deserve a closer look in 2026. Oil especially is historically cheap and broad commodity indices like the SPGSCI, heavy in energy, could be the sleepers that awake in the coming year.

This year was the beginning of the end for American exceptionalism in markets, top strategist says

Uhm … no it wasn’t. Look first to 2020, when the Fed hammered rates down to zero, promised to hold them there indefinitely, and printed by the trillion.

Okay fine, you could make a case that the initial salvo of this moneypalooza was justified. Covid triggered a deflationary crash (though the economy was headed towards recession even before that, as evidenced by the soon-forgotten yield curve inversion of 2019). By April, oil prices had gone negative.

But even after the crash had ended and prices were soaring, especially in early responders like stocks, realty and commodities, the Fed kept going. And even when this inflationary surge started to show up in late responders like consumer prices, the Fed went into denial, tarnishing the word “transitory” for years. How this was anything but negative for the dollar and American financial exceptionalism isn’t explained in the above linked propaganda piece.

The next blow came in 2022 when the US weaponized the dollar and its global hegemony, freezing and seizing Russian assets. This assault on property rights and egregious abuse of its exorbitant privilege served to put the world on notice that the US could not be trusted with its dominant position as the issuer of the primary reserve currency.

We could go back further, but you get the point. It sure didn’t start this year.

The above linked piece of amnesiac reportage and revisionist history should crawl back into the swamp from which it slithered.

So why do you suppose the corporate media are spewing such propaganda?

It’s simple … corporations hate tariffs, because part of the cost comes out of their bottom lines. They love cheap immigrant labor, because it bolsters their bottom lines. So they bend over backwards to spin a narrative in which all bad things come from tariffs and tight borders.

The BLS released this morning the November CPI and it was a shocker. The year over year increase expected was 3.1% … the data came in at 2.7%. Corporate media were beside themselves, aghast at the apparently good news.

“Butbutbutbutbut … TARIFFS!!!” one reporter screamed. Another sobbed “This wasn’t supposed to happen!”

As the day wore on, its anti-tariff agenda under threat, corporate media rushed out numerous reports questioning the validity of the data, dismissing it as a statistical distortion induced by the government shutdown.

The elephant in the room, however, was never spotted. ALL of these reports are statistical distortions. The CPI has been understated at least since the Boskin Commission and has NEVER been the measure of general inflation econ lite pretends it to be. I have discussed this at length repeatedly in these pages.

The irony is that for once, the stopped clock is right … the stats understate the price increases endured by Americans … but that’s the way it has been for years.